Location: Home >> Detail

J Sustain Res. 2023;5(1):e230004. https://doi.org/10.20900/jsr20230004

,

Pierre Failler 1,2,

Michael Bennett 1

,

Pierre Failler 1,2,

Michael Bennett 1

1 Centre for Blue Governance, University of Portsmouth, Portsmouth, PO1 3DE, UK

2 UNESCO Chair in Ocean Governance, Portsmouth, PO1 3DE, UK

* Correspondence: Antaya March.

This article belongs to the Virtual Special Issue "Oceans and the Blue Economy"

The aim of this study is to identify the key policy, regulatory, economic, and capacity constraints, as well as opportunities for the financing needs of Blue Economy (BE) projects focused on fishery and aquaculture in Barbados, Grenada, and St. Vincent and the Grenadines. Coastal and marine environments provide multiple important contributions to the Blue Economy in Barbados, Grenada and St. Vincent and the Grenadines. The total contribution of the ecosystem services provided by mangroves, coral reefs and seagrass beds is estimated at around US$800 million annually for all three countries. The health of these important provisioning ecosystems is under threat. The natural capital in Grenada, Barbados, and St. Vincent and the Grenadines is being depleted, largely due to the anthropogenic drivers of overfishing, coastal development, pollution, introduction of invasive species, and the impacts of climate change. Despite these threats, at present the policies and agreements in place (at the national, regional and international level) operate in fragmented manners with insufficient overarching frameworks to involve financial support or investment to mitigate these threats. In this way, the full potential of the fisheries and their ability to contribute to the wider Blue Economy is not being realised in the target countries. To valorise the fishery sector and generate long-term sustainable financing options, prioritising the domestic market and intra-regional trade, and increasing the value addition of fish products to increase profitability is recommended. Further to this, by improving the condition of the ecosystems on which fisheries depend through sustainable financing strategies such as blue bonds or payments for ecosystem services, the capacity of fisheries can be increased by up to 60%. In this regard, better valuing of the ecosystems for their economic role to each nation should be a key focus of national priorities and investment. Lastly, the improved management of current marine protected areas (MPAs) and the networking of MPAs should be a more refined focus for fisheries management, rather than using MPAs solely for conservation purposes. In terms of investing into the expansion of the aquaculture and mariculture sectors, three focus areas are discussed. The first area is the scaling up of aquaculture and mariculture which offers the potential to optimise the benefits received from the development of the marine environment, create sustainable quality employment, and offer high-value commodities for export and the domestic market. Dedicated blue financing funds are needed to drive technological advancements to facilitate development and exploitation of the currently immature aquaculture sector. The second focus is integrating aquaponics into Blue Economy development strategies alongside fisheries and aquaculture to provide a pathway to realise the sustainable intensification of fisheries, aquaculture, food and agriculture. Lastly, to achieve scalable growth of aquaculture, investing in avenues that enhance existing relationships with other sectors, as well as encouraging new ones, should be explored. In this way, alternative and emerging industries related to aquaculture provide a wealth of opportunities. An essential factor in the development of these industries is to effectively integrate them amidst the Blue Economy, and having a well established understanding of how to implement it.

The COVID-19 pandemic exposed the structural economic vulnerabilities that developing countries in general—and small island developing states (SIDS) in particular—are facing. This was not least due to the developing countries’ position in the world economy and due to the vulnerabilities of their often resource-based economies. Many countries that had liberalised capital movement in preceding decades saw rapid capital flight; economies focused on tourism saw declines in growth, employment and tax revenues; and the seafood industry in particular was also impacted as lockdowns and restrictions disrupted global supply chains and shifted demand patterns. The pandemic has created lasting impacts that have been felt hard, particularly by developing countries. There is therefore a need to strengthen existing industries and develop new industries, in an effort to recover from the pandemic.

The aim of this study is to identify the key policy, regulatory, economic, and capacity constraints, as well as opportunities for the financing of Blue Economy projects focused on fishery and aquaculture in Barbados, Grenada, and St. Vincent and the Grenadines. A well-managed seafood sector can be an important source of revenue; however, public and private resources are required in order to invest in a well-managed and productive seafood sector. In order to explore potential investable revenues for and from a diverse seafood sector (including actors from commercial industry to small-scale fishers) with varying degrees of capacity and financing needs, we need to review the role of existing policies and regulations and the opportunities that exist for the valorisation of fisheries and expansion of aquaculture in the context of wider Blue Economy development at the various resolution levels within the sector. While the study focuses on these three countries, its review of policy and regulatory structures, as well as capacity and economic constraints, and the analysis of financing opportunities, are not limited to these three case study countries. This evaluation will allow for the identification and development of options to address the financing constraints that project developers face in the fisheries and aquaculture sectors. As such, this has the potential to contribute to program developments to reduce poverty and inequality, and enhance prosperity and resilience, by strenthening biodiversity and the health of the blue ecosystem in the region. By proxy, this will support the achievement of the Sustainable Development Goal (SDG 14) (life below water) and contribute to SDG 8 (Decent Work and Economic Growth) and SDG 17 (Partnerships for the Goals).

The findings of this study are based on a literature review of relevant documents relating to fisheries and aquaculture financing, and engaging with relevant stakeholders during workshops. Under the ʿSDG Joint Fund Programme: Harnessing Blue Economy Finance for SIDS Recovery and Sustainable Development’, the consultation process involved meetings with stakeholders at a national level, with state and various sector representatives at the industrial, semi-industrial, and small-scale levels, who are able to implement blue financing strategy and identify gaps and needs in the current system. The consultation was done to identify projects suitable for blue financing solutions and was conducted between October and December 2022. A series of regional workshops were hosted over this period and included the three countries of Barbados, St. Vincent and the Grenadines, and Grenada, as well as the Fisheries and Aquaculture Organisation (FAO), the United Nations Environment Programme (UNEP), and the United Nations Development Program (UNDP).

Firstly, we provide an overview of the fishery and aquaculture sectors in the three countries, including key figures around production, consumption and future trends, key economic and social figures, as well as environmental and climate change associated figures and trends. This section builds on findings from the CFRM 2020 Statistics and Information Report, the UNEP Final Report on Barbados, Grenada, and St. Vincent and the Grenadines, the UNDP Review of National Blue Economy Frameworks for Barbados, Grenada, and St. Vincent and the Grenadines, and the FAO 2021 ‘Rapid Assessment of the Regulatory and Policy Environment for Blue Economy Financing in Barbados, Grenada, and St. Vincent and the Grenadines’, which identify key policy, regulatory, economic and capacity constraints and opportunities for financing fisheries and aquaculture. We then analyse the key policies and regulatory frameworks in place relating to the fishery and aquaculture sector, with a specific focus on their effectiveness and achievements. This includes international, regional and national policies and frameworks, as well as related policies associated with tourism, climate change, and biodiversity targets. The third section reviews capacity constraints, including structural constraints and institutional coordination issues, as well as examining the opportunities for the financing of Blue Economy projects.

Annual fish catches for the three countries have been stable over the last decade at around 5000 tonnes (see Figure 1 below). Aquaculture is still in the early stages of development with almost no production, except that of Eucheuma algae for about 50 tonnes per year in Grenada and St. Vincent and the Grenadines, and about 25 tonnes of freshwater tilapia in Barbados. Imports tended to increase slightly in recent years to reach a plateau of 15,500 tonnes, driven mainly by the increase of Barbados imports of tuna and canned sardinella. Exports are below 2000 tonnes over the decade. For Barbados and Grenada, this is composed mainly of tuna, and for St. Vincent and the Grenadines, of various crustaceans [1].

Figure 1. Production, Import and Export of fish of the 3 countries [1].

Figure 1. Production, Import and Export of fish of the 3 countries [1].

