Location: Home >> Detail

J Sustain Res. 2026;8(3):e260065. https://doi.org/10.20900/jsr20260065

,

Antonio Pereira 1 ,

Camila Cunha 1 ,

Sônia Gomes 1

,

Antonio Pereira 1 ,

Camila Cunha 1 ,

Sônia Gomes 1

1

2

*

The study uses an experimental design to investigate investors’ reactions to suspending Environmental, Social, and Governance (ESG) projects versus suspending general business projects, accounting for the life cycle of both initiatives. The study employed a 2 × 2 design with an initial population of 231 participants, classified as investors and comprising graduate students and members of Finance Leagues at Brazilian universities. After excluding participants who did not qualify as investors or did not understand the experiment, the final sample consisted of 162 participants. The analyses involved tests of means and analysis of variance (ANOVA). The results indicated that investors react more positively to the launch of conventional business initiatives, possibly because they associate these initiatives with increased financial performance and shareholder returns. Regarding discontinuations, we found that discontinuing ESG projects elicits a more negative reaction than discontinuing traditional initiatives, suggesting that investors interpret the decision as a waste of resources and a negative signal to the market and others. The findings advance the literature on behavioral finance, ESG, and decision-making, while offering practical implications for organizations seeking to align sustainability with value creation. Furthermore, the results shed light on how distinct categories of initiatives are perceived by investors, providing insights for companies, regulators, and policymakers regarding the disclosure and management of social and environmental practices.

ESG, environmental, social, and governance; ANOVA, analysis of variance; CSR, corporate social responsibility; CVM, Brazilian Securities and Exchange Commission; WTA, willingness-to-accept; WTP, willingness-to-pay; H1, Hypothesis 1; G1, Group one; G2, Group two; G3, Group three; G4, Group four; UFBA, Federal University of Bahia; UCSAL, Catholic University of Salvador; UNIFACS, University of Salvador; UFS, Federal University of Sergipe; USP-RP, University of São Paulo-Ribeirao Preto; CI, Confidence Interval; Df, Degrees of Freedom; Sq, Squared; IR, Investor Reaction; ME, Market Evaluation; CE, Customer Evaluation; WE, Worker Evaluation; ATM, Before Manipulation; DTM, After Manipulation; Diff, Mean Difference between the Compared Groups; FAPESB, Bahia State Research Support Foundation; CNPq, National Council for Scientific and Technological Development

The publication of sustainability reports, although voluntary, has become important to investors, and large companies have issued them, covering information on the organization’s interactions with its stakeholders, namely the community, employees, and consumers [1,2].

In this sense, ESG standards have led some stakeholders to shift their business expectations, no longer investing solely in companies based on financial factors but also considering social and environmental initiatives, and emphasizing robust corporate governance [3]. These shifts in perspective demonstrate that some investors have come to value organizations that adhere to ESG practices and react significantly when these initiatives are discontinued [3–6].

Nevertheless, it is important to note that this market trend has not yet taken hold, as some stakeholders have criticized and even questioned the way ESG practices are disclosed [7]. In this regard, there is information that in 2023, BlackRock, the world’s largest asset manager, reduced its support for ESG proposals to historic lows, as disclosed in the company’s governance report [8]. This evidence corroborates the study by [9], who identified a reduction in resource allocation to strategies explicitly guided by ESG criteria, with a shift toward investments considered more neutral in addressing climate change.

Changes in investment patterns, particularly observed in Europe, the United States (US), and Asia, are evidenced by investments in green assets [10]. For example, the world’s 500 largest companies spend an average of $20 billion on ESG reporting and invest approximately $35 trillion in assets linked to ESG practices [3,10].

Brazil’s stock exchange created an ESG index in partnership with S&P Dow Jones. BTG Pactual bank has established an index fund that tracks the Brazilian Stock Exchange index, and the world’s largest asset manager, BlackRock, despite reducing its support for ESG projects, analyzes its investment portfolio using ESG metrics [3,5,10,11].

Thus, the ESG movement has demonstrated its ability to influence the decision-making of many investors, encouraging a preference for sustainable assets over non-sustainable ones [3]. This process highlights the importance of ethics and social responsibility as central criteria in investment selection [5]. Previous studies show that ESG reports can influence investors’ judgments [12]. However, investors do not see value when ESG performance is negative [4,6].

The debate over the value creation of ESG initiatives becomes even more sensitive when considering their potential discontinuation, as evidence indicates that the market reacts differently to such discontinuations [5].While Guiral et al. (2020) [6] point out that the impact of ESG initiatives depends on their relevance and alignment with core business activities, Garavaglia et al. (2023) [5] show that the market reacts significantly more negatively to the discontinuation of ESG initiatives than to the discontinuation of conventional business projects.

This finding suggests that the discontinuation of ESG projects may be interpreted differently by investors, depending on regulatory expectations and commitments previously communicated to the market [5,13]. Although Santos et al. (2024) [2] indicates that the value-generating capacity of these environmental initiatives depends on the firm’s financial condition, there remains a need to better understand how the Brazilian market specifically reacts to the discontinuation of ESG projects compared to traditional projects.

The most significant advancement regarding the discontinuation of ESG initiatives and investor behavior, considering the ethical and moral context, came from the study by [5], who introduced the concept of the ESG stopping effect and examined whether investors value ethical considerations differently across the life cycles of ESG initiatives compared to those of conventional business initiatives [5].

Emerging countries, such as Brazil, still face structural challenges in ESG practices due to social and infrastructure problems, institutional fragility, and limitations in the informativeness of environmental disclosures [2,14]. In addition, characteristics such as high tax costs, a volatile macroeconomic environment, and the predominance of a civil law legal system can influence the functioning of governance mechanisms and investor perceptions [15].

In May 2026, the Brazilian Securities and Exchange Commission (CVM) published Resolution 244 [16], which repealed the requirement for publicly traded companies to prepare and disclose sustainability and climate reports (IFRS S1 and S2 standards). The disclosure of these reports is now entirely voluntary. This shift in stance by the Brazilian capital markets regulator underscores that a significant portion of investors believe the current costs are not fully justified by future benefits in terms of stock returns. Therefore, the context of the Brazilian capital market—where some companies, such as Vale and Lojas Renner, voluntarily disclose their sustainability reports—has sparked debate among academics, investors, and regulators regarding how investors define their investment strategies, particularly when guided by ESG indicators or initiatives.

Based on behavioral, ethical, and moral theoretical approaches, Brazilian investors are expected to exhibit significant skepticism toward allocating resources to companies with ESG initiatives, given the opportunistic behavior of some corporations. As reported by the Brazilian press, Gol Linhas Aéreas was ordered to pay R$ 5 million in collective moral damages for engaging in greenwashing. The basis for the ruling was the finding that the company’s programs offered carbon offsets through “tokens.” The complaint highlighted a lack of transparency in the methodology, the absence of an audit, and the use of carbon credits of dubious origin [17]. In this specific institutional context, although the international literature shows that ESG information influences investor judgment through informational, moral, and behavioral mechanisms [5], the robustness of this effect in the Brazilian environment remains uncertain, especially regarding the reaction to the discontinuation of such initiatives.

Given the lack of experimental evidence on how investors in emerging markets, particularly in Brazil, react to the discontinuation of ESG projects compared to conventional projects, we formulated the following research question: how do investors react to the discontinuation of ESG projects compared to the discontinuation of general business projects, considering the life cycle of the initiatives?

To address the research question, the study’s overall objective is to investigate, through an experimental design, investors’ reactions to the discontinuation of ESG projects compared to those of general business projects, accounting for the life cycles of both initiatives.

ESG initiatives have gained prominence in corporate practice worldwide [5]. In the United States, ESG investments reached approximately $12 trillion in 2020 [18], while United Nations (UN) Principles for Responsible Investment signatories managed over $100 trillion in assets incorporating ESG criteria [19]. In Brazil, ESG funds raised approximately R$2.5 billion in 2020 alone [11].

Previous studies suggest that investors respond more positively to information about sustainable investments, believing that effective ESG investing increases a company’s value, leading them to pay more for its assets, and that valuation estimates are influenced by whether CSR performance is explicitly assessed [4,6,12].

Experimental studies consistently show that investors incorporate ESG and CSR performance into their value estimates. Elliott et al. (2014) [4] examined whether an unintentional affective relationship exists between CSR performance and investors’ fundamental value perceptions, and whether explicit CSR assessment moderates this relationship. Their results show that investors who did not explicitly evaluate ESG information were willing to pay higher prices for shares than those who did (suggesting an affective halo that explicit analysis moderates).

The materiality of ESG information further moderates these reactions. Guiral et al. (2020) [6] found that when CSR performance is driven by issues core to the business, investors’ fundamental value estimates are not affected by explicit CSR assessment; however, when immaterial issues drive performance, positive CSR performance increases value estimates only in the absence of explicit assessment, underscoring that the reporting channel shapes the information’s impact.

Despite the prospect of a shift in mindset among some investors, it is important to recognize that the ESG movement has also been the target of skepticism and controversy [9]. Studies indicate that many initiatives classified as sustainable lack measurable, standardized, and transparent criteria [9,20]. This deficiency has contributed to greenwashing and socialwashing practices, characterized by the disclosure of environmental or social information that does not align with the entities’ actual practices [7].

