Location: Home >> Detail

J Sustain Res. 2021;3(2):e210011. https://doi.org/10.20900/jsr20210011

Seeds of Opportunity, P.O. Box 1423, Blantyre, Malawi

This article belongs to the Virtual Special Issue "Corporate Sustainability"

The Sustainable Development Goals (SDGs) are calling for developing and developed nations to strive to end inequality, promote universal access to electricity and enhance climate change mitigation. However, ensuring that the SDGs can be achieved will require significant new investments from both the public sector and corporate sector. For example, it has been estimated that climate change adaptation costs in Africa may rise to above US$100 billion per year by 2050, hence likely surpassing the magnitude to which the United Nations Framework Convention on Climate Change (UNFCCC) processes can mobilise climate funds. There have therefore been urgent calls for the private sector and corporate world to provide additional financial and technical assistance for SDGs implementation at all levels. Some studies have shown that climate resilient development in any country is feasible provided that a range of market and policy failures are corrected; and new technologies, business models, and financial innovations are implemented. This paper therefore aims to improve awareness of SDG 7 and SDG 13 implementation modalities in the Global South in order to improve knowledge on which actions from the corporate sector can enhance the mobilisation of climate funds and accelerate SDG 7 and SDG 13 implementation through funds mobilised via conventional and non-conventional financing mechanisms. Through an exploratory analysis of various research articles, case studies, policy briefs and project reports it was possible to determine the policies that can enhance climate change mitigation and renewable energy deployment in developing countries through the corporate sector. The analysis concluded that Africa’s climate finance landscape lacks venture funds to stimulate climate change entrepreneurship and innovation hence corporate actors may augment SDGs and Nationally Determined Contributions (NDCs) implementation by initiating policies that can incentivise corporate actors to facilitate the development and implementation of climate change venture funds.

The Sustainable Development Goals (SDGs) and United Nations Framework Convention on Climate Change (UNFCCC) are two international frameworks that are calling for developing and developed countries to transition to low carbon climate resilient trajectories in order to mitigate and avert harmful climate change. This follows that climate change is considered as a global development challenge that is constraining inclusive development by increasing the frequency and intensity of climatic shocks through intense rainfalls, floods, droughts and prolonged dry spells [1]. Accordingly, some reports have pointed out that the frequency and magnitude of natural hazards triggered by climate change has been increasing globally, leading to US$1.5 trillion in economic damages from 2003 to 2013 [2]. Unfortunately, it has now been reported that the cost for adaptation are five times higher than previous estimates with the cost of adaptation in developing countries including countries in Africa estimated to be between US$280 and US$500 billion per year by 2050, suggesting that the cost of adaptation in Africa may rise above US$100 billion per year by 2050 [3]. This therefore means that while adaptation finance through the UNFCCC will help offset some climate change adaptation costs, it is not of the magnitude required for climate proofing [3]. Arguably, without new innovations to create new climate finance instruments and without new innovations to leverage private and public finance, climate change adaptation and ultimately the attainment of the SDGs will be unattainable in the Global South.

Sub-Saharan Africa (SSA) may be considered as a region that faces a “double injustice” in that while having contributed the least to global greenhouse gas emissions, the region will bear the brunt of climate change impacts, and at the same time have the least resources to cope and adapt [4]. However, paradoxically, whilst it might be envisaged that SSA would be in the forefront in initiating programmes aimed at promoting the adoption of technologies to mitigate future climate change since the continent has potential to undertake technological leapfrogging (i.e., undergo processes where a developing country can circumvent the resource-intensive and expensive form of economic development by skipping to “the most advanced technologies available, rather than following the same path of conventional energy development that was forged by the highly industrialised countries”), some research points out that the region is still investing in fossil fuel power systems that will lock the world into a high carbon path that would all but guarantee that the goals agreed in the Paris Agreement of keeping global temperature increases below 2 °C and of enabling communities to adapt to climate change will not be met [5,6]. Some of the factors that have led to the slow uptake of the implementation and scaling-up of climate change mitigation programmes and notable transitions to climate resilient development trajectories in SSA include a range of market and policy failures and a lack of finance/financial innovation [7,8]. Similarly, various climate finance mechanisms have been developed in order to augment the efforts of the UNFCCC to reduce greenhouse gas emissions but such climate finance modalities have not always been successful in incentivising investments from various crucial sectors due to their failure to consider how policy, regulations and institutional capacity affects intended outcomes [9]. Similarly, climate finance mechanisms such as the Clean Development Mechanism (CDM) were created to incentivise the private sector in investing in developing countries to promote sustainable development. However, some CDM projects have been criticised for perpetuating inequality by among other things having a strong focus on investments in particular countries and regions thereby adversely affecting the livelihoods of local communities [10]. With all these issues in mind, it might be argued that there are still some knowledge gaps on how the financial and technical resources from the corporate sector can be harnessed in order to improve the implementation of the SDGs more particularly SDG 7 (universal energy access) and SDG 13 (climate change action).

Some previous studies on the nexus of corporate sector financing and climate change in SSA include Kissinger et al. [11] who explored the potential of climate finance to support developing country efforts to shift away from unsustainable land use patterns in the context of the 2015 Paris Climate Agreement. Kissinger et al. [11] concluded that while much attention is directed to the inadequate quantities of international climate finance, a lack of fiscal reform remains a key hurdle to realise transformative change in the land use sector. Zhang and Pan [12] undertook an analysis of 160 NDC reports (covering 188 Parties) submitted to the UNFCCC Secretariat in order to determine the financial demand, mitigation cost and priority investment areas for developing countries. Their results indicated that in 2030 the total amount of financial demand for developing countries in response to climate change would be close to US$474 billion. Chirambo [13] assessed the roles businesses could play in supporting the implementation of the SDGs. Chirambo [13] concluded that microfinance institutions supporting small, medium, and micro-enterprises may be amongst the best options for the private sector to support all three elements of the climate change resilience, inclusive growth, and conflict prevention/resolution nexus in SSA. In a research by Sireh-Jallow [14], it was argued that even though Africa has various sources of non-conventional development finance mechanisms to replace and/or compliment Official Development Assistance (ODA) (i.e., diaspora bonds, remittances, carbon sequestration and trading, Islamic finance, etc.), many African countries do not use such mechanisms to finance development since African policy makers do not prioritise the use of non-traditional sources in their revenue diversification strategies. In a research by the World Bank [15], it was argued that even though crowdfunding/crowd-investing represents an easier way for entrepreneurs to access capital outside conventional banking systems, many developing countries still require to build an ecosystem that addresses the economic, social, technology and cultural challenges to the adoption of crowdfunding.

Despite the studies highlighted above and other similar research, SSA still experiences climate finance gaps hence it might be argued that there are still more opportunities for corporate sector activities to be improved so that they are better aligned to augment the financing of programmes for the Paris Agreement and SDGs. This arguably also means that there is still a need to deepen the understanding and awareness of how corporate sector activities can accelerate state actor and non-state actor actions that have a bearing on facilitating sustainable development in the context of SSA. Accordingly, to address these concerns and knowledge gaps, an exploratory analysis using various research articles, case studies, policy briefs and project reports was undertaken. The analysis focused on highlighting the status and implementation modalities of various public and private climate finance mechanisms and business models in order to improve knowledge and awareness on which actions from the corporate sector can enhance the mobilisation of climate funds and accelerate SDG 7 and SDG 13 implementation through funds mobilised via conventional and non-conventional financing mechanisms.