As most of the resources on the insular shelf of these countries are already fully exploited or even overexploited for the crustaceans and reef fish [2], the catches will remain at the 2010–2019 level for the coming years. The restoration of degraded habitats such as mangroves and seagrass meadows as well as the reduction of the land-sea pollution may help to increase the catches in a mid-term perspective. For Africa, it is estimated that coastal habitat restoration should provide an additional 8 to 10 million tonnes of fish biomass for current catches estimated at 7.5 million tonnes [3]. Protected habitats such as marine reserves in Florida (USA) and St. Lucia have increased the fish catches of artisanal fishers between 46%–90%, over five years of habitat protection and restoration [4].

The net supply remains stable for the 3 countries over the period; on average 40 kg/capita/year for Barbados, 27 for Grenada and 20 for St. Vincent and the Grenadines (see Figure 2 below). Fish continue to be a key element of the population’s diet of Barbados providing about 50% of the animal proteins.

Figure 2. Net fish supply for each country [1].

Figure 2. Net fish supply for each country [1].

As the population will stay at the 2020 level until 2030 for the three countries, fish supply is not likely to be an issue. Furthermore, as the population is expected to decrease in Barbados between 2030 to 2050 (from 290,000 to 277,000) and to a lesser extent in St. Vincent and the Grenadines (from 113,000 to 109,000), while that of Grenada should stay the same (116,000, UN Population Prospects 2022), the pressure on marine resources should not be exacerbated as is currently the case where populations are growing significantly. However, the tourism population, in the case of drastic augmentation in the coming years, will continue to maintain pressure on inshore and nearshore fisheries, due to the increased consumption of fish products by tourists.

Key Economic and Social FiguresThe importance of fisheries for coastal communities and livelihoods in the focus countries is high. According to FAO, this is particularly the case for ‟coastal fisheries”, including subsistence, artisanal and/or semi-industrial varieties. Although the Caribbean has limited resources in terms of developing a large-scale fishing industry, the value of fish and sea products as a source of food has long been recognised. More than three billion people rely on fish products as an important source of animal protein [2].

In St. Vincent and the Grenadines, sea moss (Eucheuma spp., Gracilaria spp., and Kappyaphycus alvrezii) aquaculture is in place, with exports begining in 2019. St. Vincent and the Grenadines was able to fill the gap on the market associated with border closures of traditional exporters of sea moss (St. Lucia and Jamaica). In Grenada, sea moss (Eucheuma spp. and Gracilaria spp.) occurs in very small quantities for aquaculture. Experiments with aquaponics were previously initiated but to date have not been successful. Barbados is exploring the possibility and potential of aquaponics with a demonstration farm under development.

In Barbados, the inland fisheries are not of economic importance, and the permanent and temporary freshwater catchments of Barbados serve as habitats for species of freshwater shrimps [2], however, no known commercial fishing activities occur in these fresh water catchment areas. The same is true for Grenada, where it was noted [5] that inland fishery is restricted to harvesting of fresh water crawfish and a half dozen species of finfish within small streams, carried out solely on a subsistence basis [5]. The crawfish population in Grenada has been depleted to such an extent that Grenada has imposed a closed season for this species from 1 May to 31 August annually [6]. As a result there is no visible or direct harvesting of this freshwater shellfish throughout much of the year. As it relates to other freshwater fish in the river (wild), over 90% of these species are no longer frequently seen and currently there is limited fishing for these species because they are no longer targeted as trading commodities (on the produce market). In St. Vincent and the Grenadines, there is some economic importance of the freshwater fisheries where the traditional catching of Goby fry (locally called Tri-tri) caught at river mouths and estuaries, is of economic importance. While not econommically important in all cases, inland waters/freshwater systems are of cultural importance to Grenada and St. Vincent and the Grenadines, despite Grenada having no economic importance in this regard. There is currently no information available on the number of persons employed in direct production from the inland or fresh water systems.

The fisheries sector also provides employment for many persons who supply services and goods to the primary producers. This includes persons engaged in processing, preserving, storing, transporting, marketing, and distribution, or selling fish or fish products, as well as other ancillary activities, such as net and gear making, ice production and supply, vessel construction and maintenance, as well as persons involved in research, development and administration linked with the fisheries sector. The number of persons employed in direct production in the commercial marine capture fisheries and aquaculture sub-sectors (including full-time and part-time fishers, harvesters, and farmers engaged in artisanal/subsistence and commercial activities), in the three countries together for 2019, was approximately 23,500 persons (roughly 6000 persons employed in direct production in the marine capture fisheries and 17,600 persons employed indirectly from fishery related activities). In Grenada, 85% of all fishers possess a minimum elementary education (i.e., pre-secondary). Studies regarding the value of Barbados’ fisheries [7], showed that as the fish moved through the various market pathways to the consumer it increased in value and contributed to livelihood, and that the overall additional value was 2.6 times the landed value of the fishery.

The fisheries are exploited by various sectors of the society, including: citizens or authorised persons who exploit the fisheries as their primary source of income—commercial exploitation or commercial capture fisheries; citizens or authorised persons who exploit the fisheries as a recreational activity—recreational exploitation or recreational fisheries; citizens or authorised persons who exploit the fisheries under sporting activities—sports fisheries; and citizens or authorised persons who exploit the fisheries as a primary source of protein for dependents—subsistence fisheries. The key socio-economic figures associated with fisheries and aquaculture for the three countries, including employment, contribution to GDP, and the value of production, are presented in Table 1 below.

Table 1. National socio-economic values for the focus countries.

Table 1. National socio-economic values for the focus countries.

In all three countries there is a lack of integration of fishery data into economic value (particularly the data from artisanal, subsistence, and small boat fishing). Economic data on fisheries is generally lumped together with agriculture and forestry since they often fall under the same ministry. Even when disaggregated, fisheries data does not reflect the real contribution of the fisheries sector to the socio-economic welfare of the country. The national socio-economic perspective does not take into account the subsistence fisheries as no data has as yet been captured in this regard, and this includes line fishing from rocks, small boat fishing, the use of fishing traps and spear fishing. As such, the contribution of the fisheries sector to the GDP and other economic indicators is therefore underestimated. For example, in St. Vincent and the Grenadines, disaggregated data from the Government Statistical Department shows fisheries contributing 0.04% of the national GDP. In this regard, improved integration of fishery data pertaining to artisanal, subsistence and recreational fisheries into national statistics and economic valuations should be a notable priority.

Key Environmental and Climate Change Figures and TrendsCoastal and marine environments provide multiple important contributions to the Blue Economy [8]. In almost all cases, a healthy environment underpins economic activities. Vital ecosystem services for the continued functioning of society include carbon sequestration, coastal protection, and waste disposal for land-based industries. Direct uses of the marine and coastal environments include extraction of natural resources like (capture and recreational) fisheries, wood, and tourism associated with coral reefs. These ecosystems also provide ecosystem services associated with carbon sequestration, biodiversity and wastewater mitigation. Particular to the fisheries and aquaculture in the region under study, coastal ecosystems (specifically mangroves, seagrass beds, and coral reefs) provide notable functions to capture fish, acting as breeding grounds, nurseries, and feeding grounds that contribute to productivity. The removal and/or degradation of these environments, either in area or health, will likely undermine the provision of these services. For example, mangrove afforestation provides increased blue carbon benefits (carbon storage and sequestration) compared to mangrove deforestation, in terms of mitigating climate change effects [9]. The economic cost of replacing these functions and services once lost will be extremely high. Moreover, a single habitat type will concurrently contribute multiple services, underscoring the value of these systems to the country’s well-being. Among the seven focus countries, St. Vincent and the Grenadines has the largest area of coral reefs, more than double that of Grenada (Table 2). Seagrass meadows are virtually non-existent in Barbados [10]. In the other two counties, seagrasses have limited coverage and are on the decline. In all three countries, mangroves have reached a critically low extent and are close to local extinction [11]. A rough estimate [12] of the total contribution of these environments is around US$800 million annually for all three countries, where the ecosystem services from ecosystems in Martinique (per equivalent area) were valued at €250 million per year, each.