Furthermore, the study by [21] provides evidence of a negative relationship between ESG disclosures and market value. Similarly, previous research by [22], and Duque-Grisales and Aguilera-Caracuel (2021) [23] also found a negative association between ESG practices and corporate performance.

With the expansion of the sustainable market, companies have begun to adopt ESG practices not only as a strategy for competitiveness in the global market but also to mitigates the risk of stock price [24]. However, the literature also suggests that such practices may be motivated by symbolic incentives, including opportunistic ones, reflecting legitimation, or signaling strategies that are not necessarily accompanied by the changes the initiatives propose [3].

However, Lima and Queiroz (2025) [25] found, in a study of the effect of socio-environmental corruption scandals on the financial performance of companies adhering to ESG practices in Latin America, a positive relationship between such scandals and corporate performance. This result diverges from the literature, which maintains that ESG performance is associated with firm value, with higher value when ESG performance is positive [4,5].

In this context, the literature has begun to investigate not only the effects of CSR and ESG performance but also investor reactions throughout the life cycle of these initiatives [5]. The study by [5] shows that investors react more negatively to the discontinuation of ESG initiatives than to the discontinuation of general business initiatives, even after accounting for the projects’ life cycles. This result indicates the need to identify the theoretical mechanisms that explain the observed asymmetric reaction.

On the other hand, despite divergent assessments of these practices, investors feel responsible for the interruption of ESG initiatives, even when they are not [5]. This occurs because they perceive they have a role in the manager’s decision-making, leading them to react negatively to such interruptions [5]. Furthermore, this reaction tends to be even more negative when the ESG project is proven to be effective. However, when the project’s interruption is properly justified, reactions are mitigated [5].

Previous studies have found that investors react more negatively to environmental issues for nonfinancial reasons, such as emotional and moral considerations [5]. These reasons may explain why shareholders are more likely to react negatively to the discontinuation of ESG projects [26–28].

Literature from other disciplines, primarily economics and psychology, makes causal inferences and predictions. This literature posits that investors may consider ethical and moral aspects when making decisions [5].

In economics and psychology, people tend to value items they own simply because they own them [29]. In this context, according to Prospect Theory, discontinuing an ESG initiative can be framed as a loss that is not only financial but also ethical and moral, thereby amplifying loss aversion [29,30]. This mechanism is consistent with the idea that previously assumed socio-environmental commitments create expectations and a sense of ethics, the breach of which generates a higher evaluative penalty than that associated with discontinuing conventional projects [5].

Furthermore, in line with [13] signaling theory, the adoption of ESG initiatives can signal to investors a long-term commitment, managerial quality, and a sustainable strategic orientation. In contrast, investors interpreted their discontinuation as a negative signal regarding the company’s strategic consistency, ethical and moral standards, or financial soundness, intensifying investors’ adverse reaction.

In addition, based on [31] attribution theory, the discontinuation of an ESG initiative can be attributed to opportunistic motivations, a lack of moral and ethical commitment, or an exclusive prioritization of financial results, leading to harsher judgment than that directed at the discontinuation of a general business project, which has a lesser ethical dimension [5].

From this perspective, much of the literature suggests that ethical and moral characteristics can moderate the endowment effect [5,26,27,32,33]. Furthermore, this effect is intensified when environmental issues and ESG initiatives are brought to the fore.

Studies consistently show that willingness-to-accept (WTA) values exceed willingness-to-pay (WTP) values when environmental assets are involved, and that this disparity is amplified when human action, rather than natural causes, produces environmental damage [26,32,33]. Critically, the asymmetry is explained by individuals’ sense of moral responsibility toward environmental assets [26,27], which can be seen as a mechanism that parallels the ethical co-responsibility investors feel when firms discontinue ESG initiatives [5].

Although Garavaglia et al. (2023) [5] provides robust evidence on the discontinuation of ESG initiatives, some questions remain about their generalizability across distinct institutional contexts, as previously discussed. Emerging markets exhibit significant differences in regulatory enforcement, capital market maturity, the degree of internalization of ESG practices, and the level of skepticism toward corporate sustainability (factors that may influence the intensity of investor reaction to the discontinuation of socio-environmental initiatives) [2,14,15]. Furthermore, more unstable economic environments may alter the relative weight of financial versus ethical considerations, potentially moderating the effect identified in the literature [15].

From this perspective, by integrating the studies discussed in this section with the loss-aversion logic of Prospect Theory, the informational interpretation of Signaling Theory, and the inferential mechanisms of Attribution Theory, we formulated the following Hypothesis 1 (H1):

H1: Investors will react more negatively when an ESG initiative is discontinued compared to the discontinuation of a general business initiative, considering the life cycle of both initiatives.

The experiment used a simple, straightforward design to test H1, which posits that investors will react more negatively to the discontinuation of the ESG initiative. In this context, the hypothesis is not rejected if participants respond more negatively to the discontinuation of the ESG project than to that of the conventional business project, according to an international study [5].

In this procedure, we analyzed dependent variables—such as investor decisions—and independent variables—related to the initiatives, the market, the customer, and the company in question—as well as the experiment’s control variables. This enabled inferences from investor responses, with statistical tests used to validate results and identify significant patterns. This methodological approach helped clarify the dynamics between interruptions in the company’s ESG practices and investors’ perceptions and behaviors.

ParticipantsThe study participants were professionals pursuing graduate degrees in accounting, business administration, economics, and other related fields, as well as students participating in the Finance League at Brazilian universities across various states, since experimenting with all investors would have been economically unfeasible. Since the subjects serve as proxies for investors, the questionnaire included questions on gender, ethnicity, age, and educational level, as well as questions to determine whether participants had experience analyzing financial statements and whether they had made investment transactions in the past six months. In this study, we selected only participants who had made at least one investment in the last 6 months or reviewed financial statements. These measures are necessary for the experiment to be properly conducted [5,32].

We divided participants into four groups. Group 1 (G1) involved manipulating the launch of the general business initiative, with 75 participants. In Group 2 (G2), the manipulation was the launch of the ESG initiative, with 57 participants. In Group 3 (G3), the manipulation involved discontinuing the general business initiative, with 38 participants. Finally, Group 4 (G4) involved discontinuing the ESG initiative, with 61 participants. After data processing, the final sample consisted of 162 individuals.

We acknowledge that the sample size, particularly for Group 3, falls below the recommended threshold of 30 to 50 participants per group for traditional parametric tests. This limitation is addressed through our analytical approach, which employs non-parametric statistical methods better suited to smaller sample sizes, as detailed in the Section “Analyses”.

We administered the main instrument in 2025 at the following institutions: at the Federal University of Bahia (UFBA), among students in the stricto sensu and lato sensu graduate programs in Economics, Business Administration, and Accounting, as well as among members of the university’s Finance League; at the Catholic University of Salvador (UCSAL), in the graduate program in Human Resources Management; at the University of Salvador (UNIFACS), in the stricto sensu graduate program in Business Administration; at the Federal University of Sergipe (UFS), with participants from the Finance League; and at the University of São Paulo-Ribeirao Preto campus (USP-RP), in the stricto sensu graduate program.

Similar studies should also show that a financial incentive was necessary to ensure participants responded appropriately to the procedure [27,33,34]. Thus, a weekend getaway for a couple at a Quality Hotel & Suites, including breakfast, was raffled among respondents who completed the pre-test and the experiment.

DesignThe experiment employed a 2 × 2 design: Initiatives (ESG/Conventional) × Decision (Start/Stop), with these variables as independent factors. The research design is consistent with the studies by [5,32,33]. The dependent variables were questions on personal evaluation and the company’s attractiveness, from which we derived the investor reaction variable. Furthermore, as controls, the following questions were included: how the participant believes the market would evaluate the company, the participant’s evaluation of the company as a customer, and the participant’s intention to work for the company. Graduate students assumed the role of investors.

The hypothetical company was Blue House, a nationally renowned supermarket chain that operates exclusively in the retail sector. So, we use a fictional company to control for biases arising from prior reputation established in the social context and actual performance, thereby ensuring greater internal validity for the experiment.

The ESG initiative consisted of launching bags made from organic material, with all proceeds donated to Always on Fund, an organization that supports the development of children with autism. Meanwhile, the conventional business initiative involves launching durable plastic bags with a distinctive design and a zipper that seals the bag, and the revenue from their sale will be added to the company’s revenue.

Procedures and Stages of the ExperimentThe procedure was carried out in six stages, using five envelopes and a video, since investors tend to use information in a one-dimensional manner. Thus, the staged experiment helped elicit more accurate responses [12]. The experiment was conducted by an independent facilitator, with materials organized in letterhead envelopes, each identified by an ID number.

The facilitator prepared the environment, ensuring that speakers were available and that there was no noise or interruption that could interfere with the experiment. He then provided general information about the procedure and began distributing the envelopes.

In the first stage, the facilitator distributed 1, containing the informed consent form and a detailed description of the experiment. The participants read the instructions. Providing instructions in the questionnaire ensures that participants have equal conditions for beginning and completing the experiment [33].

In the second stage, the facilitator presented Envelope 2, which included a company overview covering its operational context, mission, vision, values, financial aspects, customer service, and business practices. This description helps participants understand the scenario applied in the decision-making process.

