Location: Home >> Detail

J Sustain Res. 2021;3(2):e210010. https://doi.org/10.20900/jsr20210010

,

Tensie Whelan

,

Tensie Whelan

Center for Sustainable Business, New York University Stern, 44 West 4th Street, New York, NY 10012, USA

* Correspondence: Tracy Van Holt, Tel.: +1-212-998-0226.

This article belongs to the Virtual Special Issue "Corporate Sustainability"

Background: Fifty years ago, Milton Friedman first published his famous article in the New York Times—“The Social Responsibility of Business is to Increase Its Profits”. We explore the evolution of an extensive field of business management research that for 50 years has been devoted to examining that proposition. Today we find researchers exploring how embedding sustainability in corporate operations and business models can yield multiple business and societal benefits such as improved employee engagement, supply chain management, and reduced pollution. Stronger corporate sustainability has the potential to drive better management and performance and, as such, is emerging as a significant body of research for academics and practitioners alike. Findings of this research are also important because they may influence many corporate leaders who currently believe that adopting sustainability measures is too costly (i.e., reduce profitability) and not mission critical. Research across the social, economic, political, and business disciplines has been quite siloed to date. Business and sustainability scholars are just beginning to help each other analyze whether and how businesses can deliver on their sustainability goals for people and Earth. Our analysis highlights key thematic areas of research in the business literature. We also explain the disciplinary differences in the meanings and measurement of fundamental ideas including the scope of “governance”, who counts as “stakeholders”, and what elements to consider in conceptualizing “systems” relevant to business and society. Our analysis identified major topical areas for future collaboration among the disciplines, and how recognizing the diverse understandings of key terms listed above may unlock new synergies among researchers.

Methods: We apply a novel quantitative bibliometric network (an author citation network analysis), text analysis, and semantic network analysis of 65,000 academic articles on sustainability issues from 1960 to 2015.

Results: Foundational concepts were formed around 1995, and by 2006 empirical studies helped shape the field. Early research explored corporate social responsibility approaches such as philanthropy, stakeholder capitalism, and corporate environmental impacts. Research today is focused on how sustainability is embedded into business operations and research on purely environmental issues or philanthropy has diminished. Sustainability is a cohesive area of research with four main dimensions and 12 sub-clusters of research: (1) Management dimension (leadership, global ethics, shared value sub-clusters); (2) Performance (environmental, social, and governance [ESG] impacts, organizational, financial); (3) Marketing (attitudes, employees, brand/reputation); and (4) Strategy (supply chains, competitive systems, creating value).

Conclusions: Companies that embed a sustainability core to business strategy are likely to perform well due to consumer, supplier, and employee engagement, reduction of risk, and improved operational management, among other factors. However, holes remain in the research, and we suggest new frontiers for academics and practitioners. This requires prioritizing understanding human and environmental systems, rather than the firm as the focal point of research.

CSR, corporate social responsibility; ESG, environmental, social, and governance; KPIs, key performance indicators; CFP, corporate financial performance; SSCM, sustainable supply chain management

Just 10–15 years ago, few companies had dedicated sustainability or CSR officers. None had embedded sustainability functions into core business operations such as the supply chain. Generally, the only stakeholders referenced in annual reports were shareholders and employees. Other stakeholders, such as the producers who sourced the raw material, were not considered integral to the business. Corporate environmental efforts were often limited to complying with laws and regulations. Social issues were limited to a few topics such as community relations and philanthropy. Governance issues were focused more on firm governance and less about global governance challenges. A company’s performance on these efforts was self–reported, with little third-party assurance.

Today, the transparency brought by social media, the growing impact of environmental and social issues on company operations, and increasing expectations of business by stakeholders, have caused companies and investors to recognize sustainability as a strategy that is core to business. Social and environmental issues such as the global pandemic, climate change, and diversity and inclusion are increasingly seen as relevant to everyone’s lives. Indeed, businesses are becoming important actors in driving sustainability initiatives as they discover multiple strategic and management benefits. The sustainability performance of firms is now tracked by multiple ESG data providers and there is third-party auditing and certification to verify performance. Investors are increasingly including ESG data in their decision-making. With this rapid pace of change, has academia been researching what matters? How do academics build on these recent developments to identify relevant research questions for future work? How can sustainability and business scholars work together? Finally, in a world where global environmental and social challenges such as climate change and inequality are taking center stage, how can academics best work with companies to improve and measure corporate sustainability performance?

DefinitionsCSR/Sustainability/ESG. The term CSR has evolved during the period of research. Originally, CSR referred primarily to philanthropy, good community relations (in a general sense), and employee engagement activities. While many researchers and companies still use CSR in that sense, it has evolved to a more holistic meaning—one where stakeholders are emphasized over shareholders, and corporate performance is assessed on environmental, social, and governance metrics. The challenge is that companies and academics use both definitions interchangeably today. Sustainability and ESG (which refers to environment, social, and governance issues) are more specific, though they are also subject to differing interpretations. Sustainability includes economic sustainability, as well as ESG; ESG only refers to non-financial metrics. As sustainability truly becomes embedded into core business operations, even these labels may disappear, because today’s sustainability strategies may be just how companies operate tomorrow. Our keyword and semantic network analysis document the changes in words affiliated with CSR, sustainability, and ESG. In this article, we use the term sustainability to describe strategy and practice as it includes both CSR and ESG (which is usually used by investors). We use ESG when we are describing specific ESG metrics that are being tracked or reported.