Table 2. The extent of key coastal and marine environments and their estimate values.

Table 2. The extent of key coastal and marine environments and their estimate values.

Pollution, destruction, and climate change, threaten the ability of these ecosystems to provide their essential functions to fisheries in terms of productivity, and to fishing communities in the form of coastal resilience, against the effects of climate change. Where coral reefs have the highest coverage in the three countries, they act as the key ecosystems to provide services to the fishery and aquaculture sectors, as well as acting as the only major coastal defence against the effects of a changing climate. Coral reefs support a multitude of fish species and produce significant amounts of fish for various fishery sectors [16]. Coral reefs can also serve as important biodiversity and genetic reservoirs which have potential in aquaculture.

In this regard, it is necessary to understand the condition of coral in these islands. Mean live coral cover has declined precipitously in many shallow reefs across the Caribbean over the last few decades [17]. Grenada’s coral condition is considered critical in many places, and poor to fair in others. Barbados reef condition overall is considered as fair to poor. St. Vincent and the Grenadines national coral condition is considered fair, and given the large coverage, suggests the reefs support larger fish populations [15]. The notion that very few coral reef systems in the identified countries are considered to be in good condition is a worrisome prospect for the delivery of fishery services. However, coral in poor condition can recover if human impacts are reduced, and marine managed areas are prioritised to help fish to recover [15]. Currently the poor data on fish stocks makes it difficult to determine their state, but there is scope to increase data collection for evidence-based management.

Caribbean island states share similar environmental challenges with related characteristics such as small size, susceptibility to natural disasters and climate change, vulnerability to external shocks, concentration of population and infrastructure in the coastal zone, high dependence on limited resources including marine resources, fragile environments, and excessive dependence on international trade [18,19]. Throughout the literature there is strong evidence that the natural capital in Grenada, Barbados, and St. Vincent and the Grenadines is being depleted, largely due to the anthropogenic drivers of overfishing, coastal development, pollution, introduction of invasive species, and the impacts of climate change [5,11,17,20]. Such depletion represents a significant risk to the economic benefits generated by the ocean economy of these nations, and likely to future growth prospects. Notably, the fisheries sector is more vulnerable to climate change than in other regions.

Negative impacts from climate change that are already obvious in this region include coral bleaching [19,21], associated ocean acidification [22,23], increasing frequency of high intensity storms and hurricanes, increased sea level, and Sargassum influxes that are disrupting fishing operations, fish landings, and fisher livelihoods [1]. Sea level rise in the region has already impacted the fisheries sector (in particular in combination with damages caused by storms and hurricanes) by means of beach erosion and the impacts thereof on housing and fisheries landing sites. In Barbados, for example, fishers have had to relocate in the Six Men’s Bay fishing community partly as a result of the increasing level of beach erosion [18]. Such stresses on coastal and marine ecosystems will ultimately affect the harvest and post-harvest sectors, as well as the national economy.

Tropical storms and other major weather events, which are intensifying due to climate change, hit the island’s fishery communities disproportionately hard by preventing fishing before, during, and after the events. During the event itself, vessels and fishing gear may be destroyed or damaged. Afterward, the harm is compounded by loss of public services such as electricity, fueling stations, piers, and roads. Fishery products stop flowing to market, causing special hardships in poor communities. Yet at the same time, fisheries can play an important role in disaster recovery. While the sector is highly vulnerable to climate hazards, its people can get back out on the water as soon as they have good weather—and functioning boats and equipment. They can bring back fish to communities that would otherwise go hungry after a disaster. For this reason, a rapid bounce-back of the fishing industry after weather events can be critical for overall recovery and food security in the three countries [18].

In terms of pollution, all three countries are threatened by growing levels of mismanaged waste disposal (including from land and ship-based sources), untreated sewage, soil erosion, and agricultural runoff. In particular, increasing volumes of untreated sewage generated by growth in coastal development has impacted water quality and public health, as an estimated 85% of wastewater entering the Caribbean Sea is untreated, with a higher percentage in many urban areas [24]. This can constitute a significant risk to the fisheries sector. With regard to marine debris, the Caribbean Sea is estimated to have relatively high levels of plastic concentrations compared with many other large marine ecosystems [25].

The Caribbean region has seen a significant influx in the seaweed Sargassum during the past decade [26,27], where mass strandings on coastlines have significant socio-economic impacts on fisheries (and other sectors such as tourism). This results in reduced access to fishing grounds and disrupted fishing operations when fisheries cannot take their boats to sea [28]. Furthermore, Sargassum can clog engines and gear, and affect water quality. Fisheries and aquaculture may also be severely impacted by the mortality of fish and other marine life, resulting in reduced and/or altered fish catches. Coastal systems like seagrass beds are also at risk of mortality due to Sargassum blooms [29]. As an example, in Barbados, the arrival of massive amounts of Sargassum have coincided with a dramatic decrease in flying fish landings from 981 tonnes in 2014, to 278 tonnes in 2015. This represented a 72 percent decline in one of the island’s most important fisheries [30].

Despite the threats of climate change and environmental degradation to fisheries, at present the policies in place operate in fragmented manners with insufficient overarching frameworks to involve financial support or investment to mitigate these threats. In this way, the full potential of the fisheries and their ability to contribute to the wider Blue Economy is not being realised in the target countries. Existing frameworks are not cohesive and are characterised by a collection of multilateral fisheries agreements, programmes, projects, and dated national laws at various levels. As such, coastal and marine resource management, environmental agendas, and tourism management, remain separate from fisheries management. Furthermore, there is a significant lack of consideration of the potential of natural environments to continue to provide ecosystem services essential to the fisheries. The lack of integration has resulted in gaps in implementation and duplication of efforts across agencies at the national and regional level. There are a range of barriers and gaps in enabling conditions that implicate the fisheries and aquaculture sectors both at the sector and wider Blue Economy level. Specifically, efforts to fully accelerate the socio-economic potential of fisheries and aquaculture are hindered by a lack of sustainable blue financing, and an overarching integrated governance framework to coordinate various pressures on coastal and marine resources.

There are a number of existing policy structures in place in Barbados, Grenada, and St. Vincent and the Grenadines, where the countries have signed onto many international fisheries agreements with the anticipation of fruitful and mutual beneficial progress and prosperity within the fisheries industry (see Table 3). Although these international agreements and policies have been ratified, there are still several loopholes which need addressing as relates to the impacts on the local fisheries sector. For instance, the Government of Barbados is currently a member of ICCAT but lacks active participation which has resulted in stunted growth within Barbados’ fishery development. Grenada has not signed onto many international agreements, and in particular has not ratified the 1993 FAO Compliance Agreement which leaves room for the reflagging of fishing vessels and discrepancies in fisheries conservation and management measures. Similarly, Grenada has not ratified the FAO Agreement on Port State Measures, indicating significant lack in progress towards combating IUU fishing as identified as a target of SDG 14.6.

Table 3. International and regional mechanisms related to fisheries.

Table 3. International and regional mechanisms related to fisheries.

From a regional perspective, all three countries are members of the Caribbean Regional Fisheries Mechanism (CRFM), which is a specialised CARICOM Institution established in 2002 by CARICOM Heads of States, to promote sustainable use of the living marine and other aquatic resources by the development, efficient management, and conservation of such resources. As such, Barbados, Grenada, and St. Vincent and the Grenadines are all party to the Caribbean Community Common Fisheries Policy (CCCFP), a binding treaty focusing on cooperation and collaboration of Caribbean people, fishermen and their governments in conserving, managing and sustainably utilising fisheries and related ecosystems. Grenada and St. Vincent and the Grenadines are both members of the Organisation of East Caribbean States (OECS) and thus party to the Fisheries Management and Development Strategy and Implementation Plan. While Barbados geographically forms part of the eastern Caribbean, it is not, however, a member of the OECS. All three countries are members of the Caribbean Network of Fisherfolk Organisations (CNFO) which endeavours to contribute to participatory fisheries governance and sustainable fisheries development.