The paper is structured as follows: Section “METHODOLOGY AND CONCEPTUAL FRAMEWORK” follows with the paper’s methodology and conceptual framework. Section “ENHANCING NATIONALLY DETERMINED CONTRIBUTIONS (NDCS) IMPLEMENTATION THROUGH THE CORPORATE SECTOR” provides insights into the financial instruments that can support Nationally Determined Contributions (NDCs) implementation. Next, an analysis focusing on the complimentary roles that corporate actors in microfinance and financial intermediation can have in developing inclusive financial systems are presented in Section “THE RISE OF MICROFINANCE INSTITUTIONS AND FINANCIAL INTERMEDIARIES AS CORPORATE ACTORS FOR SUSTAINABLE DEVELOPMENT”. Thereafter, Section “CORPORATE CLIMATE CHANGE FINANCING IN AFRICA: THE CASE OF ETHIOPIA” highlights how green bonds through the corporate sector can complement ODA. Section “SDG 7 AND SDG 13 BUSINESS MODELS FOR CORPORATE ACTORS” provides three case studies on corporate sector led SDG 7 and SDG 13 business models. In Section “DISCUSSION”, the discussion focuses on highlighting the need for corporate sector actors to support SSA policymakers and investors to create venture capital funds for climate action in SSA. The paper concludes in Section “CONCLUSION” by highlighting the policies and strategies that can increase the impact of the corporate sector in SDGs and NDCs implementation in SSA.

In order to achieve the aim of this paper (i.e., to determine the policies that can enhance climate change mitigation and renewable energy deployment in developing countries through the corporate sector), an exploratory analysis using secondary data consisting of various research articles, case studies, policy briefs and project reports focusing on the nexus of climate change, private finance and renewable energy investments was undertaken. Since the research was exploratory in nature, the case studies provided in the paper were identified through purposive sampling. The case studies were not intended to provide a representative or statistical sample of best practice in renewable energy deployment and climate change adaptation business models in SSA, but rather to provide an indication of the different private sector led modalities that are available to state and non-state actors as solutions to SSA’s varied and complex challenges regarding strengthening local capacity for adaptation to climate change and increasing energy access. SSA’s climate change vulnerability is influenced by factors such as high poverty levels, poor infrastructure and low social resiliency [16,17] and access to renewable energy services is influenced by factors such as the efficiency of public utilities in expanding energy access and a lack of appropriate financial mechanisms to incentivise the private sector to invest in the energy sector [18,19]. Moreover, there are substantial variations in socioeconomic conditions between and within countries that entail the need for a spatially explicit localisation of vulnerable populations to define targeted interventions [20]. Consequently, rather than attempting to formulate a conceptual framework on how corporate sector actors can be organised to supplement public funding for the implementation of the SDGs, the paper focuses on theorising that supporting innovation and entrepreneurship in the corporate sector can improve access to, and utilisation of technology; and create new bespoke financing modalities thereby enabling national and regional actors to have access to resources for enhancing SDGs implementation more particularly SDG 7 and SDG 13. This approach is therefore anticipated to support conceptualisations that explain how entrepreneurship and innovation help in resolving the environmental problems of global socio-economic systems and how opportunities for creating new products, services and income sources are inherent in market failures [21].

Green finance, that is all forms of investment or lending that consider environmental effects and look to promote environmental sustainability [22], are considered as mechanisms that can facilitate climate change mitigation, adaptation and capacity building in different contexts, and as such support corporate actors and policymakers in their efforts to attain the aspirations of the SDGs and Paris Agreement. However, whilst there is a proliferation of institutions and modalities facilitating the development and utilisation of various green finance products and services, challenges still remain in ensuring that green finance significantly improves the implementation of SDGs in the Global South. For example, various forms of concessional and non-concessional financing mechanisms are available for climate change mitigation through the deployment of renewable energy. However, such mechanisms have not drastically changed the energy landscape in SSA as the region has an electrification rate of only 35% hence 80% of the population there relies on solid biomass for cooking and heating, and this leads to approximately 600,000 annual deaths in the region due to air pollution caused by the use of firewood and charcoal for cooking [23,24]. Additionally, ensuring that universal energy access (SDG 7) is attained will require Africa’s energy sector investments to increase from the current levels of about US$8 billion annually to an estimated US$41 billion to US$55 billion annually until 2030 [18,25]. With these considerations in mind, it can be seen that global and national corporate sector actors can have a significant impact in fostering new private sector led green finance business models that can simultaneously enhance climate change mitigation and renewable energy deployment in developing regions such as SSA.

Global South countries have numerous investment opportunities for local and international corporations. Accordingly, it has been suggested that SSA, South Asia, and East Asia & Pacific are arguably the three regions that present the most significant investment opportunities in both energy access and climate change mitigation [26]. For example, within the regions identified, India, South Africa, Mozambique, Cambodia, Mongolia, Uganda, Kenya and Rwanda are noted as countries that can deliver the highest impact per dollar invested both in improving the quality of energy access and delivering climate impact using renewable energy, and these countries alone can offer more than US$360 billion in investment potential in clean energy by 2030 [26]. However, it might be argued that climate change has the potential to simultaneously reduce the investment potential of these countries/regions and the potential for investors to successfully mobilise finances for investments in these countries/regions. In this regard, Espagne [27] highlighted that climate change is a systemic risk for local and international financial systems as it affects financial stability through the physical risk (i.e., impacts on the value of financial assets of climate events such as floods, storms, etc.); the liability risk (i.e., impacts of lawsuits by those who might have been victims of natural disasters that they would try to link to climate change, aimed at those deemed responsible for these changes); and the transition risk (i.e., the financial risk that would result from an adjustment to a decarbonised economy) [27]. Furthermore, even though to date, no sovereign downgrade by a major credit rating agency has been attributed to climate risks, it is probable that unmanaged risks of climate change may also negatively affect credit ratings and capital cost of countries which are least resilient [2]. With the aforementioned factors in mind, it might be argued that even though various corporations can harness the significant investment opportunities in developing countries to foster sustainable socio-economic development through sectors such as renewable energy and infrastructure, with increased climate change, corporate actors and developing countries might find it even harder to attract affordable private capital for hard infrastructure in various sectors due to unfavourable credit ratings and perceptions of climate risks on investments. In the light of these insights, it can be argued that one way of engaging the corporate sector in climate change related issues would be for local climate change policies and international climate change policies such as NDCs to start incorporating provisional financial climate risk management data. Through the incorporation of provisional financial climate risk management data it can be argued that NDCs will be aiding the decision making processes for corporate sector actors and will also be equally engaging and informative to investors and financial analysts since there will be initial analyses of a country’s climate change related systemic risks and transition risks on which investors and financial analysts can base their initial decisions on or form a basis for further analyses. More importantly, with this approach, all the programmes and projects included in the NDCs could have initial assessments which may provide stakeholders with an awareness of how a particular project/programme/investment might be affected by climate change and how a particular project/programme/investment could have an influence on reducing various climate risks for the country. This could turn out to be very important since some research shows that investors and financiers have challenges in understanding how to develop climate change projects and how to integrate climate data with investment data, and as such situations exists where climate change investments by corporate and public actors are guided by historical experiences and implementation risks rather than context and need [28,29].