(1)

(2)

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

We used “big data” and bibliometric analysis to trace the evolution of the field of corporate responsibility to systematically identify the core structure of the discipline, key research clusters, the evolution of sustainability and specifically ESG issues in academia, and what may be missing. This is a novel approach to develop future research questions, as we didn’t selectively or identify a priori which themes were relevant, but let the data—that is, a synthesis of authors’ citations of other works—speak for themselves. This is a different approach than, for example, Bansal and Song’s paper where they have also discussed the distinction between corporate sustainability and responsibility, and theoretical areas of overlap [2]. We did not derive the words or linkages based on our preconceptions, but rather the words and linkages were derived by how authors cited other authors. Dominant authors in the field have emerged via their citation networks. Bibliometrics help trace the evolution of a field, find coherent fields of inquiry, and identify clusters of research topics [3–5]. Bibliometrics open the possibility to systematically analyzing the relationships among 65,000 papers, which include not only the direct papers in the Web of Science (WoS), but the citations in the bibliographies of those papers, which may include articles that were not originally indexed on the WoS. We analyzed these data through a citation network that we used to identify key time periods and thematic clusters. We then tracked broad topical changes through word frequencies and semantic networks during key time periods. Next, we identified key thematic areas and research through a cluster analysis, which we used to identify future research topics.

(1)

(2)

(3)

(4)

To cast a wide net and account for the multiple terms associated with sustainability, we searched the following terms on the WoS Core collection in July 2016: TS = sustainab*, “ESG”, “social responsibility”, “shared value”, “social impact”, “impact investing”, “social entrepreneurship”, “social entrepreneur”, “social innovation”, “integrated reporting”, “triple-bottom line”, “green marketing”, “green market”, “sharing economy”, “conscious capitalism”, and “socially responsible”. These terms were limited by the WoS subject SU of Business and Economic and include the following document types: articles, books, book chapters, editorial material, letter, proceedings, and reviews. This resulted in 29,084 unique articles. We downloaded the articles as well as the bibliographies that were coded in the WoS database, resulting in ~65,000 articles. We chose this approach, rather than selecting sustainability more broadly, since businesses have become more prominent actors in sustainability. Additionally, Business and Economic papers often have much higher citations than those in other sustainability fields such as geography, anthropology, and ecology, for example. Papers from these fields were not excluded. They would be connected via the bibliographies. Even the top scholars in socio-environmental sustainability fields did not appear as key papers in this network.

Analysis Cohesive areas of researchTo identify cohesive areas of research (Q1), we ran a cluster analysis on a citation network derived from the WoS. First, we processed the WoS records using CitNetExplorer Version 1.0 [6] to analyze the citation patterns through time (from 1960 to 2016). In CitNetExplorer, we created an acyclic, directed citation network where each edge in the network represents the relationship between two publications (the model is constrained so that a 2015 publication cannot cite a 2016 publication for example) and this directed network begins with the citing publication and ends with the cited publication (see [4] for further explanation of the CitNetwork model). Each publication was given a citation score that represents the number of citations that the publication received in the entire citation network.

We then ran a cluster analysis on the adjacency matrix of the citation network—the primary cluster analysis of the citation network, setting a minimum threshold of 100 articles in the cluster analyses because we were interested in broad research trends. This is a square matrix with each element equal to either 0 or 1. If element (i,j) of the matrix equals 1, this means that publication i cites publication j. These clusters were categorized in broad terms to describe, in general, the content of the clusters. This is visualized in Figure 1, and the four unique clusters—that is, four main thematic clusters of ESG were identified.

Identifying key time-periodsTo identify the key time periods (Q2), we visually examined the structure of the network, and read the articles from the citation network in Figure 1. The first key year was 1995, because key theories about corporate responsibility were developed at that time. Articles prior to 1995 were more focused on general business topics. The year 1995 also had more citations in the visualization, implying that it was a pivotal point in the discipline. The next key year was 2006, about 10 years later, when a number of review studies were published, and the research moved beyond mainly theoretical constructs. The third period, 2015, we considered relevant to capture recent trends and was the last complete year of articles that we obtained.