At the national level, the three countries have separately developed national plans and policies for managing fishery resources (Table 4). There is a significant lack of policies governing aquaculture, given that aquaculture is underdeveloped, and there are no national institutions engaged in basic research for sustainability in the aquaculture industry. The national policies outlined below fail to address issues such as conflicting use of resources between tourism, environmental service, and cruise ships.

Table 4. National fishery and aquaculture related policies.

Table 4. National fishery and aquaculture related policies.

In Barbados, within the Fisheries Act [31], there lies issues with the technicality of implementing closed seasons for sea urchins and the control and surveillance of fishing within the boundaries of marine reserves. The lack of data and unknown status of stocks of many marine fishery resources, suspected overfishing and overexploitation of resources, poses significant challenges to national policy implementation. All fish exports are currently directed to a single importer, which can increase market risk, limit price discovery, and exacerbate a lack of pricing transparency. Due to the lack of transparency, fishers face a significant grading risk because this is a consignment fishery and the fish are not officially graded until they reach Miami.

In St. Vincent and the Grenadines, the Fisheries Act (1986) [36] and Regulation (1987) [37] requires revisiting as there are loopholes such as the lack of legal management structure within the ten conservation areas in the territorial waters, and a disregard of catch limit for any of the fisheries. This has resulted in pressure on the inshore fisheries, stakeholder’s conflict and overuse, and unsustainable methods of harvesting. Governmental and private funding in fisheries ventures are notably inadequate, although some technical support is given by the National Fisher Folk Co-operative. The national policies of St. Vincent and the Grenadines also do not adequately address the safety and quality assurance for export markets, contributing to a significant trade deficit where import exceeds export by a ratio of 3:1.

In Grenada, there are significant financial and human resource constraints in fisheries and a lack of a cohesive management structure for resources, due to the multiple departments and agencies with jurisdiction over aspects of implementation and monitoring, together with the recent induction of fish aggregating devices (FADs). Although the introduction of FADs has led to a significant increase in the catching of yellowfin tuna and has created new opportunities, there have also been concerns about the viability of the country’s yellowfin tuna fisheries given the increased pressure and open access nature of this fishery. Only Grenadian registered vessels are allowed to fish in Grenada’s waters.

Naturally, all national policies have priorities for feeding the nation and ensuring food and nutrition security as well as creating jobs, generating value addition, and ensuring sustainability. Unfortunately, in the three countries, the fisheries policies as stand-alone policies often do not cover environmental and social issues such as labour, resource efficiency, community-related issues, ecosystem restoration, indigenous people, and cultural heritage.

Regulatory Frameworks and Their EffectivenessAt the regional level, there are a number of management plans or frameworks in place for the fisheries, particularly under the CRFM, for which there are five, such as for the management of Queen Conch, for example [52]. Each of the three focus countries has a regulatory framework for fishery activities on varying scales.

Barbados’ Fisheries (Management) Regulations (1998) includes: mesh size restrictions for seine nets (3.81 cm, stretched mesh, minimum size) and fish traps (3.18 cm at narrowest point); the mandatory installation of escape panels and identification marks on fish traps; prohibits the use of trammel nets and other entangling nets; prohibits the capture of lobsters carrying eggs or removing the eggs from lobsters (scrubbing); prohibits the capture, possession or sale of marine turtles, turtle eggs and turtle parts; bans the use of SCUBA for harvesting sea eggs; regulates the sea egg fishery through the designation of closed seasons and closed areas by the minister responsible for fisheries; prohibits landing tunas of less than 3.2 kg live weight; stipulates that aquatic flora or fish to be used for ornamental purposes may only be fished with the written permission of the Chief Fisheries Officer; stipulates that corals may not be damaged, destroyed or fished without the written permission of the Chief Fisheries Officer. The maximum penalty for breaking any of these regulations is a fine of US$50,000 and/or two years’ imprisonment.

In St. Vincent and the Grenadines, The Fisheries Act (1986) [36] and Regulation (1987) [37] gives the Fisheries Unit the legal authority to issue fishing licenses to local and foreign fishers and to enforce the terms of these agreements. The Fisheries Regulations also outline conservation measures including the size of lobsters, the times of the year they may legally be caught, and the mesh size (one inch) that may be used in fish posts. The closed season for lobsters is 1 May to 31 August while the closed season for turtles is 1 March to 31 July. Other conservation measures implemented in St. Vincent and the Grenadines include the designation of marine parks and marine conservation areas. There is no catch limit for any of the fisheries in St. Vincent and the Grenadines, but boat size is a limiting factor to the quantity of fish a fisher can take at any one time and how far into the territorial waters he can go. The Fisheries Division, which is under the direction of the Chief Fisheries Officer who reports to the Permanent Secretary, the Ministery’s administrative chief, is in charge of managing and overseeing the fisheries. It is the duty of The Permanent Secretary to report to the Minister, who in turn reports to the Cabinet. The Fisheries Division staff consists of technical officers, data collectors and managers, and research and clerical officers.

The Grenada Fisheries Act (1986) [32], declares that Grenada has no catch limits or stock assessments in place. Grenada has size limits for lobsters, turtle, and conch, but none for finfish. The Fisheries Division is working closely with the International Commission for the Conservation of Atlantic Tunas (ICCAT) to manage tuna effectively. This work focuses on data improvement and regulation compliance. Grenada’s fisheries data are usually passed onto CRFM upon request, but are not deposited there. Fisheries data collectors record the weight and value of landings daily at Grenada fish markets. Landings data are collected based on boat name, species, effort, crew size, area fished, and type and quantity of gear used. Usually, a data collector approaches each vessel that lands to take the landing details. To capture the weight and price, the fish are separated by species. Fishers receive concessions (i.e., duty and tax) and other incentives for complying with the data collection process. The fisher and gear registers are not updated regularly due to capacity problems, so it is difficult to know what quantity of gear is used and how many fishers are out at sea at any given time. The Fisheries Division has only four technical officers, a number insufficient for the job.

Although these regulations are in place, all three countries face similar issues associated with fisheries management. Despite the purpose of being party to the CRFM and the requirement of member states to “collect, manage and appropriately use scientific data and information to inform the fisheries management planning and decision-making process, and fulfil international reporting requirements” [52], there is an overwhelming lack of consistent data collection concerning the fisheries of Barbados, Grenada, and St. Vincent and the Grenadines. Furthermore, uncertainty about the biological status of many of the regions’ fish stock has remained high, but available data reported [2] suggests that nearly 60 percent of commercially exploited fish stocks are either overexploited or have collapsed [2,53]. As such, with fish stocks under such a state of overexploitation, this suggests that existing structures for regulating the activities of fisheries are not functioning as intended.

Many attempts have been made in recent decades to incorporate co-management as part of fishery management strategies [54–56], with significant prospects for improved management. However, twenty years later, efforts in this regard seem to have diminished. Given the success of co-management in various other SIDs and developing state contexts [57,58], there is a precedence for further effforts in this regard to improve the existing regulatory structures in place to manage the fishery resources.

Given the nascent stages of aquaculture in Barbados, Grenada, and St. Vincent and the Grenadines, regulatory frameworks for aquaculture development are yet to be developed. However, some indications for regulation can be drawn from coastal tourism regulations, given the occupation of the coastal area, which would need to be shared with any aquaculture sites. Furthermore, some incentive mechanisms could be developed at the national level for the development of aquaculture.