In the third stage, the facilitator distributed Envelope 3 to participants and included the pre-experimental questions, aimed at assessing investors’ reactions prior to the manipulation and enabling comparisons between the groups. Participants answered the following questions before receiving information about the company’s initiatives: Question (1) how they believed the market would value the company’s stock; Question (2) how they would personally value the company’s stock; Question (3) to what extent they would consider the firm attractive; Question (4) would they be willing to purchase the company’s product; and Question (5) to what extent would they be willing to work at the company. The questions were rated on a 101-point scale, divided into increments of 0, 25, 50, 75, and 100. This type of scale ranges from 0 to 100, with 0 representing an extremely negative evaluation and 100 a very positive one.

In the fourth stage, the facilitator showed the video (i.e., the experimental condition) to participants in their respective groups. The video lasted between 1 min and 2 min and 20 s and presented different scenarios: (1) Group 1 watched a video about the general business initiative; (2) Group 2, about the ESG initiative; (3) Group 3, about the interruption of the general business initiative; and (4) Group 4, about the interruption of the ESG initiative.

In the fifth stage, the facilitator distributed Envelope 4, which contained the questionnaire with post-experimental questions. Participants answered the five questions from the previous stage again to update their responses based on the current information. This stage allowed us to capture the effect of manipulation on the perception and adoption of each initiative, as well as on the disruptions.

In the sixth stage, the facilitator finally distributed Envelope 5, which contained the experiment verification questionnaire and questions on participants’ demographic information, including age, educational background, and investment experience.

After each stage, the corresponding envelope was collected, and the next-stage envelope was distributed. The experiment was estimated to last 30 to 50 min.

Internal and External Validity of the Experiment Internal ValidityWe ensured the instrument’s internal validity through multiple methods. First, 10 experts with knowledge in Investments, CSR, and ESG evaluated the questionnaires to improve the instrument, identify biases, refine the questionnaires, and point out redundancies in the forms. This procedure aims to increase the internal validity of the research, as outlined by [35].

Consequently, analyzing participants’ reactions before and after the manipulations allows us to account for individual differences in how investors respond to the research context. This procedure means that the observed variation can be attributed more accurately to experimental manipulations rather than to preexisting individual differences [36]. Furthermore, separating questions related to market assessment from those on participants’ personal assessments ensures greater precision in data collection, avoiding confusion and providing a clearer view of investors’ perceptions of the impact of ESG initiatives [5].

Furthermore, the Investor Reaction variable was measured using the Personal Assessment and Attractiveness variables, thereby strengthening the construct’s reliability and validity [37]. Including additional variables, such as customer and employee evaluations, enables a broader understanding of the influence of ESG initiatives on other stakeholders. This approach not only validates investor reactions but also assesses whether they are consistent with perceptions of other stakeholders, offering a holistic view of the impact of Blue House’s ESG initiatives [38].

External ValidityWe strengthened the external validity of the study by selecting participants who were graduate students in business administration, accounting, economics, and related fields. So, we used these professionals as proxies for investors, given their familiarity with financial statement analysis and a tendency to invest in stocks and other investments. The questionnaire included specific questions to verify that participants had analyzed financial statements and made at least one investment in the past six months, ensuring that the sample is representative of typical investor behavior [5].

Furthermore, selecting these students as proxies allowed the results to be generalized not only to other students and professionals but also to the general investor population. Professionals pursuing graduate studies in the fields and students participating in the Finance League often qualify as investors due to their knowledge and ability to interpret financial data and make informed investment decisions. Therefore, the chosen sample increases the generalizability of the results, thereby strengthening the study’s external validity and enabling the conclusions to be applied to a broader audience of investors [39].

We acknowledge important limitations regarding the external validity of this study. The participants were primarily graduate students in business administration, accounting, economics, and related fields, as well as members of Finance Leagues, rather than active investors in real market conditions. While these individuals serve as proxies for investors due to their familiarity with financial statement analysis and investment experience, they do not represent the full diversity of the investor population [5].

Pre-TestAccording to [39], pre-tests should be included in experimental designs. Thus, to verify that the questions did not pose structural problems that could invalidate the results of the entire research, we conducted a pre-test with students in the final semester of the Undergraduate Accounting Sciences program. The students served as proxies for investors and responded to a preliminary application of the questionnaire [36].

In this sense, the sample for this test was small, using 20 students, considering that the main objective of the pre-test was to identify potential problems, ensuring that the questions were understandable and appropriate for the research’s target audience. Furthermore, it is important to note that the participants were randomly selected and did not participate in the main experiment [5]. The pre-test was conducted at UFBA in 2024 with 20 participants, five in each experimental group.

AnalysesFirst, the sample is characterized demographically through descriptive statistics. Next, the responses of the dependent variables are collected before and after the independent variables, that is, the firm’s ESG and conventional project initiatives and interruptions. In the third analysis, we classified the responses referring to the mean changes in Questions (2) and (3) as Investor Reaction, according to the study by [5].

In the fourth analysis, Question (1) is asked so that participants can express how the market evaluates the company. This method facilitates the isolation of investors’ individual opinions, as they will not confuse their individual opinions with those of the market. According to research, investors’ perspectives differ from the markets on average [5].

Responses to Questions (4) and (5) make it possible to identify whether investor reactions are in line with those of other stakeholders, such as customers and employees. Previous studies assume that investors in ESG assets should incorporate the perspectives of customers and employees into their analysis [5].

Finally, inferential analysis is conducted using the Analysis of Variance (ANOVA) technique to identify differences in the means of the groups analyzed before and after the manipulations [5]. We tested the main equation according to Equation (1).

concerns the company’s overall initiative and the ESG initiative; concerns the company’s overall initiative and the ESG initiative; Equation (1): Investor Reaction represents the dependent variable of the model, represented by the investor’s reaction to the decision regarding initiatives and decisions. Initiatives is the independent variable that identifies the type of initiative presented (ESG or general business). Decisions correspond to the variable that indicates the decision related to the initiative (launch or interruption). The term (Initiatives × Decisions) represents the interaction between the type of initiative and the decision made. β0 is the model intercept; β1, β2, and β3 are the estimated coefficients; and εi corresponds to the error term.

Investor Reaction is operationalized by Equation (2), in which Initiatives include conventional and ESG projects; Decisions refer to the actions of starting and stopping; and the third variable represents the interaction between Initiatives and Decisions. This specific interaction indicates that the decision to discontinue an ESG initiative has a more negative impact on investors’ reactions than the decision to discontinue a conventional business project.

Personal Evaluation Variation (∆) represents changes in investors’ perceptions of the company, while Attractiveness Variation (∆) indicates changes in investors’ opinions of the company’s attractiveness. These variables will range from 0 to 100 on the 101-point scale.

For example, suppose the investor personally evaluated the company at 50 points before the launch of the conventional business initiative and, after the manipulation, evaluated it at 75 points. The change in personal evaluation, therefore, is 25. Likewise, consider that the investor rated the company’s attractiveness at 25 points, but after the initiative’s launch, began evaluating it at 75 points, resulting in a 50-point change. Thus, the investor’s reaction will be calculated as (25 + 50)/2, resulting in 37.5, which is positive.

We measured the Market Evaluation variable as the change in market evaluation after the manipulation. Similarly, the Customer Evaluation variable represents the change in customer perception after the procedure, while the Worker Evaluation variable denotes the change in employees’ perception. All these variables range from 0 to 100 points on a 101-point scale. We used these measures in the analysis as controls to isolate the investor’s individual opinion and prevent their evaluation from being influenced by perceptions of market evaluations, customer opinions, and workers’ judgments.

To strengthen the robustness of our findings and account for potential confounding effects, we conduct a two-way analysis of variance (ANOVA) to examine the main effects of Initiatives and Decisions, as well as their interaction effects. We also perform nonparametric tests, including the Wilcoxon–Mann–Whitney and Kruskal–Wallis tests. Furthermore, we report effect sizes (Cohen’s d for paired comparisons and partial eta-squared for ANOVA) alongside significance tests to provide a comprehensive assessment of the magnitude of observed effects.

The experimental design adopted was a 2 × 2 between-subjects design, requiring at least 20 participants per group. Since the experiment involved four groups, the minimum required number was 80 participants [39]. We initially applied the experiment to 231 participants. However, after analyzing the verification questions, we found that 69 individuals did not understand how the application worked or did not qualify as investors. Therefore, we excluded these participants from the sample. After data cleaning, the final study sample had 162 participants.