Evolution of Sustainability ThemesTo see how the topics have evolved over time (Q3), we analyzed the keywords of the top 100 articles (identified by the number of citations) for each key year (identified above—1995, 2006, and 2015) by a word frequency analysis and a semantic network analysis. We obtained the keywords by extracting the available abstracts and/or book summaries, when possible. We created a content dictionary by eliminating the nonessential words that included stoplist words such as “and”, “but”, etc., that are typically used in content analyses and other words relevant to research (e.g., theory, data, analyze, etc. that were not relevant to our topical inquiry). We were interested mainly in nouns as it is more challenging to analyze emotion, etc. [7]. Then we grouped together like terms (i.e., stakeholder and stakeholders were recoded to stakeholder, etc.). We created n-grams, that is, multiple words that typically go together by coding “corporate social responsibility” as “corporate_social_responsibility”, rather than three separate words “corporate”, “social”, and “responsibility”. Finally, we also coded for and included any acronyms that we found. The same content dictionary was applied across all years. For the word-frequency analysis, we analyzed how frequent the words were for each year. We sized the words by their frequency for each year (Figure 2). For the semantic network analysis, we used Automap [8]. In Automap, we first preprocessed the text using the content dictionary, rhetorically eliminating other words, and then used a window size of seven, which has been determined sufficient in other studies to see which words were linked together in sentences [9]. Here the visualization shows which words co-occurred in each of the three years (Figure 3).

Data-driven topics for future researchTo identify data-driven research topics (Q4), we further divided the four main thematic clusters of sustainability (i.e., the four clusters that emerged from the primary cluster analysis of the citation network). For each of the four thematic sustainability clusters, we ran an additional cluster analysis (minimum cluster size set at 100) to further identify sub-clusters, which we described in detail. We chose this iterative approach, rather than initially clustering 12 clusters at the onset, because we wanted to verify that our clusters made sense, and this also helped to identify four broad themes for the field. Each of the four thematic sustainability clusters (the top 100 articles) were then visualized according to their sub-clusters, and we qualitatively analyzed the abstracts and key articles for sub-clusters to relevant, dominant topics that were cited often within the discipline.

To identify future research questions, first we summarized the content for each sub cluster. We qualitatively traced the evolution of key works and explained how they were linked. Then for the four major clusters, we identified research topics that captured both the key most recent trends, as well as possible causal linkages.

The field is well developed, as evidenced by four main thematic clusters of sustainability (see [10] for examples of non-cohesive research). The four main thematic clusters of sustainability focused on management, marketing, strategy, and performance (Figure 1). Management (blue) represents the heart of the theoretical development of why corporations should manage beyond the shareholder alone. Performance (orange) is mainly focused on assessing which companies engage with sustainability factors, how those are defined, and how sustainability can affect financial performance. Strategy (purple) explored which strategies are key for sustainability factors to become embedded inside business. Marketing (green) represents how consumers can influence companies to engage in sustainability, and how companies that engage in sustainability influence consumer perceptions. The management (blue) cluster is literally in the center of it all and has more linkages to other clusters. The articles by Milton Friedman clearly begin the research discussion as they are cited by many of the researchers. There is less integration across clusters; for example, there are fewer connections across marketing, strategy, performance, and marketing clusters.

Figure 1. Four thematic areas have emerged—management, performance, strategy, and marketing. The foundational theoretical concepts began to take shape by 1995, and in 2006 empirical studies helped the field to evolve into specialized fields.

Figure 1. Four thematic areas have emerged—management, performance, strategy, and marketing. The foundational theoretical concepts began to take shape by 1995, and in 2006 empirical studies helped the field to evolve into specialized fields.

Much research addresses making the business case for why companies should do good (see Figure 1). This is, in part, because the foundational articles in the early years (’60 to ’94) were often written in response to Milton Friedman’s work [11] that states that companies must manage for shareholder value and not include other stakeholders or societal needs (see [12] for a sample response). Most papers, especially in the earlier years, focused on whether engaging with society detracts from financial performance. In that period, articles focused on business operations and explained why sustainability issues were relevant for business, though they stopped short of providing a financial business case [3–16]. In the mid-1990s, sustainability concepts were theoretically developed, though they were not referred to as sustainability at the time and instead were often focused on general social responsibility or specific environmental issues. These works often fell short of systematically operationalizing and evaluating these concepts. At this time, the field began to be influenced by the growing global policy focus on environmental and social issues related to corporate behavior. From 2005 onward, we begin to see empirical studies that applied the theoretical concepts developed earlier, still focusing on the business case for companies engaging with sustainability factors. By 2015, studies began to address how engaging with sustainability provides value and focused on how to create the most meaningful sustainability engagement (i.e., embedding sustainability within core business functions).

Evolution of Themes Associated with CSR and SustainabilityThe word-frequency analysis showed that environment, performance, and sustainability have been central components of research across all years analyzed (Figure 2). In 1995, environmental aspects focused on pollution and being green, a term that referred to a niche market. Today, managing for pollution or being green is a given, and expected, so these keywords do not appear prominently in more recent years (2005 and 2016). The terms social and stakeholders began to emerge in 2006. Today, sustainability appears much more frequently, and generally refers to environmental, social, and stakeholder aspects of sustainability. We also see evidence of core businesses operations discussed as accounting and employees emerged as keywords in 2015.

Figure 2. The most frequent words for each time period are shown. Larger-sized and darker-shaded words mean that the word occurred more frequently.

Figure 2. The most frequent words for each time period are shown. Larger-sized and darker-shaded words mean that the word occurred more frequently.