Overview of Financial Sources and Intermediaries for Nationally Determined Contributions (NDCs) ImplementationMultilateral funds have a key role in facilitating sustainable development as they are channels for mobilising and disbursing development finance to corporate actors and national governments. However, even though multilateral funds are sources of climate finance, various factors have constrained the success of multilateral funds in promoting the implementation of climate change programmes through corporate and public sector actors in the Global South. For example, developing country stakeholders have often been resentful of programmes implemented through multilateral funds as they perceive them to reflect the priorities of international implementing institutions and the donors that fund them, rather than responding to their national needs and circumstances [9]. Similarly, developed country stakeholders have pointed out that many developing countries have weak governance systems and lack credibility hence drastically increasing financial flows to these countries does not guarantee that climate change funds will be used for the intended purposes [30,31]. These issues therefore suggest that developed country and developing country stakeholders have divergent perspectives regarding the type of reforms that need to be undertaken in order to engage actors from different regions and sectors to implement socio-economic programmes.

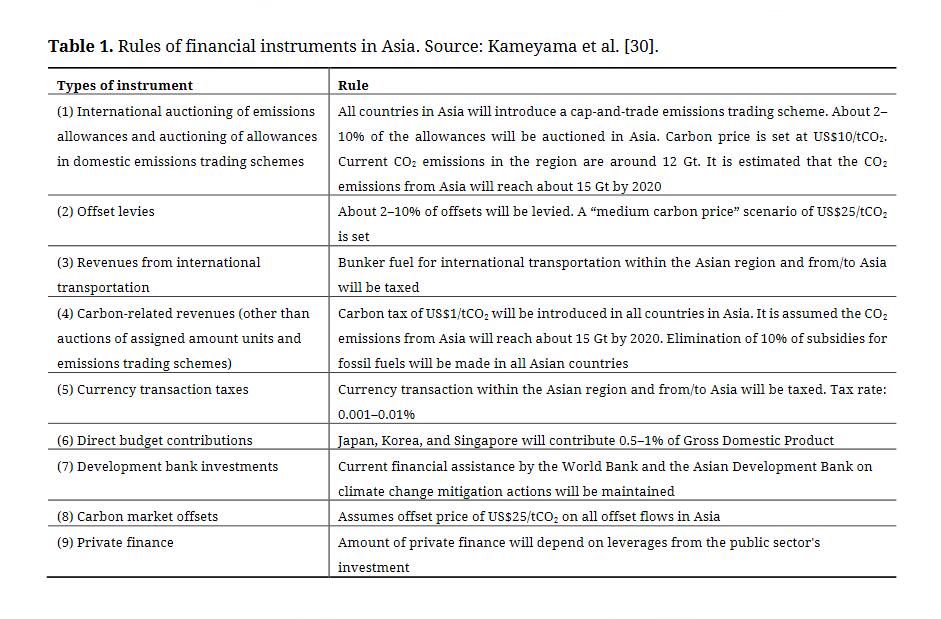

Globally, there are various strategies and financial instruments for mobilising funds to compliment ODA in supporting green investments and in augmenting NDCs implementation. For example, the redirection of fossil fuel subsidies, carbon market revenues, diaspora bonds, remittances, financial transaction taxes, export credits and debt relief [14,30] may be considered as emerging sources for increasing the cumulative value of climate finance hence corporate entities can collaborate with state and non-state actors to improve their structure, implementation and impact. To put things in perspective and to illustrate the magnitude of these funds, one can look at the potential value of carbon market revenues. In an assessment by Timilsina et al. [32], it was estimated that the potential carbon market revenues from CDM projects could attract US$158 billion of total investment to SSA and could generate US$7.5 billion of carbon revenue annually at an assumed carbon price of US$10/tC2. However, many countries in SSA have not been able to tap into the carbon market due to investor’s negative perceptions regarding the countries’ political and macro-economic stability and implementation of regulatory frameworks [33]. This therefore means that corporate actors and governments have to increase their efforts and collaborations to initiate and implement reforms that can improve the mobilisation of climate funds through various international climate finance instruments. Table 1 provides an illustration of various instruments for Asia that can be used to augment climate finance and their potential values. Whilst not all the instruments can directly be used or leveraged by corporate entities, it can still be argued that corporate actors can have an impact in their use and impact as they can accelerate their adoption and implementation by lobbying their governments and/or providing technical assistance to their governments to address the institutional challenges that developing country governments have in the climate finance domain. More importantly, even though table 1 has a focus on Asia, there is potential that SSA countries can implement similar instruments or some of the climate finance realised through such instruments in Asia can be transferred to SSA countries through South-South Climate Finance modalities. Ultimately, whether these financial instruments are implemented in Asia or SSA, there will still be a need for corporate actors to increase the impact of these instruments by ensuring that corporate actor led investments in renewable energy, infrastructure, etc. have synergies with climate change priorities as outlined in a country’s NDC.

Table 1. Rules of financial instruments in Asia. Source: Kameyama et al. [30].

Table 1. Rules of financial instruments in Asia. Source: Kameyama et al. [30].

Another area that corporate actors can help with, especially in the case of NDCs is arguably in helping to provide reliable cost or funding estimates for NDC implementation. As it stands, it might be argued that another factor that has potential to constrain some corporate actors from augmenting the effective implementation of NDCs is that many NDCs do not provide sufficient specific details related to mobilising and disbursing finance for their climate change programmes, and as such some corporate actors do not have precise information on how their contributions can be leveraged or utilised by state actors. For example, some NDCs (e.g., Togo and Guinea) provide details on funding required for the implementation of NDCs actions but do not provide an indication of possible sources for mobilising the required funds [34]. Similarly, other NDCs (e.g., Nigeria, Cape Verde and The Gambia) do not specify how much money they would need to finance the implementation of the actions outlined in their NDCs [34]. At a global level, the research by Zhang and Pan [12] showed that among 160 NDC reports submitted to the UNFCCC, 122 reports clearly included the finance content, 64 reports proposed specific amounts of financial demand for the implementation of the NDCs, and 31 reports pre-estimated the domestic amount and financial demand for greenhouse gas mitigation in 2030. The climate finance and NDCs implementation landscape is therefore disjointed as on one hand developing country and developed country actors and stakeholders have divergent perspectives on how the impact of climate finance and multilateral funds can be enhanced in developing countries, and on the other hand there are knowledge gaps in estimating the mitigation and adaptation finance demand for some African countries.