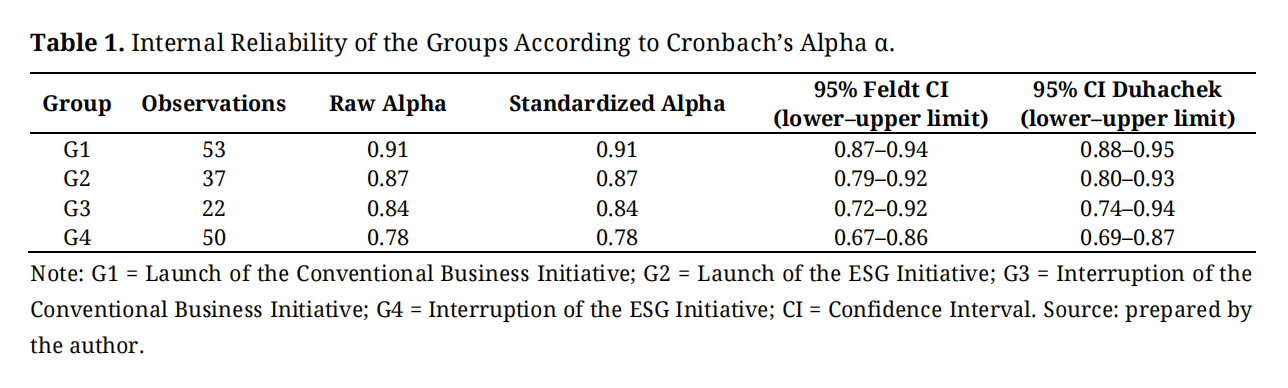

The collected data were tabulated using Microsoft Excel software, and we carried out the statistical tests using RStudio®️ software. To assess the internal reliability of the collected data, we used Cronbach’s Alpha, a commonly used method [40]. Table 1 presents the raw and standardized Cronbach’s Alpha values, along with their respective confidence intervals.

According to Cronbach’s Alpha test, the data collected for Group 1 show excellent reliability. Regarding Groups 2 and 3, reliability is good. Regarding Group 4, reliability is considered acceptable. Thus, since all Cronbach’s Alpha values are above 0.70, the data has adequate internal consistency for analysis [40].

Table 1. Internal Reliability of the Groups According to Cronbach’s Alpha α.

Table 1. Internal Reliability of the Groups According to Cronbach’s Alpha α.

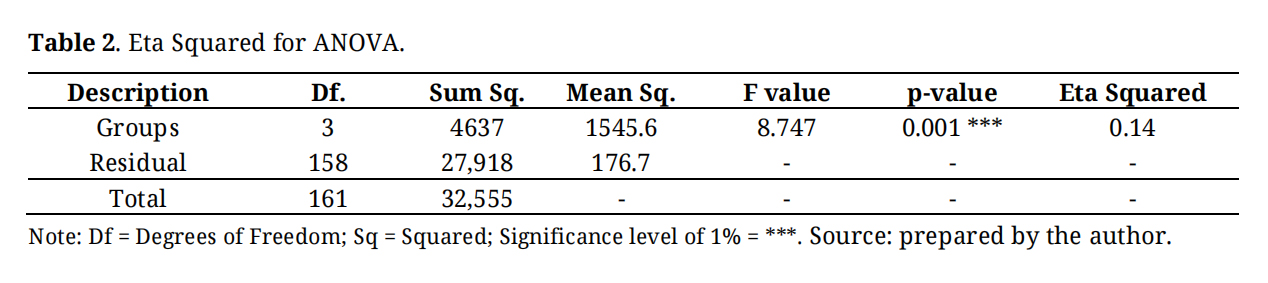

In Table 2, the eta squared (η²) coefficient was calculated to assess the proportion of variance in investor reaction explained by the experimental manipulation. The ANOVA results revealed an eta squared value of 0.14, indicating that approximately 14% of the variance in investor reactions across the four experimental groups is attributable to the type of business initiative (conventional or ESG) and its temporal manipulation (launch or interruption). This effect size is considered medium to large according to Cohen’s conventions, suggesting that the experimental manipulation had a meaningful impact on investor behavior.

The remaining 86% of variance is attributable to other factors not captured in this study, such as individual investor characteristics, market conditions, and external economic variables. The significance of the F-statistic (F = 8.747, p < 0.001) and the substantial eta-squared value indicate that the experimental conditions produced robust, practically meaningful differences in investor reactions.

Table 2. Eta Squared for ANOVA.

Table 2. Eta Squared for ANOVA.

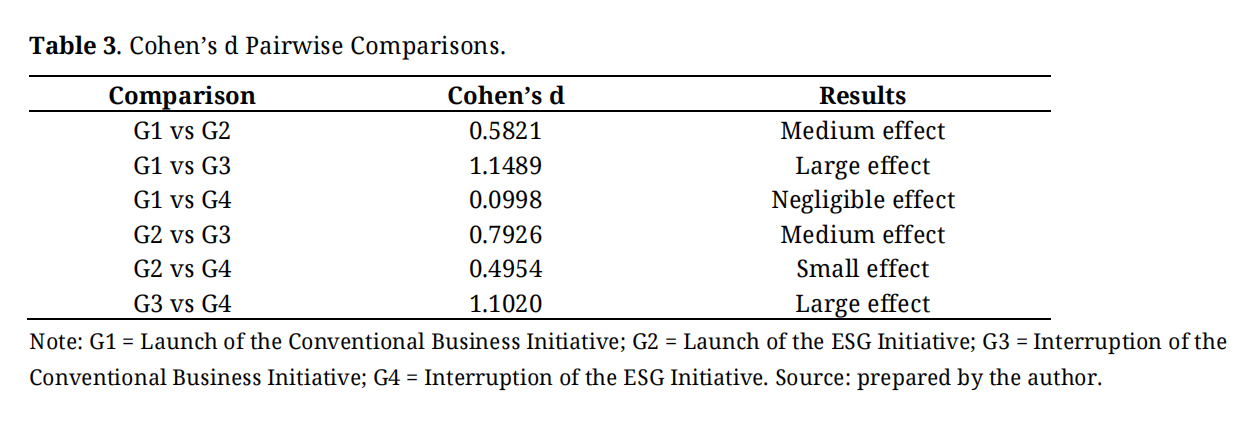

To complement the ANOVA results, Cohen’s d was computed for all pairwise comparisons between experimental groups in Table 3, providing standardized effect sizes for individual group contrasts. The comparisons revealed considerable variation in effect magnitudes across group pairs. The largest effects were observed between G1 (Launch of the Conventional Business Initiative) and G3 (Interruption of the Conventional Business Initiative; d = 1.149, large effect), as well as between G2 (Launch of the ESG Initiative) and G4 (Interruption of the ESG Initiative; d = 1.102, large effect).

These findings suggest that the temporal dimension of the manipulation—whether initiatives were launched or interrupted—produced the most substantial differences in investor reactions. Moderate effects were found for G1 versus G2 (d = 0.582) and G2 versus G3 (d = 0.793), indicating meaningful differences between launch and interruption conditions within each initiative type. The comparison between G1 and G4 yielded a negligible effect (d = 0.100), suggesting comparable investor reactions to launching a conventional initiative and interrupting an ESG initiative. The small effect between G2 and G4 (d = 0.495) indicates relatively modest differences between these conditions. Overall, the effect size analysis reinforces the practical significance of the experimental findings and highlights the differential impact of initiative type and temporal manipulation on investor behavior.

Table 3. Cohen’s d Pairwise Comparisons.

Table 3. Cohen’s d Pairwise Comparisons.

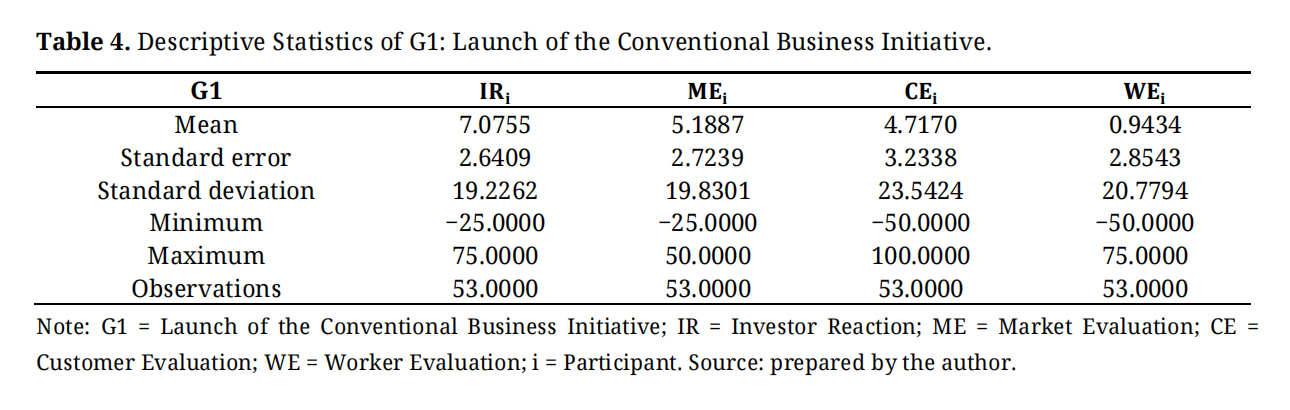

Group 1 refers to the participants in the experiment whose manipulation consisted of launching the conventional business initiative: a project involving plastic bags with a differentiated design that provides benefits to customers, with sales revenue converted into income for the company. In this context, Table 4 presents descriptive statistics for the responses, including the mean, standard error, standard deviation, minimum and maximum values, and the number of observations in this group.

Regarding the launch of the conventional business initiative, the final sample comprised 53 participants. In this sample, we observed that the investor reaction (IR) had a positive average of 7.07, with a standard error of 2.64 and a standard deviation of 19.22, indicating high dispersion around the mean, consistent with [5]. The values ranged from −25 to 75, representing the minimum and maximum, respectively. These results suggest that, in the Brazilian context, investors tend to react positively to the launch of conventional business initiatives.

Table 4. Descriptive Statistics of G1: Launch of the Conventional Business Initiative.