The semantic network analysis (Figure 3) showed that the terms synonymous with CSR and sustainability have changed. The term CSR was absent from the 1995 network, CSR emerged in 2006, and by 2015, it was central and co-occurred with firm and performance. ESG only emerged in 2015, and the term was peripheral in the network. Over time, the term CSR co-occurred with more terms associated with terms emphasizing embedded dimensions—e.g., strategic, sustainability behavior, social economic, and organization, which built on 2006 co-occurring terms marketing and supply chain. Sustainability in 2015 co-occurred with many other themes (to a high degree), which was a big shift from 1995, where sustainability was only tied to three concepts (CSR, ecological, and organizational) and was peripheral in the network (low degree). In 1995, the terms regulation and polluting co-occurred with firm and environment, and today those words do not even appear in the semantic network, perhaps because it is expected that companies follow regulations and do not pollute. Instead of regulation, reputation appeared in 2005, signaling that reputation is influential in driving CSR. Reputation and risk have become more central in 2015, and in 2006 reputation and brand emerged in comparison to 1995 when risk was peripheral, and reputation and brand were absent. In 1995, social responsibility was discussed in terms of ethics, rather than core business. In 2006, stakeholders become central in the semantic network. In 2015, governance and global responsibility emerged, though they are still peripheral in the network. Design and transformations emerged in 2015, and these terms refer to system-level thinking about businesses and how companies think about sustainability.

Thematic Areas of ResearchWe describe each of four main thematic clusters of sustainability (Figure 3), and their associated sub-themes (Figure 4).

ManagementManagement (Figure 1, blue) had three sub-clusters—shared value, global ethics, and leadership (Figure 4a, blue, green, and purple nodes, respectively).

Shared value. The shared value approach has taken center stage in the management cluster. Shared value [17,18] postulates that companies create economic value by addressing societal challenges, and is a central concept related to embedding sustainability into core business practices. The shared value work builds on the idea that stakeholder theory is a management philosophy that incorporates attitudes, structures, and practices, essentially strong governance, rather than a description of stakeholders of a firm [16] and testable propositions that explain how stakeholder influence creates variations in corporate financial performance (CFP) [19]. The shared value idea is a direct challenge to Friedman’s foundational work [11], where he argued that companies should manage for solely for shareholder value. Over time, the conversation has shifted from responding to Friedman’s thesis by explaining or questioning why companies should get involved in managing for anything other than shareholder value [20] to papers discussing how the shared value approach is the way forward, though how each firm engages with shared value is still an area of research [17].

Figure 3. The semantic network visualization shows the co-occurrence of words (nodes here), that is, words that were discussed together in the abstracts analyzed. Words in the center are more frequently discussed with other words. Larger sized nodes have higher degree centrality, that is, these words have more connections with other words (which can also be seen by the direct ties).

Figure 3. The semantic network visualization shows the co-occurrence of words (nodes here), that is, words that were discussed together in the abstracts analyzed. Words in the center are more frequently discussed with other words. Larger sized nodes have higher degree centrality, that is, these words have more connections with other words (which can also be seen by the direct ties).

Figure 4. The four main thematic clusters—(a). management, (b). marketing, (c). performance, and (d). strategy-- have well developed sub-themes, shown as different clusters here.

Figure 4. The four main thematic clusters—(a). management, (b). marketing, (c). performance, and (d). strategy-- have well developed sub-themes, shown as different clusters here.

Global ethics. Today, corporations are viewed as globally responsible actors and potentially active drivers of governance and democracy [21,22]. This role of corporate citizenship became defined in this cluster [23]. Research is now focusing on how external actors’ affect organizational change (e.g., how NGO pressure influences organizations to be more responsible) [24,25]. These new areas build on foundational work about organizational processes and drivers of institutional change within organizations [15,26,27], which now is being applied to problems outside the firm.

Leadership. Leadership today takes a broad vision of leadership within the firm and is moving beyond the leader–follower relationship. For example, Maak and Pless [28] emphasized that leadership is really an interaction with many stakeholders inside and outside the corporation, and it isn’t necessarily the predominant leader–follower relationship as seen in previous research. In another example, Waldman et al. [29] examined broad cultural reasons for CSR leadership in a cross-cultural analysis across 500 firms in 15 countries; they show that when leaders came from a country where institutional collectivism is common, the managers valued many aspects of CSR (the study had multiple CSR dimensions), while in those cultures where power differentials were expected, all dimensions of CSR were devalued. Of course, today’s perspectives on leadership rely on earlier work that focused on ethical decision-making at an individual level. These include works that examined ethical behavior by individuals through the lens of moral decision-making [30]; person–situation models [31], and decisions as they relate to individual factors, the organization, and opportunities for action [13]. Today’s vision of leadership includes people across all areas of a company, not just the C-suite, and still has its roots in basic decision models [30].

MarketingMarketing (Figure 1, green) had three sub-clusters—brand, ethical consumers, and employees (Figure 4b, blue, green, and purple nodes, respectively).