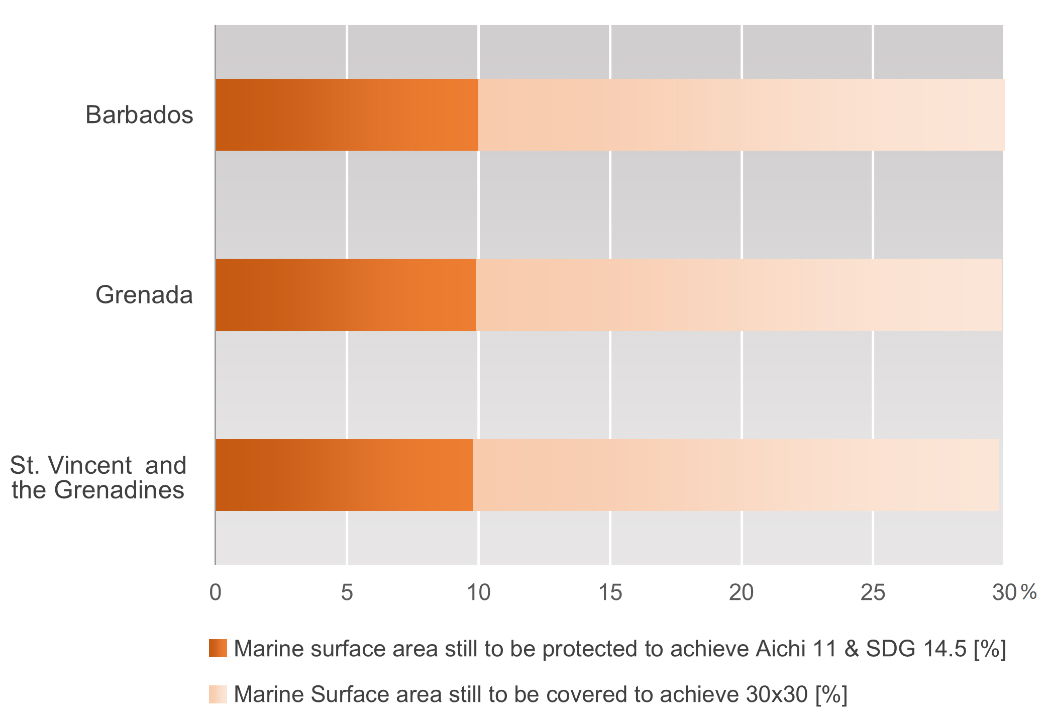

Current Policies and Frameworks in Relation to Fisheries: Biodiversity Targets and Climate ChangeIn terms of reporting on their National Biodiversity Strategy and Action Plan pursuant to their obligations under the Convention on Biological diversity and the Aichi Targets, Barbados and St. Vincent and the Grenadines have submitted their 6th National Reports in 2019. Grenada is yet to do so, having submitted their 5th National report in 2014. Aichi Target 11, defined at the sixth meeting of the Conference of the Parties (COP) signatories of the Convention on Biological Diversity, states that by 2020, 10% of the coastal and marine areas of the signatory countries should officially be protected. The same is so for the delivery of SDG target 14.5. Progress towards Aichi Target 11, is very far from achievement in all three countries (Figures 3 and 4). These targets, updated to achieving 30% protected area coverage of signatories’ exclusive economic zones (EEZs) by 2030, though COP15 has been hailed to go a long way towards averting the biodiversity crisis while also helping to address climate change. However, this is not without its criticisms, and remains controversial because of the chequered history of poorly designated and managed protected areas. While some have saved species from extinction and allowed for significant recovery of fisheries related resources, others—so-called ‘paper parks’—through ineffective management have caused severe impacts to fishing communities through forced displacement. In response to the 30 × 30 targets, the three focus countries have thus achieved very little given their marginal contributions to attaining the original 10% (Figures 3 and 4).

Figure 3. Percentage (%) of marine surface area of national EEZ to be protected to achieve Aichi target 11 and SDG 14.5 for Barbados, Grenada, and St. Vincent and the Grenadines.

Figure 3. Percentage (%) of marine surface area of national EEZ to be protected to achieve Aichi target 11 and SDG 14.5 for Barbados, Grenada, and St. Vincent and the Grenadines.

Figure 4. Marine surface area (sq.km) of national EEZ to be protected to achieve Aichi target 11 and SDG 14.5 for Barbados, Grenada, and St. Vincent and the Grenadines.

Figure 4. Marine surface area (sq.km) of national EEZ to be protected to achieve Aichi target 11 and SDG 14.5 for Barbados, Grenada, and St. Vincent and the Grenadines.

From a wider environmental and climate change perspective, Barbados’ Second National Communication (2018) indicates climate change as a major challenge that affects the natural environment and the social and economic stability of the country. The Ministry of Environment and National Beautification leads the Environmental Management Programmes and the National Strategy Plan 2006–2025 in the country, which includes building a green economy and the establishment of a sustainable development agenda. Barbados Fisheries Management Plan 2004–2006 establishes the Guiding Principles for managing fisheries in the country, such as maintaining biodiversity and using ecosystem management approaches. However, there are no specific policies for the protection and conservation of biodiversity in the fisheries sector.

Regarding the fishing sector, the Fisheries Policy for Grenada includes ecosystem conservation issues and was formulated with the participation of different stakeholders, including associations. Likewise, the sector is prioritised within the Nationally Determined Contributions (NDC), and it is on the list of priority sectors in Grenada, according to the Blue Growth Coastal Master Plan. In addition the country has agreements/conventions for maritime protection.

However, despite these, at present there is no regulatory framework for the three countries that integrates fisheries and aquaculture with climate change mitigation and adaptation. Furthermore, fisheries are still loosely included in the broader concept of biodiversity. This could be considered a key missed opportunity, where efforts for biodiversity conservation and climate change mitigation, particularly through Nature Based Solutions (NBS), could particularly benefit the fisheries. Fisheries rely heavily on coastal ecosystems for the provision of services, therefore investing into mechanisms that integrate biodiversity and climate change into fisheries policy and actions, is an area that should be prioritised.

The existing demand for fishery products within the Caribbean region presents a significant opportunity. The demand across the region is guaranteed, and with increasing Blue Economy developments, there is a similar increase in purchasing power, as is being seen in Barbados, Grenada, and St. Vincent and the Grenadines. The purchasing power of the Caribbean population is also on the rise as the GDP per capita is increasing on average [59]. The population of the three countries will therefore have access to more fish on the local markets, the price of which will be similar, possibly even the same, as export fish prices. The economic growth occurring in the Caribbean nations and its industries allows for local buying of fish before sending to export, which in itself is beneficial as it is always far easier to supply a local market than an international one, with fewer risks, less exposure to external shocks, and minimising of problems regarding product origins and certifications. The importance of the local market and with it the prioritising of support for the Caribbean’s needs first before exporting, could result in the region as a whole becoming net exporting countries rather than each country being an individual net exporter. It is speculated that the reason for a limited amount of intra-regional trade in fish products in previous years was due to reduced buying power of locals, high-quality fish products being reserved for well-paying tourists, limited fish processing capacity for particular species, as well as changes in diet over the years [60].

In terms of constraints associated with the export issue in SVG, 17% of the fish catch is exported, mainly to the United States. Despite the fact that fish trade is crucial for food security (fish in cans and salted fish are used during emergencies and the hurricane season), St. Vincent has a trade deficit where imports exceed exports at a ratio of 3:1. The government fish market purchases 10% of all landings. The government fish market has the technical capacity to process and package fish but the demand for processed fish is limited, resulting in the underutilisation of the facility. A result of the underutilisation of the facility is that 136,000 kg of fish by-products (scales, guts, fins etc.) are discarded annually. Similarly, in Grenada, the United States of America takes more than 90% of total seafood exports. Grenada is also a net exporting country of fishery products, with exports three times the import value. Barbados, has particularly high per capita fish consumption imports at 80% of fish [61], making it the biggest net importer of fish between the three nations.