Table 4. Descriptive Statistics of G1: Launch of the Conventional Business Initiative.

The market evaluation (ME) also showed a positive result, with an average of 5.18, a standard error of 2.72, and a standard deviation of 19.83, demonstrating high dispersion around the mean. The values ranged from −25 to 50.

Similarly, the customer evaluation (CE) was positive, with a mean of 4.71, a standard error of 3.23, and a standard deviation of 23.54, indicating greater variability among the responses. The values ranged from −50 to 100.

Finally, the worker evaluation (WE) showed a slightly positive mean of 0.94, with a standard error of 2.85 and a standard deviation of 20.77, evidencing high dispersion of responses. The values ranged from −50 to 75.

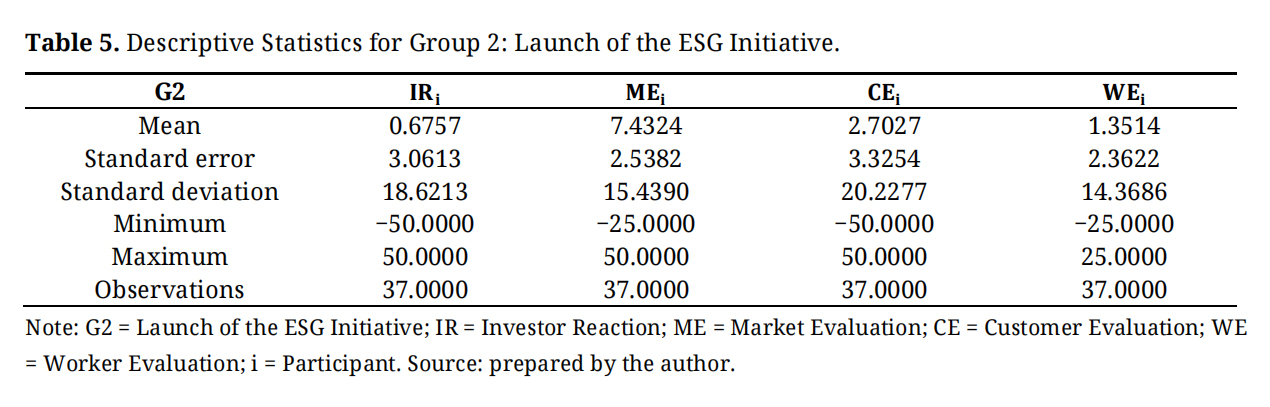

Descriptive Analysis of Group 2: Launch of the ESG InitiativeGroup 2 corresponds to the participants in the experiment whose manipulation involved launching the ESG initiative, namely, shopping bags made from organic materials, to reduce the carbon footprint. Revenue from sales is intended for Always on Fund, an institution that supports autistic children. Thus, Table 5 presents the descriptive statistics of this group’s responses, including the mean, standard error, standard deviation, minimum and maximum values, and the total number of observations.

Table 5. Descriptive Statistics for Group 2: Launch of the ESG Initiative.

Table 5. Descriptive Statistics for Group 2: Launch of the ESG Initiative.

Regarding the launch of the ESG initiative, the final sample consisted of 37 participants. For this sample, we found that the IR had a positive average of 0.67, with a standard deviation of 18.67 and a standard error of 3.06, indicating high dispersion of individual reactions around the mean. The values ranged from −50 to 50. This result is consistent with the study by [5], who also identified a positive reaction (average of 7.72). However, in the Brazilian context, the IR tends to be more neutral toward this initiative than in studies conducted in developed countries.

The ME had an average of 7.43, a standard deviation of 15.43, and a standard error of 2.53, indicating substantial variation around the mean. The values ranged from −25 to 50.

The CE was also positive, with a mean of 2.70, a standard deviation of 20.22, and a standard error of 3.32, indicating a high degree of variation around the mean. The values ranged from −50 to 50. So, we observed that the CE was lower at the launch of the ESG initiative than at the launch of a conventional business initiative, suggesting that Brazilian clients tend to prioritize direct benefits over indirect benefits of ESG practices.

Regarding the WE, the mean was positive (1.35), with a standard deviation of 14.36 and a standard error of 2.36, indicating considerable dispersion around the mean, with values ranging from −25 to 25. Workers’ perceptions were more favorable toward the launch of ESG initiatives (1.35) than toward conventional business initiatives (0.94), indicating that employees evaluate ESG practices more favorably than traditional ones.

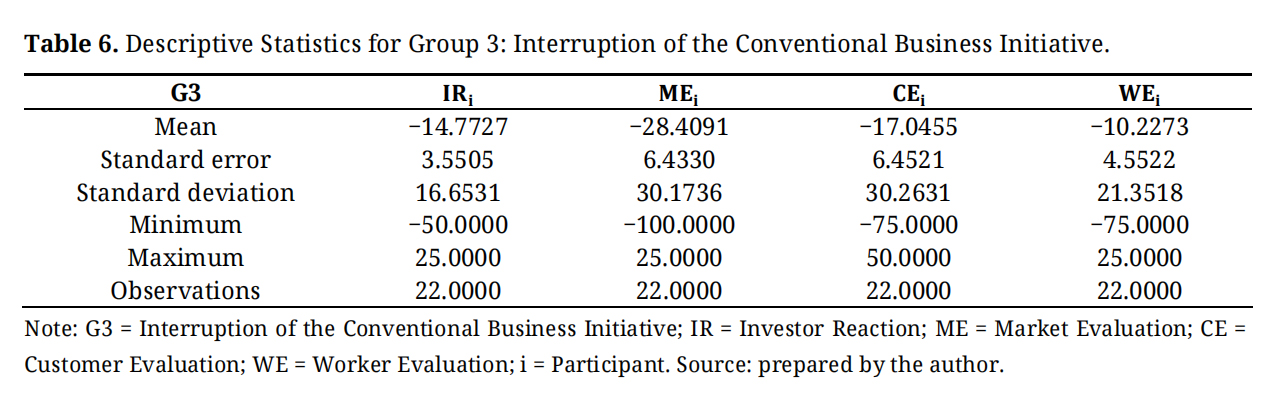

Descriptive Analysis of Group 3: Interruption of the Conventional Business InitiativeGroup 3 consists of participants exposed to manipulation regarding the interruption of the conventional business initiative, that is, the interruption of the project for plastic bags with a differentiated design. From this perspective, Table 6 presents descriptive statistics for this group, including the mean, standard error, standard deviation, minimum and maximum values, and the number of observations.

Table 6. Descriptive Statistics for Group 3: Interruption of the Conventional Business Initiative.

Table 6. Descriptive Statistics for Group 3: Interruption of the Conventional Business Initiative.

Regarding the group related to the interruption of the conventional business initiative, the final sample consisted of 22 participants. The mean IR was negative (−14.77), with a standard error of 3.55 and a standard deviation of 16.65, indicating considerable dispersion around the mean, ranging from −50 to 25. This result aligns with the findings of [5], who also reported a negative reaction in developed markets, though to a lesser extent than observed in the Brazilian context.

The ME had a mean of −28.40, a standard error of 6.43, and a standard deviation of 30.17, indicating high dispersion around the mean, with values ranging from −100 to 25. The CE was negative, with a mean of −17.04, a standard error of 6.45, and a standard deviation of 30.26, also indicating high variability in the observations, which ranged from −75 to 50.

The WE also presented a negative result (−10.22), with a standard deviation of 21.35 and a standard error of 4.55, indicating wide variation in the evaluations around the mean, which ranged from −75 to 25.

In general, investors, the market, clients, and workers reacted unfavorably to the disruption of the conventional initiative. Thus, the results show that stakeholders demonstrated a negative perception of the discontinuation of this initiative.

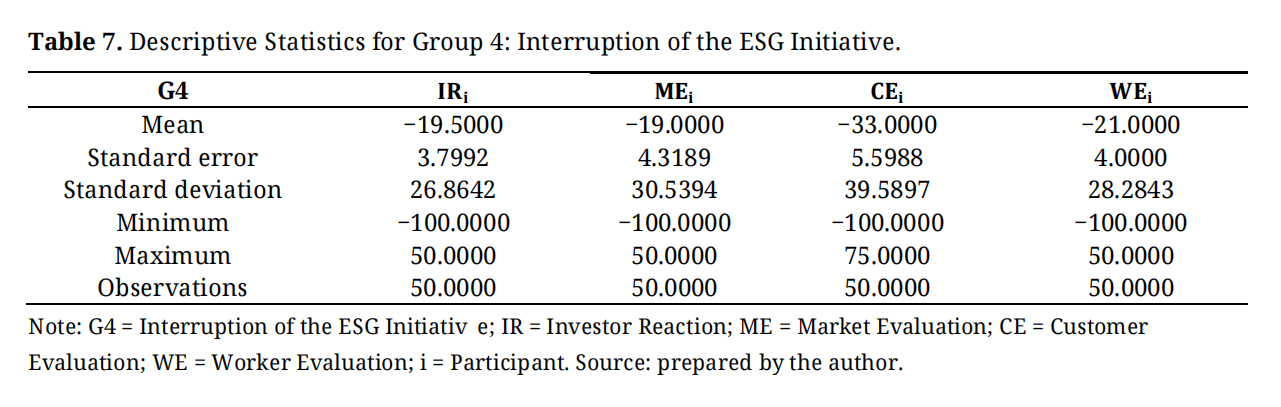

Descriptive Analysis of Group 4: Interruption of the ESG InitiativeGroup 4 includes the experiment participants subjected to manipulation related to the interruption of ESG initiatives, specifically the project involving bags made from organic material. Thus, Table 7 presents the descriptive statistics of Group 4, including mean, standard error, standard deviation, minimum and maximum values, and the total number of observations.