Brand. Today, the brand cluster focuses on long-term relationships with ethical customers and strategies that are well matched with the brand. This builds on earlier work that characterized customer attitudes about responsible corporations. Customers resonate best with genuine responsibility initiatives [32] that are proactive [33] and aligned with the company’s core business strategy [34,35]. This reinforces consumer trust, positively affects consumer attitudes, and generates long-term loyalty [36–38]. Initiatives that are not well matched with the brand negatively influence customer perceptions of the company [33]. In addition to loyalty, companies can more easily bounce back after a negative crisis, which typically harms brands [39]. This recent research on responsibility initiatives shows improved awareness, image, credibility, brand feelings, community, engagement [40], and identity [41]. Earlier research described cause-related marketing [42], marketing in general (i.e., perceptions of price, quality, and value) [43], the value of brands [44], marketing that builds trust and relationships [45], social marketing and non-economic criteria [46], and the relationship between charity donation and social marketing [47].

Ethical consumers. The ethical consumers cluster today takes a broad, holistic vision of the ethical consumer, and research is focused more on experimental targeting, rather than descriptive characteristics of ethical consumers as in the past. For example, companies that focus on mindful consumption consider not only the environment and economics, but also the well-being of the consumer [48]. Marketing is also being used to reduce consumption and promote healthy lifestyles [49]. To target the ethical consumer, research has shown that people perceive ethical products as “gentle” rather than “strong” [50]; ethical consumption can be related to personal expenditures, certainty, social norms, and perceived availability [51]; and people are driven by status to buy green products, but only when shopping in public and when green products cost more [52]. This builds on earlier work that focuses on basic demographics and measures of ethical consumers [53] and describing the field, in general [54]. Ethical consumers believe that they can solve environmental problems, are morally driven [55,56], and may be willing to pay more [57], an assertion that is challenged as well [58]. Environmental attitudinal scales [59] and whether consumers care about being ethical or not [60] were also earlier topics in this area of research.

Employees. Today, the employee cluster is focused on employees in the firm. Employees working for socially responsible companies have a stronger commitment to the firm [61,62] that is of equal or greater importance than job satisfaction [63]. Employees identify more with companies that have developed responsibility programs, rather than just CSR affiliations [64]. Companies with developed responsibility programs also attract employees [65], talented ones [66], and this provides a competitive advantage [67]. Today’s work draws on earlier research focused on the relationship between employees’ social identity and organizations that employ them, in the general sense [68–70].

PerformancePerformance (Figure 1, blue) has three sub-clusters—organizational, ESG, and financial (Figure 4c, blue, green, and purple nodes, respectively).

Organizational. The organizational cluster includes the benefits of embedding some sustainability activities within structural features within the firm. For example, higher board diversity has been shown to positively affect reputation [71] and firm value [72]. Firms with extensive sustainability efforts (i.e., more embedded) had more transparent, high-quality financial reports [73]. When social auditors and ethical indexes were in place, stakeholder engagement activities withstood managerial turnover [74]. This builds on work examining the structural features of the firm and corporate governance in general, and includes studies about how the separation of ownership influences control [14,75], and agency costs (i.e., the cost of interactions) [76]. Topics also include board capital structures, which affect resources and monitoring [77], and how ownership concentration affects legal protection of investors, corporate shareholders and creditors [78,79], and corporate finance and takeovers [80].

ESG. Overall, the ESG-cluster focused on the non-financial ESG measures, their validity, what causes companies to disclose these measures, and the linkage to financial performance. Disclosures today are comprehensive in that they report on performance with respect to non-financial environmental, social, and governance issues [81–83]. While the validity of ESG disclosures are increasing, researchers question the persistence of social issues focused on corporate and employee issues alone, rather than broader social issues in areas where companies operate and among their suppliers, for example [84]. This concern is reinforced because reporting has been shown to be not “good enough” for key stakeholder groups [85]. While these ESG measures or social accounting as Gray [81] calls it, goes beyond economic accounting, the field still struggles with its place in the accounting field [81], likely because companies often do not calculate the financial value of sustainability actions. Research has shown that there is financial value to ESG measures. ESG disclosures reportedly provide reputational benefits [86] and Bebbington et al. [82] lay out the linkage between reputational risk, ESG measures, and corporate financial performance. ESG disclosures improve analyst forecast accuracy [83], indicating that these disclosures likely give insight into a company’s vision as well as their financial performance. The type of reporting depends on firm governance [82], and third-party assured reports are not always more prevalent [87] and likely are more prevalent in companies with embedded sustainability. The roots of disclosure is in legitimacy theory—i.e., what is the socially acceptable company behavior [88,89] and how this links to risk and reputation [90].