Lastly, having addressed the issues of improving the mobilisation of climate finance, there will also be a need to improve the transparency of NDC programme implementation for the benefit of private investors and donors alike. In this regard, most countries in SSA would benefit from implementing new standardised systems for tracking climate finance flows. For example, in the NDC for Chile, it was proposed that the government would establish new modalities for improving the development of local new climate financing modalities and procedures for tracking finance. The NDC for Chile therefore states that Chile will develop a National Finance Strategy for Climate Change which will (i) initiate a periodical climate change public spending analysis, (ii) create internal institutions which will allow to optimally manage and coordinate the relationship with the Green Climate Fund (GCF), and (iii) facilitate the designing of financial instruments which can be used for purposes such as adaptation and technology transfer [35]. Learning from this experience, it can be argued that if more developing countries followed suit and included new procedures and frameworks for enhancing the accountability of climate funds and programmes in their NDCs and green finance systems, the potential of NDCs framework to promote financial innovations and financial accountability would increase. This would then ultimately enhance the engagement of corporate actors in NDC implementation. Through this suggested approach of providing additional financial frameworks to support NDC implementation, it can also be envisaged that more corporate investors would be incentivised to promote the use of the financial instruments presented in Table 1 since the additional information provided in the additional frameworks has financial data that is more relevant to corporate actors than environmentalists.

Some reports indicate that the global allocation of climate funds in 2015 and 2016 stood at around US$409 billion/year whereby public finance actors and intermediaries committed an average of US$139 billion/year or 34% of total climate finance flows and private climate finance averaged US$270 billion/year [36]. From this amount it was estimated that SSA received US$12 billion, Middle East and North Africa received US$8 billion and East Asia and Pacific US$132 billion [36]. Furthermore, mitigation activities accounted for an average of 93% of climate finance between 2015 and 2016 and of that investment, 74% was for renewable energy generation [36]. Since a significantly larger amount of climate funds emanate from private capital, state and non-state actors need to work in synergy to increase the impact of climate finance in enhancing climate change resilience and sustainable development; and ensuring that a country’s fiscal and financial instruments, market-based instruments and regulations reduce investment risk while increasing investment return [37]. In the case of SSA, there is a mismatch between actual procedures/requirements for accessing most climate funds and the desired procedures/requirements to access such funds by the communities and institutions that require such funds, and this has an impact on the eligibility of the corporate actors that can develop and implement projects using climate finance modalities. For example, (i) businesses; Micro, Small and Medium Enterprises (MSMEs); and project developers in SSA need access to risk-tolerant or concessional smaller amounts of finance to kick-start or expand their projects and investments yet Multilateral Development Banks (MDBs) have a preference towards supporting large multi-million dollar projects, and (ii) MDBs lack appetite for innovation and risk yet significant transitions with greatest impact can only be achieved through investments in early stage projects/ventures which are usually risky [9]. Additionally, there have been calls to ensure that new modalities for accessing climate finance should have lower transaction costs and should be able to support a wider range of government, business, and community actors within countries. In this regard, it can be argued that the governance structures of MDBs limits the impact to which they can support emerging social enterprises and impactful business models through MSMEs and as such integrating inclusive and flexible financing channels such as microfinance into the climate finance and green finance landscape can help address some challenges related to improving the accessibility and utilisation of climate finance modalities.

As it stands, corporate actors in the microfinance sector have developed various programmes and business models aimed at facilitating poverty alleviation, agriculture development, disaster management and recovery, post-conflict recovery and gender equality [13,38,39]. Additionally, various targets of the SDGs such as Target 1.4 (ensure that all men and women, have equal rights to economic resources, as well as access to financial services, including microfinance) and Target 5.a (undertake reforms to give women equal rights to economic resources, as well as access to financial services) [40] suggest that there is a need to further increase the outreach of microfinance services in order to alleviate poverty, promote inclusion and reduce climate change vulnerability. Some researchers have therefore concluded that in developing countries and in poor communities affected by climate change, the plight of many individuals is linked to the ability of microfinance institutions to adapt to the consequences of climate change [38]. Microfinance is therefore not only a tool that can enhance climate change resilience but is also a tool that needs to be utilised by corporate actors to deliver innovative financial products that are inclusive so as to avert engendering the marginalisation of some communities.

Some traditional means of delivering climate finance include the use of loans, grants and equity through bilateral relations, Development Finance Institutions (DFIs) and MDBs. Some reports have indicated that through DFIs and MDBs in 2015–2016, market-rate loans were the main instrument used to finance climate change adaptation activities, for an average of US$11 billion per year; and concessional instruments like grants and low-cost loans typically provided by bilateral donors amounted to US$5 billion [2]. Outside the scope of such traditional financing modalities, there are also various non-conventional financing channels such as diaspora remittances and crowdfunding which are typically used to provide additional finances to households and communities but are now considered capable of being used to finance businesses and projects of various scales [15,41,42]. In the case of diaspora remittances, remittances to Africa were estimated to peak at US$500 billion by 2017, more than three times the size of ODA [43], with the share of international remittances to Africa amounting to nearly US$70 billion, about 3% of Africa’s Gross Domestic Product [44]. Furthermore, Africa’s migrants have the potential to provide more than US$100 billion a year to help develop Africa through such means as leveraging for low-cost project finance [45]. In the case of crowdfunding, the total crowdfunding market is composed of various subtypes, including lending (debt), equity, and royalty-based models, as well as non-securitized types, such as charitable donations and rewards crowdfunding. The global crowdfunding market was estimated at US$16 billion with the large market being in North America and Europe, and the African crowdfunding market totalling about US$70 million (less than half of 1% of global crowdfunding activity and about 21% of emerging market activity) [15]. With such sums of non-conventional finance being available for use for various personal and commercial uses, integrating such non-conventional finance mechanisms into the domain of climate finance and development finance can prove to be an indispensible asset in the fight against climate change since the climate finance domain has financing gaps (i.e., the costs of climate change adaptation in Africa may rise above US$100 billion per year by 2050 hence while adaptation finance through the UNFCCC will help offset some of these costs, it is not of the magnitude required for complete climate proofing [3]). Moreover, ODA related to development and climate change has been known to be unpredictable and not transparent. For example, ODA is not only determined by a country’s need/vulnerability but by factors such as good governance of the developing country and donors’ personal interests [4]. Similarly, previous official financial pledges (obligations) and agreements under the UNFCCC remain unfulfilled and this has resulted in significant financing gaps in many critical areas of the world [43]. These issues therefore highlight how important and crucial non-conventional financing mechanisms can become in reducing UNFCCC financing gaps and why more corporate entities need to be involved in the mobilisation and delivery of non-conventional financing mechanisms.