In this regard, intra-regional trade presents a further opportunity for fisheries to increase their contribution to the regional economic market. Therefore, intra-Caribbean trade should be a key priority for investment. Only a very small percentage of exports from the three countries are intra-regional. It is important that the three countries continue to trade with the outside world, but lessen its susceptibility to external shocks by increasing intra-Caribbean trade and restricting exports, and thereby ensuring that the respective nation’s nutritional and domestic market needs are met. This promotion of intra-regional trade provides a positive response to many challenges, while enhancing the countries’ capabilities, and improving their readiness to compete on international markets (43].

There is a need to facilitate a more streamlined method of transporting fish products across borders to encourage intra-regional trade. Barbados, Grenada, and St. Vincent and the Grenadines, together with other CRFM members, need to ensure that intra-regional trade is not hampered by a complicated import/export approval process. This could be achieved by unifying the import/export declarations and phytosanitary inspections within the same government agency. A zero percent preferential tariff for intra-regional trade could be set so that fish imports/exports would not face any restrictions [62]. The systems currently operational at the ports of arrival would also benefit intra-regional trade by being updated, thereby further reducing travel time for both passenger and freight vessels. A system of common conformity assessment procedures to be utilised by all countries for the testing, inspection and certifying of fish products for import/export, would reduce confusion regarding the standards required in the trade of fish, and ensure that all products on the market comply with all legislative and food safety requirements [63].

Value addition of fishThe key element that enables optimum profit or gains from fish products is that of value addition; creating needed employment and foreign currency earnings. The three countries can explore the area of preparing ready-to-cook and ready-cooked meals that developed countries are increasingly attracted to, and which would provide a better price for their fish products than exporting unprocessed fish to American markets or other countries.

The concept of value addition substantially enhances the benefits from the fishing industry, thereby gaining more from less catch. The countries need the technology and resources to enable them to meet the processing, packaging, and marketing requirements for the target markets, however such technology is monetarily expensive and often needs to be imported from elsewhere which increases the startup costs required for developing the value addition of a country in the Caribbean. Government planning needs to prioritise value addition within the seafood value chain and (i) encourage private investors to invest in seafood value addition, by the government zero-rating imported value addition machinery (ii) realising the importance of training initiatives for seafood producers to equip them with the skills and knowledge needed to function at various stages of the value chain (iii) there is a need to study, reaccess, and if need be redefine, the seafood chain to streamline bottlenecks and operational challenges (iv) continue to market development and diversification, and (v) establish information centres to provide the various operators at the various chain nodes with the necessary information needed for planning of investment decision making. However, as likely happened in the past, government expenditure may have been directed elsewhere, with the prevalence of more immediately pressing matters such as recovery efforts from natural disasters (hurricanes, severe storms, COVID-19 pandemic), as is well-known of the Caribbean region, where immediate human welfare was of major concern.

As an example, Barbados is exploring further opportunity to valorise the fishery sector by increasing the value of tuna caught for export. With investment in this area, providing the deep-water fishing industry with the tools needed to move up the tuna value chain and away from the low-value unprocessed whole fish currently exported, towards freshly boxed loins for export, the income to the Blue Economy through the fisheries sector could increase over 20-fold by the end of the present decade [64]. By processing the tuna before export, the local fishing industry could capture much more of the final price that consumers pay, resulting in a transformation of the island’s fishing industry. By improving fleet efficiency, quality controls and infrastructure, and complying with sustainability certifications, the fishery would open itself up to fast-growing markets. Although this endeavour looks at exports, improved value from the tuna sector would better serve local hotels and restaurants, and retain more value on the island decreasing dependence on food imports.

Improving ecosystem services provisionWithout healthy ecosystems, the provision of fishery resources diminishes. Overall, the coastal and marine ecosystems around Barbados, Grenada, and St. Vincent and the Grenadines are significantly degraded (as outlined earlier in this manuscript), with the effects on the fisheries and fish catches severe. Mismanaged and unsustainable fishing practices (non-targeted bycatch, inefficient fishing gear, overfishing) also deteriorate the health of the ecosystem in which they are used.

In order to maintain the ability of ecosystems related to fisheries and aquaculture to continue to provide services, ecosystems need better valuing of their services and increased restoration (in the form of well-managed fisheries, closed seasons to allow the natural stocks and environment to recover, sustainable resource extraction such as using sustainable fishing gear, and an ecosystem-approach to sustainable resource management). In this way, improving the condition of coastal and marine ecosystems presents an opportunity to improve the capacity of fisheries by 50%–60% [65].

There is an immense gap in the knowledge pertaining to the state of ecosystems. An effective understanding of ecosystems is needed to measure baselines and progress in this area. The three nations, together with regional committees, will need to satisfactorily quantify and qualify the economic value of the ecosystem services that are provided by the coastal environments. Current ecosystem services valuation reveals a two-fold incapacity in current policy making, neither giving the services full economic weight nor accounting sufficiently for the environmental damage caused by human activity. Valuating ecosystem services and anthropogenic degradation of the environment, will assist in creating market-based mechanisms to pay for such services or compensate for any damages caused. Therefore, allocating value to biodiversity undisputely contributes to all efforts made towards marine resources conservation and sustainable exploitation.

Ecosystem services valuation would provide a strongly integrated, multi-sector management tool, consolidating knowledge from the different areas of ecology, biology, economics and social sciences—and would be conveyed in a monetary form which is understood by all. Valuating ecosystem services would provide two important policy tools: the ability to offset the costs of marine ecosystems’ degradation and destruction, while assisting in defining the environmental status of the ecosystems to determine areas requiring urgent attention. The shifting of the valuating of the ecosystem services from that of reference monetary unit values is approximate and therefore needs to be dealt with extreme care. This method however, has the benefit of being easily implemented in data-poor regions, such as Bermuda, Grenada, and St. Vincent and the Grenadines. The unit reference values of ecosystems can be used regionally and requiring only small adaptations, considering the GDP, socio-economic, and environmental factors. Fortunately, there are a range of appropriate tools available for environmental accounting. One such tool is the Natural Capital Project’s InVEST (Integrated Valuation of Ecosystem Services and Trade-offs) that offers a range of open-access software tools for valuing natural capital, however, large amounts of data are required for its effective use and a concerted effort at data collection in conjunction with its use is advocated for.

Increasing the role of MPAs as a fisheries management toolMarine protected areas (MPAs) and harvest control are incentive fisheries management tools that have been tested over time. MPAs have been extensively researched and have been shown to aid fish abundance, increased biomass, preservation of habitat health, reduction in mortality, and improved growth and reproduction [66,67]. The benefits of these MPAs extend beyond the MPA itself and into the surrounding waters [68,69]. But, the disadvantages of MPAs in comparison to the benefits are considered to be context-dependent [70–72]. To illustrate this point, one such example is that the creation of an MPA reduces the available fishing grounds accessible to fishermen, however, at the same time MPAs can be created where fishing is not a primary activity in the first place and thus little impact to the livelihood of fishermen take place. Where in such instances fishing is not the activity responsible for ecosystem degradation, the MPA would serve to regulate and manage other forms of resource extraction from that area.

A comprehensive understanding of species distribution and the habitat relationships therein, is essential in ensuring the success of MPAs, which is regularly found to be inadequate in existing protected areas worldwide. Detailed information on species distributions and habitat preferences is often inadequate and can severely compromise their successful protection even when occuring within designated MPAs [73]. It is critical that each MPA has its own individual management plans developed and implemented. The determining elements of sustainable management of fisheries, economic prosperity, the location, size, and habitats it contains, its connectivity to other MPAs, and the quality of local stakeholders’ participation in its management are is what make an effective MPA [74].