Financial. More recent work focused on accounting-based financial measures may help resolve the debate of non-financial ESG factors impact corporate financial performance. For example, high sustainability engagement (measured by disclosure, engagement, other social stock indices etc.) was related to raising more equity capital and lowering cost of capital [91,92], because sustainability-focused programs were associated with lower risk [93,94]. The evidence is mixed when using market-based measures, and this debate is likely to persist until ESG and CFP measures have higher content validity (i.e., they are relevant to the content measured), and sustainability performance is monetized. For example, sustainability has been linked to higher firm value [94,95] and higher rates of return [96–98], but then no difference was found for stock and mutual fund returns in traditional comparisons [99,100], when risk-adjusted [96,101] or when evaluating excess returns [102]. The argument that the content validity of CFP measures are flawed is supported by evidence that investors are willing to accept suboptimal financial performance [50,103] and negative stock returns [104]; corporate governance and social screens yielded lower risk-adjusted returns [103]. Clearly, there needs to be more work because differences also depend on the types of screens used [105,106]. This work is built on, and is entrenched in, research on performance in general, of mutual funds [107], stocks and bonds [108], and ethical investment funds [109], which focus on market-based measures.

StrategyStrategy (Figure 1, purple) has three sub-clusters—competitive systems, supply chains, and creating value (Figure 4d., blue, green, and purple nodes, respectively).

Competitive systems. The competitive systems cluster today identifies that today, to be competitive in the sustainability space, companies need to think more broadly (e.g., think beyond the firm itself, embrace stakeholders, and think on longer-term time scales). While many of the findings in sustainability management studies are similar to traditional management research, one unique feature in solving sustainability challenges is how the firm interacts and works with stakeholders [110]. Research shows that the companies that move beyond compliance and operational efficiencies, and those thinking as business systems—are beginning to plan in the longer term, especially when they engage with stakeholders [111–113]. In fact, it is the external stakeholders who are pushing for changes that go beyond operational efficiencies [113], and employees who are encouraged by the organizational structures and supervisors to implement sustainability strategies [111]; both institutional pressures and organizational characteristics drive sustainability adoption [112]. Sustainability today is seen as driving many advantages including market access, differentiated products, improved risk management, and lower costs, among others [114,115]. Interestingly, though, there are few financial tools to measure these advantages. This is in comparison to earlier works where being eco-efficient and avoiding pollution costs may have saved money, but this didn’t necessarily translate to market access and innovation, for example [116–119]. Early works discussed proactive firms, which really are the precursor to embedded sustainability. Proactive companies were shown to view stakeholder relationships as more important than firms that were not proactive, but rather compliance driven [120]. Proactive firms also were shown to have different organizational capabilities that allow them to develop ways to integrate stakeholders, and have deeper learning and continuous innovation [121]. All this work has its roots in the idea that pollution prevention, product stewardship, and sustainable development leads to competitive advantage [122].

Creating value. Creating value through sustainability today is about identifying which material issues to tackle first, integrating this work into business models, and identifying best management and measurement practices [123,124]. Central are Hart and Milstein’s ideas about creating sustainable value through the dimensions of shareholder value: innovation and repositioning, growth path and trajectory, cost and risk reduction, and reputation and legitimacy [125]. Approaches to create value include engaging peripheral stakeholders to foster disruptive change that leads to imagination and new business models [126], and tapping into multiple types of capital—economic, natural, and social [127]. This builds on earlier work that examined the strategies sustainability champions employ [128], and how successful strategic sustainability initiatives are aligned with company values [129]. Finally, this work builds on the triple bottom line [130], environmentally centered business models, [131], and models that link humanity, morality, and nature [132].

Supply chain. Sustainable supply chain management (SSCM) is moving towards integrating social, environmental, and economic issues [133,134] though even today the environmental focus still dominates [135]. SSCM requires more coordination across the chain including suppliers as well as retailers, but also among different functional departments of the firm (e.g., purchasing, marketing, and distribution) [136]. There is evidence that value is being created in SSCM [137]. Indeed, today SSCM goes beyond the organizational boundaries [138], includes subsidiaries and offshore suppliers [139], and considers production, consumption and post-consumer use [140]. Companies need structural changes, for example, in management structures and training, to adopt and diffuse SSCM practices throughout the supply chain [134,141]. Other structural changes include longer-term contracts and regular audits [139]. This is because, in part, SSCM requires new actions and structures that might run counter to traditional supply chain practices [142]. SSCM strategies can manage for risk, performance, or sustainable products, benefiting the company [133]. SSCM requires strong partnerships with suppliers and incentive systems [143] Collaboration across suppliers on similar problems in SSCM seems to benefit all [144], and an increase in competitiveness and economic performance has been shown in integrated green supply chains [145]. While external, rather than internal, factors seem to drive interest in SSCM [146]; this doesn’t always translate into actual adoption because while the environmental performance improves, the financial benefits are still questionable in some cases [147].