On the other hand, local banks in SSA have arguably been proven to be the corporate actors that are relatively weak and ineffective in their efforts to promote sustainable development through renewable energy deployment. For example, most banks do not provide the relevant instruments, such as risk guarantees and credit lines [46,47] to stimulate private sector led investments in the renewable energy sector and many commercial banks are dominated by short-term lending outlooks (i.e., it has been estimated that from 2010 to 2012, 49% of bank loans had a tenor of less than one year, and only 19% of loans in developing countries are over five years in duration) [26]. Arguably, most of the products and services from SSA’s local banks are not in keeping with the investment profiles for renewable energy supply systems as renewable energy infrastructure investments require large capital outlays at the beginning but then have lower running costs afterwards [18]. Fortunately, other corporate entities have noticed this market gap created by the banks and as such they have created crowdfunding platforms and financial intermediary institutions to act as alternative channels for mobilising finance to facilitate the implementation of green projects. In this regard, reference can be made to the work of Lelapa Fund which is a crowdfunding investment platform that connects global investors with African growth ventures [48]. Similarly, another private sector green finance mobilisation and delivery mechanism is through specialised financial intermediary institutions such as Sunfunder. Sunfunder is a San Francisco based organisation that mobilises financial resources from individuals and organisations in developed countries in order to provide such funds to off-grid/decentralised energy companies in the developing world on relatively affordable terms [46]. The business model for Sunfunder principally entails the company connecting investors to high-impact solar projects that improve the lives of low-income communities in Africa, Asia and Latin America. Sunfunder is reported to have improved access to energy to over 2.7 million people by providing investments of over US$20 million to enterprises related to solar lighting, phone charging, micro-grids and commercial solar projects [49]. Similarly, in South Africa, SCF Capital Solutions with support from the GCF established the US$34.15 million SCF Fund aimed at supporting MSMEs in the green economy to have a dedicated financing mechanism. In order to simultaneously ease the challenges related to access to finance and the cost of finance for MSMEs, the SCF Fund utilises Supply Chain Finance, a business model where business and financing processes are linked between the various parties in a transaction—the buyer, seller and financing institution—, and the financial institution avails credit to the supplier, based on the credit strength of the buyer, who would normally be a large entity with better financial records than the MSMEs. The SCF Fund is envisaged to create 30,660 new small, medium and large low-emission power suppliers and benefit 1380 women owned MSMEs [50]. Energy crowd funding platforms, financial intermediary institutions and MSMEs Green Funds are therefore new innovative routes that corporate actors can utilise to fill in the gaps by banks by (i) addressing the mismatches between the requirements of traditional financiers and typical needs of SSA’s project developers, and (ii) mobilising additional finance from formal and informal sources.

Unlike the Kyoto Protocol, which was a prescriptive top-down cap and trade system for limiting greenhouse gas emissions [51], the NDC framework is a bottom-up, country-led approach for improving climate change governance. Individual countries have therefore got more flexibility in the choice of fiscal and financial instruments, regulations and technologies that they can deploy in order to make an ambitious greenhouse gas emission reduction contribution in keeping with the Paris Agreement’s 2 °C target. Additionally, the World is experiencing significant changes in the way development is financed in that the global development finance landscape is changing, from a model centred on ODA and the coverage of remaining financing needs through external debt, to a framework with greater emphasis on the mobilisation of domestic resources [52]. Noting these changes, some authors have pointed out that ODA flows are not expected to grow from the current levels but rather decline and take on new competitive forms such as “blended finance” and “climate financing” [53]. Consequently, in order to adapt to these changes different countries have developed and implemented various other policies and mechanisms to enable them to successfully achieve their climate change targets and SDGs.

Ethiopia is a country located in the Horn of Africa in East Africa. Ethiopia is considered as one of the world’s poorest nations but yet it has developed an ambitious Climate Resilient Green Economy (CRGE) strategy that alongside a multi-sectoral Growth and Transformation Plan (GTP) aim for the country to leapfrog environmentally unsustainable development and bring the country to middle-income status by 2025 [54]. Since the country is embarking on a development trajectory that aims to achieve a high rate of economic growth without increasing the country’s greenhouse gas emissions, facilitating investments in its renewable energy sector are considered imperative for these development plans to be successful. Regardless of the perceptions about Ethiopia’s poverty, the Government of Ethiopia has shown ambition and innovation in seeking to mobilise climate finance from individuals and the corporate sector through green bonds. For example, the Government of Ethiopia issued the Renaissance Dam Bond in order to mobilise approximately US$6.4 billion for the construction of the 5,000 Megawatts Grand Ethiopian Renaissance Dam.

From a global perspective, the global bond market is worth around US$93 trillion [6], and from a regional perspective, at the end of 2011, total bond issuance from African economies totalled approximately US$1 billion but this figure had risen to US$6.2 billion by the end of 2014, with a total of 11 countries accessing bond markets to finance domestic expenditures [55]. On the other hand, green bonds- that is fixed income, liquid financial instruments that are used to raise funds dedicated to climate change programmes and other environment-friendly projects- are gaining in market share. The green bond market has grown from less than US$1 billion in 2007 to over US$41 billion in 2015 with over 80% of green bonds is¬sued going to climate-related infrastructure and energy efficiency projects [6]. Whilst the green bond market is only approximately 1.4% of the total bond market [56], the growth in the green bond market is encouraging since green bonds provide win-win situations for both investors and policy makers in addressing climate change as they provide governments with access to affordable and reliable financial resources in order to fulfil their commitments under the Paris Agreement and provide investors with investments that provide financial, social and environmental values. However, one of the challenges in the green bond market is that the green bond market is polarised in developed and emerging economies whereby China represented over 40% of the global green bond issuance in 2016, while regions such as Asia (excluding China) and Africa accounted for less than 6.5% of global green bond issuance in 2007–2016 [56]. From these figures, only US$2.2 billion of total flows in the green bond market have been directed towards cities in developing countries compared to US$17 billion in developed countries [56]. Nonetheless, Ethiopia is therefore one of the few African countries that has attempted to integrate green bonds in its national development financing mix in order to streamline the use of green bonds as a complement of ODA.

The experience of Ethiopia in the green bond market demonstrates that there is potential for green bonds to be used extensively by corporate actors in Africa to finance various projects with a bearing on climate change mitigation and hydro electric power projects in particular. This is encouraging as there is significant potential for the further development of hydro electric power in Africa (i.e., hydro electric power currently comprises 21% of electricity generation capacity in SSA, over 90% in, Ethiopia, Malawi, Mozambique, Namibia, Zambia, and roughly 39% in Tanzania; and 92% of the hydro electric power capacity in Africa is still unused [18,57]. According to Sireh-Jallow [14], one of the reasons why non-conventional development finance mechanisms do not easily gain popularity in Africa is that there are no institutional arrangements to allow different African governments to learn or build capacity from the countries that have successfully used different types of non-conventional development finance mechanisms. However, whilst ordinary development finance policies and strategies are country-led, climate change policies though country-led are international in perspective and as such have more scope for engagement and knowledge exchange between various countries and institutions. To put it in another way, it can be argued that there are less opportunities for countries to receive external support to build their capacity on reducing constraints to bond utilisation, whilst there are more opportunities for countries to receive external support to enhance their potential to utilise green bonds as for example there are various climate finance modalities that can support capacity building and international exchanges to enable countries to improve their capacity to mobilise finances for climate change programmes. Accordingly, policymakers in Africa may consider establishing an international forum or network focusing on creating institutional arrangements to facilitate capacity building on the development and use of green bonds in the region with Ethiopia and the other ten countries that have utilised the bond markets to finance domestic expenditures taking the lead. Moreover, since China has also shown great innovation and drive in promoting the use of green bonds domestically, and is also a significant donor towards South-South Climate Cooperation modalities (i.e., China’s NDC incorporates a pledge to provide US$3.1 billion (CNY20 billion) to establish the China South-South Climate Cooperation Fund [58]), there is significant scope that China can provide both technical input and know how on how different SSA countries can structure their institutions and projects to develop their green bond markets and also provide financing towards the establishment and operation of the proposed international forum/network for green bond development or the “African Institute for Green Bond Development.” Reference and parallels can be made to the establishment and objectives of the African Institute for Remittances (AIR). The African Institute for Remittances (AIR) is a specialised technical office of the African Union that focuses on reducing the cost of remitting money to and within Africa, and improving the regulatory and policy frameworks within which remittance transfers take place since remittance costs to and within Africa are about 12%, compared to 8% in other developing regions [44]. Accordingly, many of the benefits of remittance transfers are lost in intermediation and as such lowering remittance charges to and within Africa can increase remittance values by US$1.8 billion annually [59]. The African Institute for Remittances (AIR) therefore engages various stakeholders and countries in a bid to create an environment that can be characterised by lower remittance costs as this can also encourage more people to utilise formal remittance channels. Similarly, the proposed “African Institute for Green Bond Development” can focus on engaging various local and international actors to devise ways to improve the use of green bonds in the region since unlocking the potential of using green bonds for climate change infrastructure development in more African countries can enable corporate actors to leverage their finances for development projects. This can therefore ultimately reduce the budgetary and fiscal pressures that SSA governments have when trying to design and implement SDGs and NDC programmes.