The positive benefit to fisheries of MPAs increases through the provision of services if the ecological habitat is maintained and/or restored to a high level. On this note, MPAs should not only be used for conservation purposes but also require improved management of current MPAs, which together with networking of the MPAs should be part of a focused effort for fisheries management. Areas that have proven to have a high contribution to fishery resources are where MPAs should be designed and managed. To this end, no-take zones that prohibits all fishing activity are necessary to ensure any lasting influence on fish stocks and the export of biomass. It is essential to have rules in place to control and inhibit fishing around the periphery of MPAs for the efforts of MPAs to be realised. Furthermore, MPA management for fisheries needs to be conducted together with additional measures and not as an independent socio-economic conservation measure, which would then increase the services to the whole of EEZ.

As an example, in the case of Martinique, the abundance of aquatic populations associated with fishery closures within the marine managed areas around the island, can be multiplied by a factor of 2 to 10 [75]. The losses of the closed period thus seem to be globally compensated by the adaptive strategies of fishermen and the upsurge in catches during reopenings [76]. However, since then several of the no-take zones have been reopened to fisheries and some of the MPAs have been fished illegally by poachers. This emphasises the necessity for sufficient and appropriate enforcement or incentive measures to maintain no-take zones for the effectiveness to be realised over the long-term.

Beyond simply as a tool for fisheries, MPAs also offer significant opportunity for the eco-tourism sector to benefit from the services they provide. In this way, the development of the marine protected areas provides avenues for the fisheries and tourism to collaborate with other government, private sector, and donor agencies in the acquisition of resources, expertise, and technical knowledge associated with the Blue Economy, which helps address some of the challenges of the sector. However, the establishment of an increased number of MPAs may be a source of new emerging conflicts if fishermen do not or cannot convert to a tourism-based livelihood (due to a lack of skills or having to convert vessels to support tourism). Adequate support structures and education surrounding the opportunities in ecotourism may be required for the implementation of an increased number of MPAs. The culture and traditional fishing methods of fisherfolk can be used to leverage this transition to ecotourism, by sharing and monetising the experience for tourists.

Expansion of Aquaculture Scaling up of aquaculure and maricultureScaling up aquaculture and mariculture as part of wider Blue Economy development presents a means with significant potential to increase revenue. Currently a missed opportunity, creating an enabling environment for aquaculture should be a key priority for investment. Presently the contribution of Barbados, Grenada, and St. Vincent and the Grenadines combined was less than 0.5% of the global share in 2018 [53], highlighting the significant lag of mariculture development. With the collective fish stocks predominantly at or above their sustainable limit, fisheries offer decreasing capacity. Given that the Caribbean region has a high per capita consumption of fish (> 20kg/per capita), the demand on fish supply is only going to increase with increasing population sizes, and the decreasing ability of wild fish stocks to meet demand. Using investment directed at the development of the Blue Economy, upscaling aquaculture and mariculture offers the potential to optimise the benefits received from the development of the marine environment, create sustainable, quality employment, and offer high-value commodities for both export and the domestic market. This area also offers the potential to develop further economic opportunities up- and downstream of the mariculture and aquaculture ventures themselves, creating further livelihoods. Investment should be directed towards the creation of an enabling environment in which aquaculture operations can flourish, with the required support structures in place (such as veterinary services and distribution chains) to encourage further development. Among some relevant initiatives, it is worth highlighting Earth Ocean Farms in Mexico, where using open sea aquaculture technology, they cultivate totoaba (endangered species) and red snapper (Lutjanus purpureus, also called ‘huachinango’) in their natural environment through cages that are introduced into deep waters and with ideal conditions for their growth. They are also collaborating in a restocking program aiming to recover the totoaba by releasing juveniles grown in a hatchery, back to the wild.

Essential for further development of mariculture is the harnessing of external capabilities. In Asia, practitioners are experienced in mariculture activities [77] and therefore connecting with these practitioners would provide a valuable resource for the development of mariculture in Caribbean regions. Furthermore, cultivating these connections could provide a significant investment opportunity for international development agencies, while providing a passageway to engaging in purposeful development of mariculture [63]. These expert practitioners could deliver key pilot projects that would provide training and capacity building, while developing strategies that prioritises national development in aquaculture and mariculture. In this regard, there needs to be adequate practices supported by strong legislative frameworks, to ensure the sustainability of this sector and preserve the economic interests of farmers.

Aquaculture financing could happen both at the level of individual projects and at a national level. On a project level, countries that have some aquaculture can mobilise financing for securing production and environmental quality of aquaculture. This can also be promoted through financing of research-based institutions that support aquaculture developers. On a national level, financing is needed for not only creating but, just as importantly, for ensuring that public authorities have the capacity to execute national policies. In Martinique, for example, local support for aquaculture development exists and is aided by local and international (EU) funding mechanisms. Aquaculture research institutions such as ‘Delegation Ifremer des Antilles Francaise’ (IFREMER) can facilitate collaboration projects to further the development of aquaculture on the island and in the region on a bigger scale. However, as of yet, there is limited local trade in aquacultured products and this presents somewhat of a ‘chicken-and-egg’ scenario where this positive feedback loop can hinder the uptake of aquaculture development.

While the argument for transition to sustainable fisheries is potentially more necessary than aquaculture development, the benefits from doing so will only be realised once natural environments and fish populations have recovered (which may take a number of seasons), and the appropriate sustainable exploitation thereof ironed out. The benefits from aquaculture development, including job creation, entrepreneurship, skills development, increased food security, and potentially circular resource use, can be realised more expediently than the transition to sustainable fisheries.

AquaponicsIntegrating aquaponics into Blue Economy development strategies alongside fisheries and aquaculture provides a pathway to realise the sustainable intensification of fisheries, aquaculture, food and agriculture. Aquaponics reintroduces biological complexity into agricultural systems, closely guided by knowledge co-creation and sharing processes that aim to maximise synergies. In other words, aquaponics does more, with less. Tackling the region’s high food import bill and improving food security is increasingly being explored through aquaponics. An aquaponics industry can facilitate the rearing of fish for high-value protein concurrently with a range of vegetables and other produce, which as an import substitution measure can help reduce dependence on these foreign imports. Depending on market trends, crop production can be rapidly accelerated according to the local, tourism, and export demands. However, it is important to have access to markets that are willing to pay higher prices for superior quality produce. Costs for both construction and operating of aquaponics is fairly high. These expenses cannot be recovered, and the aquaponic initiative may not be profitable without access to, and leverage, in the markets. Certainly, a great deal of aquaponic businesses in the world have failed—typically due to poor business planning and marketing strategies, rather than production-related issues.

There is signficant potential in all three countries to develop aquaponics, especially in St. Vincent and the Grenadines, where the country is facing two key issues. Firstly, the collective of small islands face a significant constraint related to the limited availability of fresh water, which limits food production. Secondly, transport limitations constrain the availability of food and production as everything that comes from Kingston is particularly expensive. Given the nature of aquaponics, these issues could be mitigated, and a sustainable supply of fish and vegetables could be provided to the various islands without the need for massive amounts of water, as these systems can function using rainfall. In this regard, investment opportunities are wide, with the innovation and research into aquaponics expanding at a rapid rate.

Alternative and emerging industriesTo achieve scalable growth of aquaculture, investing in avenues that enhance existing relationships with other sectors, as well as encouraging new ones, should be explored. In this way, alternative and emerging industries related to aquaculture provide a wealth of opportunities.

There is the potential to create synergies between the aquaculture and biomedical industries where products or byproducts from aquaculture can provide further resources for alternative biomedical application. As an example, aquaculture farmed tilapia skin is used to treat burns of the first and second degree patients in northern Brazil [78]. The skin, previously considered a waste product of the fish bred for widespread consumption, apparently has high levels of collagen, protects against infection, increases healing time, and reduces the need for pain medication [79]. As such, tilapia skin provides a cost effective means to integrate the aquaculture industry with the medical one, in a way that requires no further development beyond aquaculture initiatives to increase fishery products for food security, livelihoods and economic development.