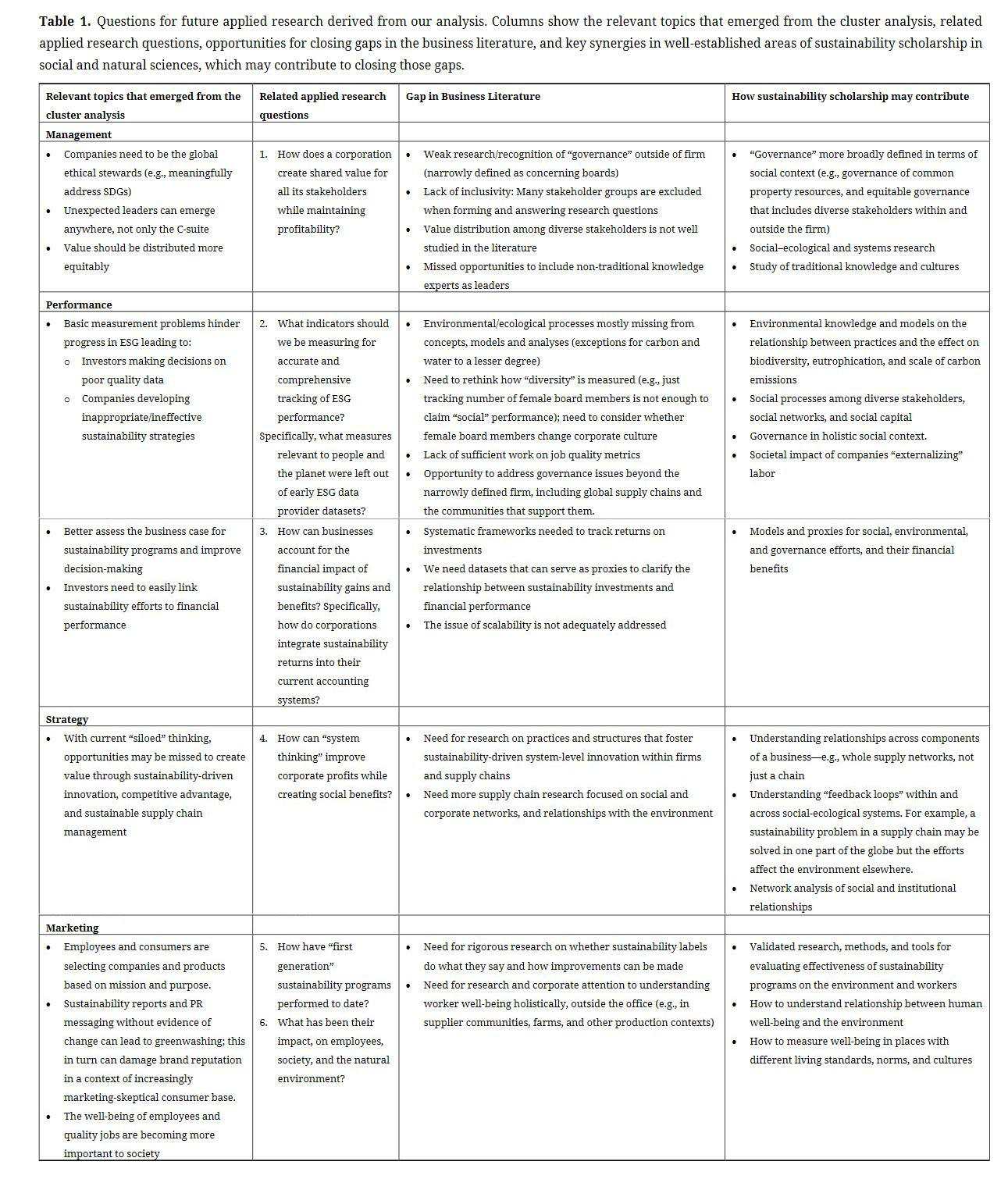

Future Research Questions: We identified key research questions that stem from our bibliometric analysis (Table 1). These questions and their relevance emerged from the research being done in the clusters of business sustainability scholarship. Building on those questions, we identify the research and conceptual gaps that need to be addressed, and how scholars focused on social–environmental aspects of sustainability can contribute to advances being made in that vein in the business literature. (Table 1). Key questions focus on more equitable distribution of value by companies amongst all stakeholders, improving measurement of ESG performance, integrating the financial impact of ESG into corporate accounting systems, bringing social–environmental systems thinking into business strategy, and understanding how well or poorly first-generation sustainability programs have performed for employees and customers and other stakeholders.

Table 1. Questions for future applied research derived from our analysis. Columns show the relevant topics that emerged from the cluster analysis, related applied research questions, opportunities for closing gaps in the business literature, and key synergies in well-established areas of sustainability scholarship in social and natural sciences, which may contribute to closing those gaps.

Table 1. Questions for future applied research derived from our analysis. Columns show the relevant topics that emerged from the cluster analysis, related applied research questions, opportunities for closing gaps in the business literature, and key synergies in well-established areas of sustainability scholarship in social and natural sciences, which may contribute to closing those gaps.

Seeing Diversity in How Scholars Define Key Concepts: We identified three key concepts that need clarification to unlock new collaborative possibilities among scholars studying social-environmental and business sustainability. These include the role of governance, stakeholders, and social–ecological systems.