Achieving sustainable development in the face of climate change will require innovation across a broad continuum, including technologies, deployment approaches and financing models, as well as capacities and institutions (including at the local level) [9]. This section therefore provides three corporate sector led business models that have an impact on the implementation of the SDGs in SSA. The case studies are not meant to provide comprehensive guidance on how corporate actors can design and implement SDGs and NDC related projects, but rather to provide an awareness of the approaches that some corporate actors have taken or can take to tap into various climate finance instruments.

Waste-To-Energy in Ivory CoastAfrica needs to drastically improve its access to modern energy to the extent that the current low rates of electrification in many African countries has been singled out as the most pressing obstacle to economic growth, more important than access to finance, red tape or corruption [60]. On the other hand, many cities in Africa are characterised by a general lack of sound municipal solid waste management systems due to challenges in the collection, transportation, disposal, and treatment of waste [61]. This dilemma has two implications. Firstly, it suggests that many African cities have environmental management problems as the waste is indiscriminately dumped at uncontrolled dumpsites and on river banks, street corners, passageways and the backs of buildings [61]. Secondly, it suggests that cities have challenges implementing SDG 12 (sustainable consumption and production) since a lot of waste that could be reused or recycled is not utilised. For example, the city of Cotonou (Benin) generates about 154,000 tonnes of waste per year of which only 8% is disposed of at the official landfill [62]. Furthermore, some reports indicate that globally cities generate over 1.3 billion tonnes of waste annually growing to 2.2 billion tonnes annually by 2025 [62], hence the uncontrolled disposal of waste can hamper efforts to attain sustainable development by adversely affecting human well-being and biodiversity. Notwithstanding the above issues, the use of Waste-To-Energy technologies can partly address Africa’s waste management problems, energy gaps and greenhouse gas emission challenges by facilitating the production of biogas which can be converted into electrical energy. Some studies have therefore estimated that Africa’s theoretical electricity production from biogas from waste could reach 27.5 Terrawatt-hour (TWh) in 2012 and 51.5 TWh in 2025 in comparison to a total electricity consumption of 661.5 TWh at continental level in 2010 [63].

Despite the numerous economic and environmental benefits associated with the deployment of Waste-To-Energy technologies, many local authorities in Africa have institutional capacity limitations (i.e., lack technical and planning expertise in waste management) and financial gaps to facilitate wide-scale investments in Waste-To-Energy technologies and waste management processes [64]. Noting this challenge, various private sector actors have therefore initiated various projects and business models based on providing Waste-To-Energy processes and services to cities. In this instance, reference can be made to the work of Soci Ivoirienne de Traitement des Dechets (SITRADE), a corporate sector actor that collects and treats 200,000 tonnes of Abidjan’s waste per year and subsequently uses the waste to produce biogas for electrifying Abidjan and transforms the residual waste into compost. Through this intervention by SITRADE, it can be envisaged that the biogas derived from the waste can provide fuel to produce 25 Gigawatt-hour (GWh) of renewable electricity annually and up to 502,318 tCO2e of avoided greenhouse gas emissions (methane) within seven years [65].

Bioenergy and Carbon-Offsets in MalawiMany countries in Africa spend a significant amount of money importing fossil fuels for the transportation sector and electricity generation. Accordingly, Africa’s heavy reliance on fossil fuels for energy contributes not only to global warming and climate change, but also to astronomical increases and volatility in the prices of energy sources [61]. However, the bioenergy potential of SSA (after accounting for food production and resource constraints) is reported to be the greatest of any of the major world regions [66] hence the development of renewable energy technologies and efficient use of bioenergy could be a viable solution to the many development challenges existing in Africa. In addition to creating opportunities for employment, an enhanced utilisation of bioenergy resources can be beneficial for Africa by enabling increased access to modern energy, reduced carbon emissions, enhanced investment and technology flows, reduced foreign exchange spending (especially for oil-deprived countries), and greater energy self-sufficiency. These opportunities can thereby potentially contribute to poverty indices, food and energy security, and sustainable management and use of natural resources, amongst others [67,68].

Africa has a huge unexploited biomass energy resource with an estimated overall potential that is vastly (531-fold at least) high (even when considering use of only inedible biomass and a combination of abandoned agricultural land, degraded land and other marginal land that does not have competing uses) [66]. In Malawi, Bio Energy Resources Ltd. (BERL) aims to facilitate sustainable development by producing biofuels and biofertiliser. The BERL business model entails the growing of Jatropha Curcas as a boundary crop to ensure that there is no conflict between utilising land for food or fuels. The smallholder farmers that are registered under the project predominantly grow sunflower and/or groundnuts as cash crops for their livelihoods. Since the demand for diesel and paraffin in Malawi is increasing at 6% per annum, BERL produces Jatropha Straight Vegetable Oil (JSVO) for blending with diesel and paraffin in order to reduce the fossil fuel import bill for the country. More importantly, due to the climate change mitigation potential of the project and its contribution towards sustainable land management practices, BERL’s Jatropha Project was registered under the Verified Carbon Standard (VCS) in order to receive carbon credits. In this regard, it is anticipated that the project will generate emission reductions of 7058 tCO2 to 25,878 tCO2 over the 30-year lifetime of the project (2008–2039) [69].

Climate Change Adaptation in MozambiqueSSA is disproportionately vulnerable to climate change due to its greater reliance on agriculture and other climate-sensitive economic sectors for livelihoods, absence of adaptive infrastructure, rapid population growth, and limited economic and institutional capacity to cope with, and adapt to, climate variability and change [70,71]. However, the agriculture sector also presents a sector with the greatest potential to reduce some of Africa’s development challenges. In the first instance, an increase in 1% of agricultural Gross Domestic Product is 3 times more effective in increasing household spending in the poorest households than non-agricultural growth [72]. Secondly, in Africa, 10 million young Africans enter the continent’s workforce annually [73] and more than two thirds of the economically active population in SSA is employed in agriculture, with the proportion for young workers in some cases being even higher [72]. Therefore, despite high rates of migration to urban areas, most SSA youth continue to reside in rural areas and will continue to do so over the coming years; and without sufficient opportunities in manufacturing or services to engage the youth, agriculture will remain a significant sink of labour and source of economic opportunity [74]. However, records indicate that Africa’s total public spending on agriculture as a share of public spending in Africa falls far short of the Comprehensive Africa Agricultural Development Pro¬gramme (CAADP) target of 10% [75], hence even though it is generally acknowledged that climate change adaptation in the agriculture sector is imperative, many countries and governments are plagued by under-investment in the sector.