Similarly, species of Rhodophyta or red algae, specifically Irish Sea Moss, found in the Caribbean, possess unique compounds with several properties that provide a number of potential health benefits, which make them valuable compounds to be involved in biotechnological applications [80,81]. The use of seaweeds in agriculture is also highly relevant as they have the ability to increase crop yields as fertilisers, and assure soils and crops are less laden with chemicals [82]. In this regard, proliferating mariculture for the addition of seaweed extracts in food processing, nutraceutical, pharmaceutical, and industrial processing, offers significant areas of investment in the Blue Economy that increases the connectivity of sectors and the generation of incomes.

Contrastingly, given the influx of Sargassum present in the Caribbean region and naturally the three target countries, there is an opportunity for the funding of projects that utilise this resource as a means to expand aquaculture and benefit the fishery industry (among others). As such, there is an initiative being developed under the Blue Tech Challenge (launched by the Inter-American Development Bank) in Saint Lucia which converts Sargassum seaweed into organic bio-fertilizer. There are similar initiatives in Barbados and Dominica. This is an interesting solution to fight the Sargassum proliferation that benefits the expansion of aquaculture/mariculture activities through synergies with other industry. Challenges with the use of the seaweed biomass include the concentration of heavy metals and chemicals like hydrogen sulfide in its tissues while at sea, however these seaweed blooms can still be leveraged as has been described in [83]. Appropriate regulations for the use of these algae for consumption and as fertilisers need to be established throughout the Caribbean region, particularly with respect to the processing requirements and specifics in removing potentially (environmentally) harmful substances from the biomass.

Integrating Fisheries and Aquaculture into the Wider Blue EconomyIn the context of the Blue Economy development at country levels, fisheries and aquaculture should be considered as a priority. It will continue to be the main animal protein provider to the population as well as the main job provider, even increasingly so with the uptake of efforts to develop aquaculture and aquaponics. These three sectors can also be a key contributor to the wealth creation if the value addition is made within each country and not in the exporting one. As the main observer of changes at sea, fisheries must play a central role in both the preservation of key habitats and the rehabilitation of degraded ones. This is possible within the Blue Economy approach that promotes the articulation of marine biodiversity with coastal habitats, for elaborating solutions that are beneficial from the biodiversity as well as the climate change mitigation and adaptation points of view. As such, fisheries and aquaculture have a bright future in the Blue Economy perspective of Barbados, Grenada, and St. Vincent and the Grenadines.

All three countries are facing strategic and technical challenges for the implementation of Blue Economy. These challenges are transversal to all sectors and components of Blue Economy, and in this way hinder the valorisation of the fishery and aquaculture sectors given their key importance as sectors within the Blue Economy and more precisely, insufficient structuring of the implementation of Blue Economy. Barbados has taken a bold step in establishing a Ministry of Maritime Affairs and the Blue Economy in 2018, while the OECS, including Grenada and Saint Vincent and the Grenadines, have benefited from a number of regional initiatives to accelerate the research and development of the Blue Economy in these countries. Despite this progress made to date in the preparation of Blue Economy, important problems remain in the institutional organisation. As such, there are limited coordination mechanisms and no supraministerial entity to drive the development of the Blue Economy, and sectoral approaches still dominate. Consequently, this limits the countries’ ability to effectively formulate and implement Blue Growth policies, as well as policies to protect the environment and improve ecosystem health by applying the concept of Blue Economy. There is furthermore a growing confusion about the role of the state for each country because of a lack of strong signals of commitment, particularly with regard to emerging activities. Thus, the structuration of the Blue Economy should be the first priority and precedes all other interventions.

Absence of accounting for Blue Economy activities and components. Accounting for Blue Economy activities and components is not done in a unified manner. Currently data have to be collected from different sources to provide a comprehensive view of the Blue Economy contribution to creating added value and creating jobs. For some sectors, such as ship maintenance for instance, data is not recorded. An appropriate system of national accounting would ease recording annual changes in economic sectors. In the same way, ecological components of Blue Economy aren’t accounted for despite the ecosystem services that coastal areas provide and their importance in mitigating hurricane effects. However, with the implementation of nationally determined contributions, green and blue accounting should emerge and become the cornerstone for assessing specific actions relating to climate change.

There is an absence of an integrated and prospective approach to marine ecosystems and spatiotemporal management tools. Neither of the countries have fully institutionalised the large marine ecosystem approach yet (Caribbean LME). However, this would help to understand the evolution of coastal and marine ecosystems using a set of ecological indicators, namely biological productivity (particularly fish biomass), pollution (plastic and chemical among others), and ecosystem health. Consequently, the actual resource and ecosystem management is less efficient. Maritime spatial planning (MSP) is also lacking in all three countries, where neither of them has an implemented plan.

In addition to a significant reduction in the amount of overseas development assistance (ODA) allocated to the Caribbean, the objectives of development funding have shifted from broad poverty reduction, health, and education, to environmental and climate change-related targets. The share of ODA allocated for environmental protection has increased from an average of 4.1% between 2003 and 2007, to an average of 8.2% between 2012 and 2016, reflecting the shift in focus towards the environment and climate change [84]. Despite close alignment of environmental and climate change objectives to the Blue Economy, the Caribbean’s ability to access funding remains challenging. Weak capacity for project identification, as well as development of proposals and their implementation, are the most prevalent factors affecting the ability of many Caribbean countries to access finance and complete projects. Therefore, accessing ODA for development of the Blue Economy will require a combination of concessional finance and technical support.

The need for concessional financing, ODA and technical support are particularly relevant for countries that have limited fiscal capacity due to external development constraints. One critical issue is the liquidity constraints that SIDS may risk in the short term [85], even if they may potentially not face long-term solvency issues. Because of the high costs of lending, it is difficult to refinance debt or they will have their economic growth and potential for public investment constrained by borrowed costs. Small, open economies that are considered uncertain by international capital owners, can face risks to their national capital accounts as crises (such as the COVID-19 pandemic) can result in capital departures.

At present, insufficient or inadequate infrastructure are in place for the valorisation of the fishery sector, or expansion of aquaculture. Presently, fisheries and aquaculture policies are not aligned to the Blue Economy or integrated into national or regional planning in this way. The Blue Economy in the context of the three countries is still in the early stages of development. Despite the wealth of resources and potential for integrated Blue Economy approaches, the pace of uptake has been relatively slow. Grenada is the first OECS member country to develop a vision for its Blue Growth economy. Grenada’s Blue Growth vision is to optimise the coastal, marine, and ocean resources, to become a world leader and international prototype for Blue Growth and sustainability.

Comprehensive planning and capacity development is needed to bring sectors and industries together. The potential is significant, provided the appropriate investments are made, but the existing regulatory and policy environment to attract investment and funding for the Blue Economy (and thus the fisheries) is lacking. The development of a the Blue Economy as a sector of each country could generate the synergies needed to facilitate finance.

Similarly, banking mechanisms are lacking, with underdeveloped financial markets. In this regard, a transparent policy framework that follows emerging blue finance principles (such as UNEP FI principles) could engender investor confidence. Generating an enabling environment for sustainable finance of the fisheries in the context of the wider Blue Economy will require particular attention, especially in the context of overcoming national debt. The recent Caribbean Blue Economic Financing Project (Caribbean BlueFin) presents an opportunity to enhance the capacity of a selected number of countries and create the enabling environment for private sector engagement and investment in the Blue Economy.

Financing for aquaculture and fisheries could happen both at the level of individual projects and at a national level. On a project level, countries that have some aquaculture can mobilise financing for securing production and environmental quality of aquaculture. This can also be promoted through financing of research-based institutions that support aquaculture developers. On a national level, financing is needed for not only creating but, just as importantly, for ensuring that public authorities have the capacity to execute national policies.