Regarding the experimental group that received an interruption to the ESG initiative, the final sample consisted of 50 participants. The mean IR was negative (−19.50), with a standard error of 3.79 and a standard deviation of 26.86, suggesting substantial dispersion in responses. These findings are consistent with previous studies, which showed a negative average reaction in developed countries [5,6,28]. In addition, investors reacted more negatively to the interruption of ESG initiatives than to the interruption of conventional business initiatives, suggesting that they attribute greater importance to the indirect benefits of ESG practices, a finding that differs from Group 2, where participants attributed greater importance to the direct benefits of conventional business projects.

Table 7. Descriptive Statistics for Group 4: Interruption of the ESG Initiative.

Table 7. Descriptive Statistics for Group 4: Interruption of the ESG Initiative.

ME presented an average of −19.00, with a standard deviation of 30.53 and a standard error of 4.31, indicating high variability around the mean, with values ranging from −100 to 50. It is observed that the market reaction was less negative to the interruption of ESG initiatives than to the interruption of conventional initiatives, suggesting that the market reacts more intensely when an initiative that generates direct monetary returns for the company is interrupted.

CE presented a negative average of −33.00, with a standard deviation of 39.58 and a standard error of 5.59, evidencing high variability, with values ranging from −100 to 75. Customers’ reactions were more negative toward the interruption of ESG initiatives than toward the interruption of conventional initiatives, indicating concern about the indirect benefits that ESG practices provide to society, in addition to their ethical and social responsibility character [5]. Finally, WE had a negative average of −21.00, with a standard deviation of 28.28 and a standard error of 4.00, showing high dispersion around the mean, with values ranging from −100 to 50. The workers’ reaction was more negative to the interruption of ESG initiatives than to the interruption of conventional initiatives, suggesting that, for employees, ESG practices are more relevant than traditional initiatives.

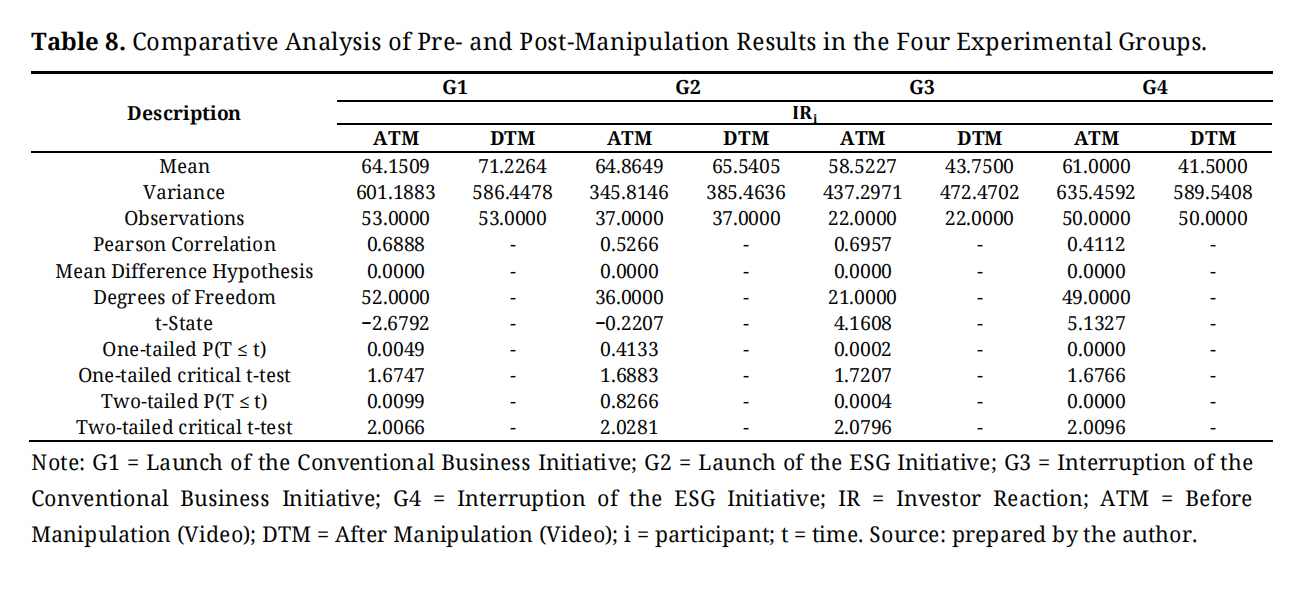

Mean Tests: Pre- and Post-Experimental ConditionsThe purpose of the mean test is to determine whether there is a statistically significant difference between participants’ responses before and after the experimental manipulations, considering both conventional and ESG initiatives, as well as interruptions to these initiatives. In this context, Table 8 presents the results of the student’s t-test for dependent samples, which compares the means of the pre-(ATM) and post-(DTM) manipulation conditions for each experimental group, including information on variance, number of observations, Pearson correlation, t-statistic, critical value, and p-value.

The results show that in Group 1, the launch of the conventional business initiative, IR increased significantly after manipulation, as indicated by t = −2.6792 and p = 0.0099, rising from 64.15 to 71.23 points. This result demonstrates a positive effect on investors’ perception, converging with the findings of [5]. Thus, the findings suggest that investors react positively to conventional business initiatives, assuming that businesses are responsible for generating profits [5].

Regarding Group 2, the launch of the ESG initiative, the average IR varied from 64.86 to 65.54, a difference that was not statistically significant (t = −0.2207; p = 0.8266). This result indicates that the launch of ESG practices did not alter Brazilian investors’ reactions, contrary to the previous study by [5]. The literature suggests that investors may not respond positively to ESG initiatives, as they entail costs for the firm. At the same time, the same capital could be invested in an initiative with the potential for direct profit or in one destined for the distribution of profits and dividends to shareholders [37].

Table 8. Comparative Analysis of Pre- and Post-Manipulation Results in the Four Experimental Groups.

Table 8. Comparative Analysis of Pre- and Post-Manipulation Results in the Four Experimental Groups.

Although the findings for Group 2 do not align with the studies, the neutral reaction to ESG practices aligns with those of [15,21,22].

On the other hand, the groups related to interruptions presented opposite results. In Group 3, where the conventional initiative was interrupted, the average IR decreased from 58.52 to 43.75, a statistically significant difference (t = 4.1608, p = 0.0004), indicating a negative investor reaction to the interruption and aligning with the literature [5]. This action may signal to the investor a lack of strategic alignment or effective business planning, suggesting that the firm made decisions that did not strengthen its core activities or generate economic value [6].

Also, regarding Group 3, stakeholders may interpret the event as an indication of management inefficiency, since the capital invested in the interrupted initiative could have been allocated to a more profitable and lasting project [41]. Regarding the interruption of ESG initiatives, Group 4 showed an average decline from 61.00 to 41.50, indicating a highly significant difference (t = 5.1327, p < 0.000) and a strong negative impact on investor reaction. This finding aligns with the research by [5,28].

The results of Group 4 suggest that investors tend to attribute importance to ESG practices because they are associated with ethics and moral responsibility [5], the reduction of the company’s cost of capital [42,43], the improvement of economic and financial performance [14,44], and the prediction of shareholder returns [19]. Thus, the findings show that the interruption of an ESG initiative can lead investors to interpret that the company will lose such benefits, which can be reflected in the market and, consequently, result in the devaluation of shares and the loss of capital, since ESG criteria create value for the organization [45].

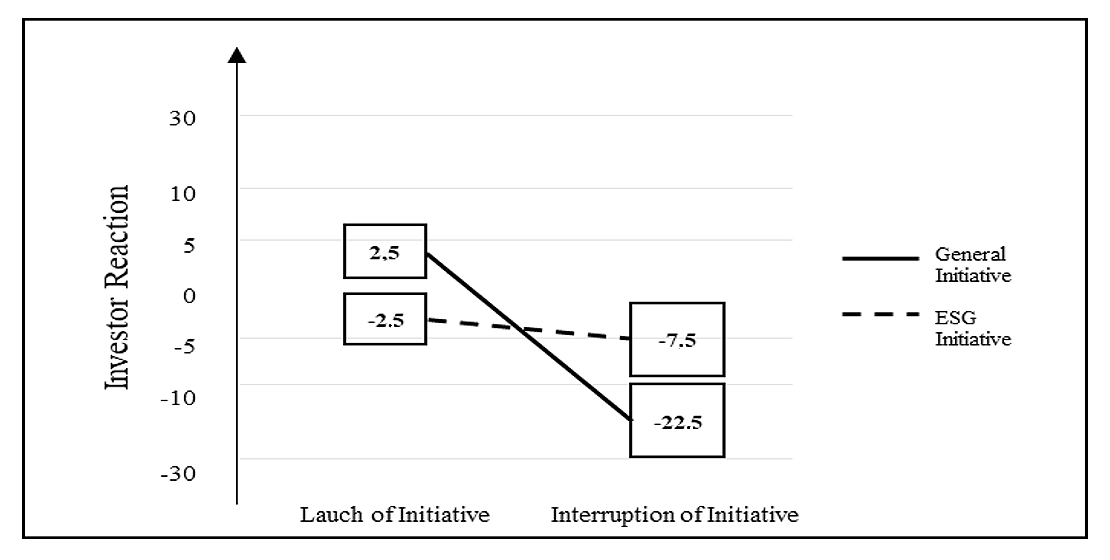

Figure 1 presents the results of the research hypothesis test, graphically illustrating investors’ reaction to the launch of conventional and ESG initiatives, as well as to their interruptions.