In response to Africa’s under-investment challenges in the agriculture sector, DanishKnowHow developed the In Grower Programme business model as an agribusiness led strategy to create rural jobs and enhance food security. Through the In Grower Programmes, the under-investment in Africa’s agriculture sector is addressed by creating a system where young entrepreneurs use pooled resources in order to achieve economies of scale for production, market access, financial support and technical support. This is done in synergy with DanishKnowHow using its international networks to provide equity investments, loans and grants to In Grower Programmes in various countries in return for financial profit and social impact. The sustainability of the In Grower Programmes is ensured by stipulating that profit from the production is shared 50/50 between the entrepreneurs and the In Grower Programmes implementers and financiers [76]. Some of the merits of this approach are that In Grower entrepreneurs are provided with training, production facilities, land, irrigation, capital, marketing and business support to reduce most agribusiness risks and climate change vulnerability. This business model therefore shows that corporate actors can have an active part in simultaneously addressing SDG 2 (zero hunger) and SDG 13 implementation through impact investments where public funding is lagging.

Some conventional scholars have argued that the development paradigm is now shifting from “beyond the question of whether growth (still) ‘is good for’ poverty reduction to a question of whether and how the poor can participate in and contribute to growth, and how institutions—formal and informal—can enhance this” [77]. Accordingly, with these considerations in mind and in order to be in-line with the SDGs, corporate sector investments in Global South energy sectors should not only be an issue of utilising various renewable energy technologies to augment climate change mitigation and universal energy access but should also be about using finance models and business models that ensure that aspects of alleviating poverty, reducing gender inequality and reducing climate change vulnerability are considered. With that said, it has been observed that large scale renewable energy projects—which often are grid connected—deliver minimal benefits for sustainable economic development as even if they may bring about an increase in electricity production, this may not translate to an increase in energy access within the country [78]. On the other hand, smaller and dispersed decentralised energy systems have a higher probability of simultaneously addressing the challenge of energy access and contributing to local economic development/inclusion [78]. Moreover, since small scale projects/decentralised energy programmes/mini-grids can provide poor communities with access to energy faster and are often cheaper and quicker to deploy than large centralised infrastructure as they require less investment costs and regulatory approvals [46,47], they can be catalysts for improving the implementation of SDG 10 (reduced inequalities) and SDG 5 (gender equality) in the context of SSA. Unfortunately, it is quite probable that more renewable energy investments will likely still focus on promoting grid connected projects as most private sector financing mechanisms especially through climate finance modalities and traditional financing intermediaries such as MDBs are less able to finance small-scale projects directly, given the higher transaction costs [79]. Additionally, even if there are global increases in private and public funds for climate change mitigation, investors and traditional financing intermediaries are likely to promote the scaling-up and replication of existing renewable energy and climate change mitigation approaches and interventions which have been successful [28]. Arguably, these issues highlight that some strategies that corporate actors can adopt to augment climate resilient inclusive growth would be (i) through the provision of financial and business products and services that can accelerate the deployment of small-scale energy projects/decentralised energy, and (ii) by supporting climate finance intermediaries such as MDBs to prioritise the funding of decentralised energy.

Entrepreneurial activities are a vehicle for economic and societal transformation, hence there is potential for SSA’s entrepreneurs to utilise Impact Investments as instruments for facilitating climate resilient growth. As it stands, approximately US$60 billion worth of assets may be under management in the Impact Investment sector (i.e., Impact Investments are defined as investments that are made to generate a measurable social and environmental impact alongside financial returns) [53], hence SSA entrepreneurs and international corporate actors and investors need to be knowledgeable on the aspects that can enable entrepreneurial activities in SSA to improve the implementation of the SDGs and/or to improve the utilisation of Impact Investments as climate finance instruments. For example, in developed countries, entrepreneurial activities simultaneously enhance economic growth, advance environmental objectives and improve social conditions, whilst in developing countries, entrepreneurship positively contributes to the economic and social dimensions of sustainable development, but its contribution to the environmental dimension is negative [80]. However, it has been suggested that the adverse negative impacts of entrepreneurship on the environment could be reduced by strengthening the innovation capacity of enterprises through more investment in training and education programmes, strengthening cooperation between industries and research centres, and stimulating applied research studies for innovative products and services [80]. Accordingly, since the environmental impacts of entrepreneurial activities in developing and developed countries are different, there is a need for corporate actors in both developed and developing countries to be aware that some entrepreneurial activities can perpetuate adverse environmental impacts so caution has to be taken when advancing entrepreneurship as a strategy to improve the implementation of the SDGs (particularly SDG 7 and SDG 13) and when advocating for entrepreneurs to utilise various climate finance instruments. Similarly, SSA’s entrepreneurship ecosystem is characterised by poor linkages between sustainable social enterprises, entrepreneurs, investors and innovation networks. This therefore means that the majority of Africa’s sustainable social enterprises are not members of professional associations or other formal networks and this adversely affects their impact since this (i) makes finding investible enterprises and entrepreneurs a challenge for investors and (ii) sustainable social enterprises may have limited access to academic and research institutions focusing on research and development (R&D) that can be developed into goods and services for markets [53]. Arguably, in the SSA context efforts to increase the mobilisation of climate finance should be accompanied by complimentary strategies by corporate actors to improve SSA’s ecosystem for social entrepreneurship in order to ensure that the potential of entrepreneurship to advance SDG 7 and SDG 13 implementation can be harnessed.

Climate change/green entrepreneurship is sometimes perceived as a strategy that can facilitate sustainable development in Africa since it enables climate change mitigation and adaptation strategies to bring out economic opportunities. Through climate change entrepreneurship, both formal and informal enterprises in Africa can take active roles in improving waste management, renewable energy deployment, material recycling, information dissemination, etc. [81,82]. Whilst entrepreneurship is often promoted as a means to which corporate actors can take an active role in creating jobs and reducing unemployment, it is also arguable that one of the important aspects of entrepreneurship and climate change/green entrepreneurship is that it can contribute towards domestic resource mobilisation indirectly. This is particularly important as some literature is emphasising that SSA needs to enhance its efforts on domestic resource mobilisation so that local revenues and taxes can complement ODA and international climate finance in financing development programmes [52]. In this case, whilst increasing corporate sector activities and investments through entrepreneurship is desirable, what is even more imperative is identifying and removing the barriers to the development of climate change entrepreneurship since climate change entrepreneurship has the dual goal of improving domestic resource mobilisation and facilitating climate change mitigation and adaptation.