Governance. Business scholars excel at understanding governance at the level of the firm. Practitioners consider governance at the firm level to be a key predictor of company success. But sustainability challenges can only be addressed by broadening the scope of the concept to include governance of both people and resources beyond the firm, beyond basic regulatory compliance, to include, for example, the formal and informal rules and norms that govern the behavior of suppliers and the use resources they depend on internationally. Companies are often setting up informal governance mechanisms in response to deal with weak governance by local and national governments wherever such matters affect their supply chains. For example, corporations and nonprofits have created informal governance mechanisms to tackle child labor in cocoa-producing communities. Informal governance has helped address concerns in seafood creating a policy and structure to prevent worker abuse and improve worker and community well-being, and improve environmental sustainability [148]. In addition, we need to be able to recognize that there are often pre-existing, sometimes complex systems of informal, traditional, and formal governance operating at local and regional scales where business has a stake, and that these may be working to improve or sustain natural resources. Much scholarship on common property and natural resource management addresses that [149–151]. Social–environmental scholars working on sustainability challenges across the globe study governance in this broader sense [152]. Business scholars have an opportunity to bring their expertise to the topic as well, which we argue is necessary if businesses are to meet their sustainability goals.

Stakeholders. Stakeholder research is a key area where business scholars on the one hand, and social–environmental sustainability scholars on the other, diverge in their understandings—and this has enormous implications for human well-being and ecological health. While there are research methodologies and business procedures on how to identify stakeholders, many legitimate stakeholders remain hidden to the business scholars. Social–environmental sustainability scholars dedicate the bulk of their research to stakeholders outside the firm—beginning with primary producers, communities, and distributors, NGOs, and governments—while business scholar center their efforts closest the firm (i.e., shareholders, employees, suppliers via third-party collaborations). Those left out of stakeholder engagements by businesses are typically the marginalized stakeholders that may include key producer actors in local communities are not central to designing the governance processes of the very products they harvest [148]. This has been observed when mapping supply chains (e.g., companies know very little about their supply chains beyond relatively superficial understanding of the first tier of suppliers) [153]. The interaction between “internal stakeholders” (the firm) and external stakeholders (throughout the supply chain and communities that support it) deserves far more collaboration and study. Some scholars even count the environment or biodiversity as a stakeholder [154].

Social–Environmental Systems: The last key area we identified with great potential for cross-pollination between business scholars and social–ecological sustainability scholars is to link social and environmental systems conceptually and in practice [155]. Social–environmental scholars have expertise studying connections, and “feedback loops” across social and environmental systems, often at multiple scales [156,157]. These linkages often reveal negative consequences of certain well-intended sustainability actions. For example, formalization of land tenure or work status of small producers can have unintended negative consequences if the environmental impacts are not also considered [158]. Business scholars understand economic systems but do not always understand the complex social–environmental issues that influence those systems. Indeed, recently management scholars are calling out the need for systems research, which will require adopting new theories and concepts, such as those outlined here.

Limitations of the analysisOverall, we provided empirically derived results from this citation network of 65,000 articles on sustainability. We took efforts to minimize bias in this approach toward synthesizing such as large volume of text.

1.

2.

3.

4.

The terms CSR and sustainability have evolved to entail more than environmental issues and corporate philanthropy. Today, non-financial ESG issues are routinely analyzed by researchers and sustainability has become more embedded in business practice. Social–environmental and business sustainability scholars need to work together so we can address key challenges of embedding sustainability into the four main dimensions of business operations: management, performance, marketing, and strategy.

We hope this paper stimulates a conversation amongst academics and practitioners about the evolution of research on sustainable business and drives further exploration of new frontiers in corporate sustainability research. We believe that research in this area will be useful to policymakers as they debate the role of business in society and explore how best to encourage pro-social corporate behavior. Finally, we hope business school educators will find this work of interest as they adapt curricula to address new risks such as global pandemics like COVID-19, climate change, and new opportunities such as innovation related to moving toward a low-carbon world.

All data generated from the study are available in the manuscript or associated supplementary files.

TVH designed the study with input from TW. TVH ran the analysis. TVH and TW wrote the paper.

The authors declare that there is no conflict of interest.

We thank Glen Dowell, Francis Milliken, Batia Wiesenfeld, the Academy of Management and Alliance for Corporate Research Alliance reviewers, and the anonymous reviewers for providing feedback on earlier drafts of this research. We thank Wendy Weisman for her valuable comments on a draft version of the manuscript.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

62.

63.

64.

65.

66.

67.

68.

69.

70.

71.

72.

73.

74.

75.

76.

77.

78.

79.

80.

81.

82.

83.

84.

85.

86.

87.

88.

89.

90.

91.

92.

93.

94.

95.

96.

97.

98.

99.

100.

101.

102.

103.

104.

105.

106.

107.

108.

109.

110.

111.

112.

113.

114.

115.

116.

117.

118.

119.

120.

121.

122.

123.

124.

125.

126.

127.

128.

129.

130.

131.

132.

133.

134.

135.

136.

137.

138.

139.

140.

141.

142.

143.

144.

145.

146.

147.

148.

149.

150.

151.

152.

153.

154.

155.

156.

157.

158.

159.

Van Holt T, Whelan T. Research Frontiers in the Era of Embedding Sustainability: Bringing Social and Environmental Systems to the Forefront. J Sustain Res. 2021;3(2):e210010. https://doi.org/10.20900/jsr20210010

Copyright © 2021 Hapres Co., Ltd. Privacy Policy | Terms and Conditions