Analyzing Figure 1, it shows that although during the launch of the ESG initiative the investor reaction was discreet or close to neutral, the interruption of this initiative elicited more intense negative reactions, even greater than those observed in the interruption of conventional business initiatives. Based on these findings, it is not possible to reject the research hypothesis, corroborating the literature [5,26,33].

It is important to note that the experiment used a 2 × 2 design, with different participants allocated to distinct experimental conditions. In this type of design, everyone evaluates only one specific scenario, without exposure to the other conditions of the experiment. As [46] (p. 1) observes, “In a ‘between-subject’ designed experiment, each individual is exposed to only one treatment”. Consequently, evaluations conducted in each treatment occur in isolation, without a common reference point across scenarios. From this perspective, due to this methodological characteristic, differences observed between the means of distinct conditions should not be interpreted as direct comparisons between the scenarios evaluated by the participants, but rather as specific average effects of each treatment [46]. Thus, cross-comparisons between conceptually distinct scenarios, such as the project launch and project interruption scenarios, are not appropriate, as they reflect evaluations conducted by independent groups in distinct cognitive contexts and without a common reference [46]. Therefore, the study’s inferences focus on differences between treatments within each experimental context, rather than on absolute comparisons between scenarios evaluated with independent samples [45].

Figure 1. Results—Hypothesis Test 1.

Figure 1. Results—Hypothesis Test 1.

The results indicate that the announcement of the launch of general business initiatives generated a more intense positive reaction from investors (14.62) when compared to the launch of ESG initiatives (0.68), diverging from the study by [5], who did not identify a significant difference in the launch of ESG initiatives and general business initiatives. We found an explanation for this result in the study by [12], which shows that investors tend to assign less weight to social responsibility information when it is evaluated alongside traditional financial information.

In this context, ESG initiatives may elicit more moderate positive reactions, as investors often weigh their potential social benefits against the possible economic costs of implementing these practices [12].

Furthermore, the moderate behavior observed in the reaction to the launch of ESG initiatives can also be interpreted in light of [4] findings. The authors demonstrate that performance in social responsibility can unintentionally influence investors’ estimates of fundamental value [4]. However, when individuals explicitly evaluate this information, the effect tends to become less pronounced [4]. Thus, in the experimental context, participants may have recognized the potential value of ESG initiatives but reacted more cautiously to their initial announcement.

On the other hand, the results also indicate that the interruption of ESG initiatives generated a more negative reaction (−19.50) than the interruption of general business initiatives (−14.77). This finding is consistent with the evidence presented by [5]. According to [28,5,34], investors tend to react more negatively when companies discontinue ESG initiatives than when they discontinue traditional business projects, as such decisions can be interpreted as signs of reduced organizational commitment to ethical and social values.

Furthermore, the study by [28] demonstrates that investors attribute positive value to sustainability-related attributes, as evidenced by the greater flow of resources directed towards investments classified as sustainable. In this sense, when a company discontinues an ESG initiative, investors may interpret this decision as a deterioration of the organization’s sustainability strategy, which can contribute to a more negative reaction [28].

Additionally, evidence indicates that indicates that good ESG performance mitigates the risk of stock price crashes by curbing both earnings management and corporate risk [24]. Thus, the interruption of these initiatives can be perceived as an indication of potential future loss of value, which helps explain the intensity of the negative reaction observed in the scenario of discontinuation of ESG initiatives [4].

Recent empirical evidence also indicates that news about ESG performance elicits significant market reactions [19]. This study shows that negative news about ESG and CSR performance is associated with adverse reactions in stock prices [4,19]. This result provides further support for interpreting the strong negative reaction observed when ESG initiatives are interrupted in the context of the experiment.

Although most of the findings of this study align with the literature [5,26], some results diverge from previous research on the importance of ESG practices. Silva et al. (2024) [21] identified a negative and significant relationship between ESG practices and market value; Macedo et al. (2022) [47] did not identify a significant association between ESG practices and the cost of capital; and La Torre et al. (2020) [48] observed that ESG practices do not affect investor reaction.

Therefore, the results suggest that launching conventional initiatives results in a significant increase in investor reaction, whereas launching ESG initiatives does not. Regarding interruptions, both conventional and ESG initiatives experience significant drops in investor response, with the impact more pronounced for ESG initiatives. These findings show that investors value the continuity of sustainable and traditional practices, reacting more adversely to the discontinuation of actions than to the launch of initiatives themselves, corroborating previous results [5,29,34].

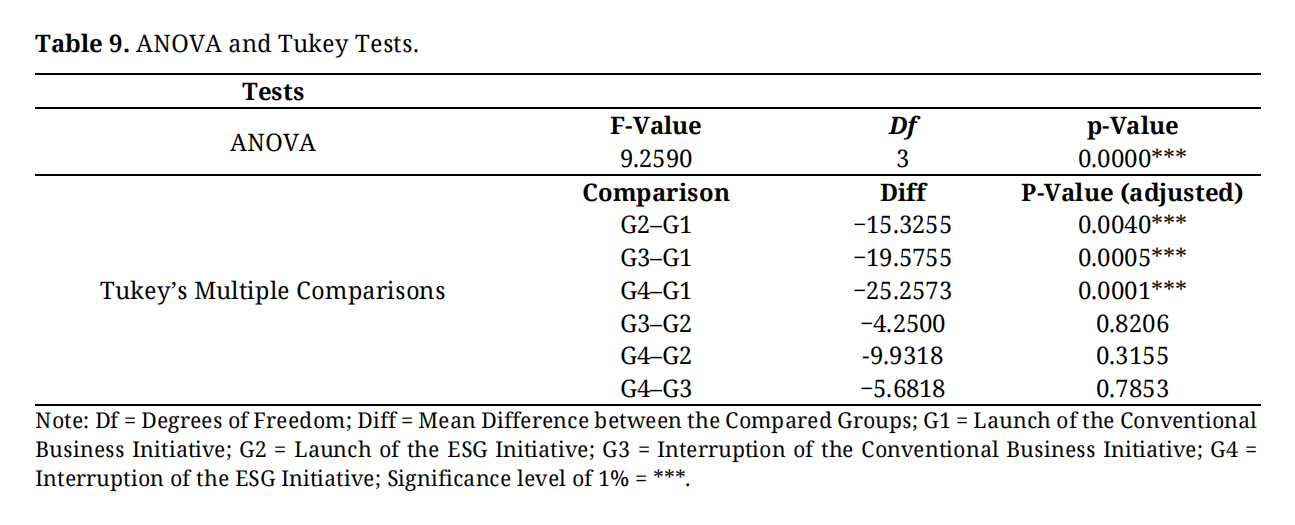

Mean Tests Between Experimental GroupsTo increase the robustness and reliability of the findings, we performed an analysis of variance (ANOVA) to test for statistically significant differences between the groups. Furthermore, we used Tukey’s test to identify which pairs of groups showed significant differences. Therefore, Table 9 presents the results of these tests, including the statistical test values, degrees of freedom, group comparisons, differences, and respective p-values.

The results presented in Table 9 reinforce the consistency of the research findings, as they show a statistically significant difference between the groups analyzed. The ANOVA test revealed an F-value of 9.2590 and a p-value < 0.0001. This result indicates that at least two groups differ significantly.

Table 9. ANOVA and Tukey Tests.

Table 9. ANOVA and Tukey Tests.

Tukey’s test allowed us to identify which group showed a statistically significant difference. The findings demonstrated that G1 differs significantly from the other groups, G2, G3, and G4. This evidence corroborates the results presented in Section “Mean Tests: Pre- and Post-Experimental Conditions”, which showed that only G1 showed a significant positive reaction. These differences indicate that the average of G1 is statistically distinct from the averages of the other groups, suggesting that conventional launch affects the analyzed variable differently than other initiatives and interruptions.

Regarding the comparisons between groups G3–G2, G4–G2, and G4–G3, no statistically significant differences were observed, as the adjusted p-values remained above 0.05. These results indicate that the means of these groups are statistically similar, suggesting comparable effects between the experimental conditions. In this context, the evidence aligns with the findings presented in Section “Mean Tests: Pre- and Post-Experimental Conditions”, which found that the reaction to the launch of the ESG initiative is almost neutral, whereas interruptions of both conventional and ESG initiatives elicit negative reactions of similar intensity.

Therefore, the ANOVA and Tukey tests reinforce the validity of the results, as their evidence converges with the findings presented in the Mean Tests: Pre- and Post-Experimental Conditions section of this research.