In general terms, a lack of access to finance in Africa is often cited as an aspect that constrains development and the implementation of projects in the region [23,47]. Similarly, the lack of finance does not only constrain business development and entrepreneurship, but it also constrains climate change entrepreneurship, and/or the potential that climate change entrepreneurship could have in the implementation of the SDGs. On the other hand, an unfortunate situation exists where-by, the climate finance policy arena has ignored improving the development of innovative early-stage risk financing modalities. Arguably, since there are large gaps in access to early stage risk financing for project preparation, decentralised energy projects, and new technologies [26], there are also financing gaps for promoting climate change entrepreneurship in SSA. To add to this, unlike other world regions, the financial landscape and climate finance landscape in Africa is devoid of venture capital, and as such without venture capital, highly innovative entrepreneurs—those who would add the most to national development—would be more likely to fail [80]. Arguably, for SSA policies to (i) achieve the deep energy sector transitions towards renewable energy deployment, (ii) enable entrepreneurs to facilitate sustainable development, and (iii) provide the corporate sector (formal and informal businesses) with an enabling environment to scale up financing to a level commensurate with the Paris Agreement’s 2 °C target, corporate sector actors should support policymakers to develop incentives and climate finance instruments that can enable investors and financial institutions to create venture capital funds focusing on facilitating climate change entrepreneurship. A failure to do this may arguably mean that viable climate change enterprises that can provide economic and environmental benefits simultaneously, and augment domestic resource mobilisation through local formal and informal enterprises will not be realised. Since, climate resilient development in any country is only feasible provided that a range of market and policy failures are corrected; and new technologies, business models, and financial innovations are implemented [47], it might be argued that an important step and process that can enable corporate actors to improve the financing and implementation of the SDGs in SSA include raising awareness on how the lack of focus of corporate actors to introduce climate venture capital funds could be a market and policy failure that has constrained the development of green entrepreneurship and development of new enterprises that can develop and utilise new technologies and business models to address climate change in the SSA context.

Countries in the Global South face various challenges in their attempts to achieve the SDGs. For example, despite the implementation of the UNFCCC and implementation of the NDCs framework to improve climate change mitigation and adaptation, global investments in renewable energy are still not yet commensurate with the target to reduce greenhouse gas emissions in-line with the Paris Agreement’s target of keeping global temperature increases below 2 °C. Nonetheless, with greater awareness and greater involvement of corporate actors in the climate finance mobilisation and disbursement domains, there might be a greater probability that the climate finance gaps experienced in the Global South will be significantly reduced. Accordingly, this paper has focused on raising awareness on Global South climate finance perspectives, highlighting the scope to which policy changes can encourage various corporate actors to utilise climate finance and highlighting the scope to which corporate actors can influence the development of new climate finance instruments.

On a positive note, various reports and trends show that the amount of funds through climate finance and various green finance modalities such as green bonds are increasing in value as for example green bond issuance was over US$41 billion in 2015 from US$1billion in 2007. Moreover, even though green bonds only have approximately 1.4% market share in the bond market, in the case of SSA, in relative terms, the rate to which green bonds could be utilised could be higher than for conventional bonds since the green bond market can utilise South-South Climate Cooperation modalities and climate finance modalities to build institutional capacity and reduce the barriers that impede the issuance of green bonds in SSA countries. Added to this, innovations and modifications have been undertaken in SSA’s financial sector hence financing modalities such as microfinance, energy crowdfunding platforms, financial intermediation and MSMEs Green Funding are gaining ground, and their impact can be magnified if the actors in these sectors are given support to enable them to unleash their potential to further develop new models of green finance projects, products and services. On another note, climate change entrepreneurship can create jobs, improve NDC implementation and contribute towards national efforts to increase domestic resource mobilisation. However, there is a lack of corporate investments in the climate change venture capital fund sector in SSA. This arguably means that another starting point to reduce climate finance gaps in the SSA contexts could be through enacting policies that (i) incentivise corporate actors to develop and implement climate change venture capital funds and (ii) support corporate actors to create climate change entrepreneurship ecosystems that can accelerate the mobilisation of funds for SDG 7 and SDG 13 implementation.

Universal energy access (SDG 7) and reducing climate change vulnerability (SDG 13) will arguably be the hardest to achieve in SSA. This paper has therefore focused on providing some emerging themes on the corporate sector activities that can enhance the mobilisation of climate funds and accelerate SDG 7 and SDG 13 implementation in SSA. From the analyses provided, it has been suggested that promoting climate change entrepreneurship and improving access to early-stage risk financing modalities such as venture capital need to be prioritised in order to improve the implementation of SDG 7 and SDG 13. From an industry or practical point of view, this highlights an emerging need for private sector organisations to prioritise the mobilisation of human capital and other resources to facilitate training and human capacity building in climate change entrepreneurship and venture capital funding modalities from SSA perspectives. As it stands, the replication of Global North environmental strategies in SSA has not always been effective due to differences in perspectives between Global South and Global North actors [83,84], hence similarly the failure to initiate training and human capacity building with a SSA context could diminish the potential to which climate change entrepreneurship and venture capital could have on enhancing the private sector’s contributions to SDG 7 and SDG 13 outcomes.

The analyses provided in this paper also highlight the need for various SSA countries to enact various policies to enhance the contributions of the private sector in facilitating sustainable development outcomes in the Global South. The policy aspects for consideration include:

•

•

•

The findings of this paper are similar to the findings of UNDP [53] and Nakhooda and Norman [9]. In this case, UNDP [53] suggested that the approaches and strategies employed by development and traditional financial sectors to facilitate SDGs implementation are inadequate to support sustainable and resilient development, and Nakhooda and Norman [9] indicated that it was unlikely that the approaches taken in most climate finance modalities would be sufficient to enable SSA corporate actors to support the shift to low carbon and climate resilient development trajectories at the scale and pace that is necessary. An important contribution of this study to the existing body of sustainability literature is therefore that the study demonstrates that even though climate finance has the potential to engage and incentivise more corporate actors in the implementation of the SDGs, particularly SDG 7 and SDG 13, most climate change financing modalities are not yet capable of supporting start-up entrepreneurial activities and climate change entrepreneurship. In the light of all these considerations, this paper may also be used in the sustainability literature to highlight why in the context of SSA, policies aiming to significantly increase the mobilisation of climate funds for NDCs implementation through the corporate sector should not only focus on creating regulatory environments for addressing market failures to decrease business risks but should equally focus on creating an enabling environment for social enterprises and entrepreneurship clusters to thrive. Through this approach, it will then be permissible for corporate actors to be in the forefront- ahead of governments- in forging new paths and strategies to address global development challenges.

An area for further investigation could be to determine how Africa’s corporate sector can be incentivised to support research and development in SSA’s climate change sector. This follows that for SSA to increase its climate change mitigation ambitions, there will be a need for technological and institutional innovation but yet finance allocated for research and development has been declining globally [9]. Consequently, there is a lack of knowledge on innovative approaches that various corporate entities can utilise to finance various climate change programmes. New research and development corporate funds can therefore play an important part in providing additional funds to be used in facilitating climate change research and development.

The author declares no conflict of interest.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

62.

63.

64.

65.

66.

67.

68.

69.

70.

71.

72.

73.

74.

75.

76.

77.

78.

79.

80.

81.

82.

83.

84.

Chirambo D. Corporate Sector Policy Innovations for Sustainable Development Goals (SDGs) Implementation in the Global South: The Case of sub-Saharan Africa. J Sustain Res. 2021;3(2):e210011. https://doi.org/10.20900/jsr20210011

Copyright © 2021 Hapres Co., Ltd. Privacy Policy | Terms and Conditions