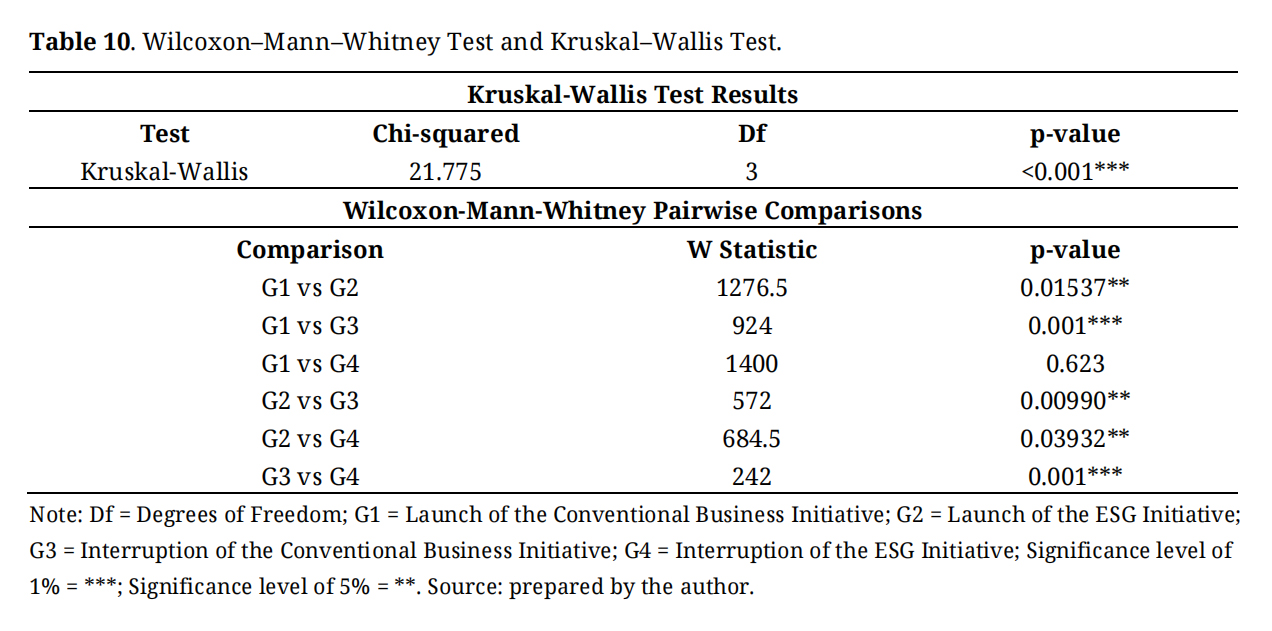

Robustness Test Between Experimental GroupsTo validate the robustness of the findings, we employed non-parametric tests—Kruskal-Wallis and Wilcoxon-Mann-Whitney—as robust alternatives to the primary parametric test. The results presented in Table 10 align with the main research findings, corroborating the conclusions’ efficiency and efficacy.

Table 10. Wilcoxon–Mann–Whitney Test and Kruskal–Wallis Test.

Table 10. Wilcoxon–Mann–Whitney Test and Kruskal–Wallis Test.

The Kruskal-Wallis test revealed highly significant differences across the four experimental groups (χ² = 21.775, df = 3, p < 0.001), confirming the ANOVA results (F = 9.259, p < 0.001) presented in Table 9. This convergence between parametric and non-parametric methods strengthens the validity of the findings and indicates that observed differences between groups are not artifacts of distributional assumptions. Pairwise comparisons via Wilcoxon-Mann-Whitney revealed that G3 (Interruption of the Conventional Business Initiative) showed significant differences relative to both G1 (Launch of the Conventional Business Initiative; W = 924, p < 0.001) and G4 (Interruption of the ESG Initiative; W = 242, p < 0.001), aligning with differences observed in the Tukey test. These results reinforce the reliability of statistical inferences and validate the robustness of the experimental design.

The objective of this research was to investigate, through an experimental design, investors’ reactions to interruptions in ESG projects compared to interruptions in general business projects, accounting for the life cycles of both initiatives.

The experiment used a 2 × 2 design: Initiatives (ESG/Conventional) × Decision (Start/Stop), with these as independent variables. In our approach, we separated participants into four groups. Group 1 referred to the manipulation of the launch of the general business initiative, involving 75 individuals. In Group 2, the manipulation was the launch of the ESG initiative, with 57 participants. In Group 3, the manipulation involved interrupting the general business initiative, with 38 participants. Finally, Group 4 conducted the manipulation of the ESG initiative interruption, involving 61 individuals. The final sample, after data cleaning, consisted of 162 participants, of whom 69 were excluded because they did not meet the investor qualification criteria or did not adequately understand the experimental procedure.

The analyses included pre- and post-manipulation mean tests to capture investors’ reactions, as well as an ANOVA to determine whether there was a significant difference in their reactions. The results suggest that investors may react more positively to the launch of conventional business initiatives, which could indicate that they perceive such initiatives as potentially capable of increasing financial performance and, consequently, generating greater returns for shareholders, whether through the distribution of profits, dividends, or equity interests.

Regarding interruptions, investors reacted more negatively to ESG initiatives than to conventional business initiatives. This result allows us not to reject the research hypothesis. The behavior may be explained by the perception that the resources invested in ESG projects were wasted and could have been allocated to conventional initiatives, which are more closely linked to generating shareholder value.

Furthermore, in the case of ESG initiatives, discontinuing them may also provoke additional negative reactions due to the ethical and socio-environmental responsibility expectations associated with this type of project, leading investors to perceive the discontinuation as a sign of inconsistency in the company’s commitment to sustainable practices.

In addition, investors may be concerned about the signal sent to the market and to stakeholders (customers and employees), since companies with strong ESG practices tend to have lower capital costs, lower earnings management (higher-quality earnings), and better performance than companies that do not adopt sustainable practices. Thus, by interrupting an ESG initiative, the company may lose market value and credibility with its target audience, face higher financing costs, and incur greater political costs. Added to this is the possibility that the investor may weigh their own ethical and moral responsibilities in the face of an interruption to an ESG initiative.

The main test, conducted through the experiment, allowed us to observe a potential relationship between the interruption of an ESG initiative and investor reaction, not rejecting the research hypothesis. The robustness tests are in line with the main tests, increasing confidence in the results of the primary analyses.

The study contributes to contemporary literature, as there is no record of previous experiments with this objective in Brazil, encompassing participants from different states (São Paulo, Bahia, and Sergipe), thereby potentially expanding the scope for generalizing the results. Furthermore, since this is an experimental study, we inferred potential causal relationships, suggesting that the interruption of an ESG initiative may provoke a negative investor reaction. However, when this interruption is duly justified and valid by the market and customers, the reaction tends to be less unfavorable. These findings may be valuable to market analysts, investors, and companies, as they can help them understand how investors may react to decisions related to ESG and conventional initiatives, potentially contributing to more informed assessments of strategic communication, reputation management, and resource allocation.

From a practical standpoint, the results suggest that companies should consider that interrupting an ESG initiative may negatively affect investor perception and, consequently, reduce the firm’s perceived market value. However, transparent and properly substantiated communication of the reasons for the initiative’s interruption, through reports, conferences, and explanatory materials, can potentially help mitigate the negative impact, especially when the company can demonstrate to the market and customers the economic or strategic rationale for the decision.

For market analysts, the findings provide potentially relevant insights, as monitoring initiatives and interruptions may improve investment recommendations and potentially increase portfolio profitability and accuracy.

Despite the contributions, the research has limitations. The results cannot be generalized to the entire national territory, as we tested only three Brazilian states. In addition, the sample size (162 participants) may affect the robustness of the results. There is also the possibility of adverse selection due to information asymmetry among the investors who participated in the experiment. The non-probabilistic sample and the application in controlled environments may have restricted the variability of the results. Furthermore, the regional and cultural characteristics of Brazil, as well as the fact that the experiment addresses only one economic sector, limit the generalizability of the findings.

Another limitation of the research concerns the possible fragility of the pre-test administered to students in the last semester of the Accounting Sciences course. Some of the participants did not understand all the questions, which may have influenced the answers obtained in the experiment.

As a suggestion for future research, the study should be replicated in other Brazilian states with a larger sample. Future research could also explicitly analyze the role of corporate justifications for interrupting ESG initiatives, verifying whether they mitigate or reverse investors’ negative reactions. Another approach is to include the ethical and moral dimension of the investor as a moderating variable in the relationship between interruption and reaction. In addition, experiments involving companies across different sectors can determine whether investor reactions vary by sector.

Data will be available from the corresponding author (MS) upon request.

All authors contributed to the preparation of the article mentioned above. MS and CC wrote the first version of the article. Independent applicators collected the data. AP and SG were supervisors and assisted in the review and drafting of the last version. All authors read and approved the published version of the manuscript.

The authors declare that they have no conflicts of interest.

This research was funded by the Bahia State Research Support Foundation (FAPESB) and the National Council for Scientific and Technological Development (CNPq: https://www.gov.br/cnpq/pt-br).

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

Silva M, Pereira A, Cunha C, Gomes S. Brazilian Investors’ Reactions to the Interruption of ESG and Non-ESG Projects: An Experimental Analysis. J Sustain Res. 2026;8(3):e260065. https://doi.org/10.20900/jsr20260065.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions