Location: Home >> Detail

J Sustain Res. 2024;6(2):e240020. https://doi.org/10.20900/jsr20240020

,

Wallapa Suengkamolpisut 2,

Selim Ahmed 3,

Sabrina Maria Sarkar 4

,

Wallapa Suengkamolpisut 2,

Selim Ahmed 3,

Sabrina Maria Sarkar 4

1 BGC Trust University Bangladesh, Chittagong 4381, Bangladesh

2 Business Administration Division, Mahidol University International College, Mahidol University, Salaya 73170, Thailand

3 Department of Business Administration, World University of Bangladesh, Uttara, Dhaka 1230, Bangladesh

4 Department of Public Policy, CIES, ISCTE-IUL, Lisbon 1649-026, Portugal

* Correspondence: Bablu Kumar Dhar.

The demand for sustainable housing in Bangladesh is increasing as the country experiences rapid urbanization. This study investigates the role of Islamic banks in facilitating green housing finance, a critical yet underexplored aspect of the region’s economic development. The novelty of this work lies in its focus on Islamic banking’s contribution to sustainable development goals through housing finance, an area with significant potential for strategic impacts on both environmental sustainability and economic growth. Utilizing a mixed-methods approach, we collected primary data through surveys of 400 borrowers and secondary data from bank reports and industry publications within the Chittagong Division. Current analysis reveals that Islamic banks are pivotal in meeting the growing demands for eco-friendly housing by providing innovative financial solutions that align with Shariah principles. The findings indicate that Islamic banks not only enhance borrower satisfaction but also stimulate market growth for sustainable housing. This study contributes to the broader discourse on green finance and proposes strategic recommendations for policymakers and financial institutions aiming to expand green housing initiatives.

The pursuit of sustainability in housing finance has become a global imperative as urban populations swell and environmental concerns escalate. In Bangladesh, where rapid urbanization strains both environmental and housing resources, the role of financial institutions, particularly Islamic banks, in supporting sustainable development initiatives is increasingly crucial. This study delves into the unique contributions of Islamic banks to green housing finance, a critical area that combines financial innovation with environmental stewardship. The focus on Islamic banking is particularly relevant given the alignment of Shariah principles with sustainable development goals, which emphasize not only economic growth but also social and environmental wellbeing.

In Bangladesh, sustainable housing financing focuses on vertical growth to address the increasing demand for lodging due to the country’s high population density and limited land availability. This approach acknowledges housing as a basic human need, essential for determining one’s socio-economic standing, along with food, clothes, health, and education. The government is crucial in offering environmentally friendly housing options to different socio-economic groups, emphasizing the significance of sustainable living spaces that promote the welfare and financial security of its residents [1].

The growing need for sustainable home finance options is becoming crucial due to the rising demand for urban homes [2–6]. The promotion of green housing financing aims to strengthen economic activity and provide social benefits including improved savings, expanded mobility, and higher investment in environmentally suitable living environments [7]. The existing sustainable financing choices are insufficient in terms of availability and quantity. This study examines how Islamic banks in the Chittagong region of Bangladesh contribute to developing ecologically friendly housing construction.

In sustainable finance housing, the emphasis is on bridging the gap between the demand for eco-friendly housing and the available funding options in Bangladesh [8–11]. Although there is a growing demand for sustainable housing, the industry struggles with a significant shortfall in deposit collecting when compared to conventional commercial banks [12,13]. The results indicate the possibility of financial institutions aligning their interests with sustainable development objectives by modifying loan and deposit policies to promote green housing projects [14–18]. This involves delivering loans that support energy-efficient and environmentally friendly housing developments, as well as providing competitive rates and flexible repayment alternatives to promote investment in sustainable living environments. The focus is on empowering Islamic banks to expand their presence in rural regions, providing guidance on green finance, and following principles that promote environmental responsibility.

The updated emphasis on the difficulties in the home finance industry, specifically related to sustainable housing financing, including insufficient amenities, poor consumer knowledge, discontent, excessive interest rates, and restricted funding options [19–21]. Financial institutions, notably Islamic banks, are making efforts to provide goods and financing solutions to meet the increasing demand for eco-friendly homes in Bangladesh [22,23]. The research intends to investigate how Islamic banks contribute to improving borrower satisfaction in sustainable housing finance, emphasizing the importance of evaluating their involvement in meeting the demand for green housing financing among borrowers. To synchronize the study’s goals with the notion of sustainable financing in housing: evaluate the efficiency of Islamic banks in offering eco-friendly home financing options in Bangladesh, with an emphasis on borrower contentment. This entails assessing the extent to which these banks satisfy client expectations for eco-friendly home financing alternatives, and, assess the ability of Islamic banks to fulfill the increasing need for sustainable home financing in Bangladesh. This involves examining how Islamic financial products and services meet the requirements of borrowers interested in investing in environmentally friendly and sustainable housing developments.

The research examines the vital role of Islamic banks in offering sustainable housing financing in Bangladesh, with the goal of assessing their influence on the capacity of low- and middle-income people to purchase environmentally suitable dwellings. The study examines the cost-effectiveness of financing green housing, the satisfaction of borrowers with Islamic banks’ green financing, and the banks’ success in addressing the demand-supply gap in sustainable housing. The study aims to provide insights on how Islamic banks may improve their services to better line with sustainable housing objectives and contribute to the development of policies for green housing financing. The significance of this research lies in its examination of how regulatory frameworks and bank-firm relationships facilitate or hinder the adoption of green finance practices within the context of Islamic banking. By understanding these dynamics, the study aims to provide insights that could help shape policies and strategies to enhance the efficacy of sustainable finance. This analysis is vital for stakeholders across the spectrum, including policymakers, financial institutions, and developers, as they navigate the complexities of integrating sustainability into the housing finance sector. Such integration is not only crucial for achieving broader environmental goals but also for ensuring economic stability and improving the quality of life for residents.

Housing includes the industry, financing, and other services in the sustainable development field. Due to its significance, a multitude of research, publications, and reports have been conducted on a worldwide and local scale. The materials provide insights into the problems and potential in sustainable housing finance, novel financing structures, and the role of financial institutions, such as Islamic banks, in supporting eco-friendly housing solutions [24]. This study establishes the groundwork for improving sustainable housing financing practices.

The literature on sustainable housing finance examines how environmental sustainability concepts might be incorporated into housing finance structures [25]. Research examines how financial organizations, such as Islamic banks, might provide funding choices to promote the building and buying of energy-efficient and eco-friendly houses [1,5,6]. They analyze the significance of green bonds, sustainability requirements in loan approvals, and the influence of such financing on decreasing carbon footprints [26,27]. Research indicates the difficulties in matching financial products with sustainable housing objectives, including increased upfront expenses and the need for regulatory assistance to promote environmentally friendly investments in the housing industry.

The updated review of literature now covers research from countries that have delved into housing finance using a mix of similar and different approaches. For instance, a study, by Ahmed and colleagues [15] in Malaysia showed how Islamic financial products play a role in supporting housing initiatives indicating a rising interest among Islamic banks in incorporating environmentally friendly building principles. Similarly research in the United Arab Emirates by Al Mamun and team [28] highlighted the increasing involvement of banks in funding projects that meet standards thereby promoting environmental sustainability.

Comparative analyses like those conducted by Jan et al. [5] and Lagoarde-Segot [29] have examined how Islamic banks in Indonesia and Turkey have embraced practices within housing finance. These studies often uncover hurdles and innovative solutions such as the utilization of sukuk and other Shariah compliant financial tools specifically designed for eco-friendly endeavors. These global perspectives offer insights into assessing the role of banks in Bangladesh presenting a reference point for evaluating international best practices and potential areas, for policy improvement.

Sustainable Housing Finance in BangladeshWithin Bangladesh, the role of Islamic banks in supporting sustainable housing has been less extensively covered, marking a significant gap that this study aims to fill. Previous local studies have primarily focused on the general performance of Islamic banking without a specific emphasis on their contribution to sustainable housing finance. For instance, research by Uddin et al. [1] explored the broader impacts of Islamic banking principles on economic sustainability in Bangladesh, suggesting potential alignments with green financing but not delving into specific case studies or empirical evidence related to housing.

This study contributes to the local body of knowledge by providing detailed empirical analysis on how Islamic banks in the Chittagong region engage in and promote sustainable housing finance. By comparing our findings with those of previous local studies, such as those by Dhar et al. [8] and Gazi et al. [12], we can identify unique trends and challenges in the Bangladeshi context. This comparison not only highlights the innovative approaches taken by Islamic banks in Bangladesh but also aligns with the global shift towards integrating sustainability into financial practices.

Sustainable housing aims to reduce the environmental impact of living areas while also focusing on affordability, health, and social fairness. The product incorporates sustainable materials and energy-efficient features to minimize greenhouse gas emissions, which is crucial in addressing global climate change. Sustainable housing, with its emphasis on durability and minimal maintenance, provides economic sustainability by decreasing long-term expenditures for residents [6,30]. It highlights inclusion and accessibility, making sure that sustainable living is available to many socioeconomic classes. Sustainable housing enhances community resilience by helping people better endure and adjust to environmental and economic difficulties [31]. Sustainable housing aims to achieve a healthy balance between human habitation and the natural environment [32] by using innovative building methods and efficient resource management, thereby promoting a healthier world for future generations.

In Bangladesh, the housing finance sector is marked by an increasing need for affordable housing due to rapid urbanization and economic expansion [33,34]. The housing financing industry often fails to fulfill the demand, especially for poor and middle-income households. Conventional housing financing approaches in Bangladesh have not adequately met the need for cost-effective, high-quality homes, and have not given importance to environmental sustainability [35]. The lack of financial solutions specifically designed to help the building and purchase of environmentally friendly houses highlights a gap in sustainable housing financing [8,16]. Financial institutions, especially Islamic banks, may take advantage of this gap to develop and broaden their sustainable home financing services via innovation. By doing this, they may have a significant impact on encouraging sustainable development, in line with Islamic finance principles that prioritize social and environmental responsibility.

Islamic banks in Bangladesh might use their distinctive position to provide Shari’ah-compliant financing solutions that promote sustainable housing developments [1]. These items may include financing for constructing energy-efficient houses, installing renewable energy systems, or making enhancements to increase a home’s environmental sustainability [36]. Creating these products would adhere to Islamic financial norms and support initiatives to address climate change and advance sustainable development on both national and global scales.

Islamic banks and other financial institutions in Bangladesh must overcome certain hurdles to successfully establish and promote sustainable home financing. These factors include legislative obstacles, the need for heightened public knowledge and education on the advantages of sustainable housing, and the establishment of collaborations between developers, government entities, and non-governmental groups committed to sustainable development [37]. To overcome these obstacles, a focused and cooperative approach is needed from all parties engaged in housing financing and sustainable development.

Islamic Banking Principles and Sustainable FinanceIslamic banking principles and sustainable finance combine ethical finance with environmental responsibility [38]. Islamic finance, guided by principles such as the prohibition of interest (riba), risk-sharing, and asset-backing, intrinsically fosters social and economic fairness. The principles strongly correspond with sustainable development objectives (SDGs) by focusing on ethical investing, poverty alleviation, and fair wealth distribution [29]. Sustainable financing in Islamic banking, such as green sukuk, upholds ethical principles by promoting environmental protection [28]. Green sukuk finances initiatives that have good environmental effects, such renewable energy or sustainable agriculture, demonstrating how Islamic financing supports both economic sustainability and environmental conservation [39]. The combination of Islamic finance principles with sustainable finance efforts offers a comprehensive strategy to tackling global concerns by integrating financial sustainability with moral and ecological accountability.

Islamic banking incorporates sustainable finance by merging the ethical foundations of Islamic finance with the goals of environmental sustainability [40,41]. This strategy prioritizes investments in projects that have a favorable environmental outcome, closely in line with sustainable development objectives [42]. An important tool in this field is the green sukuk, a Shariah-compliant bond designed to finance renewable energy projects, green buildings, and other eco-friendly efforts [43]. These instruments enable investors to support sustainable initiatives while following Islamic financial rules, including the ban of interest and the need for asset-backing [44]. Islamic finance incorporates sustainability into its fundamental principles, providing a distinctive approach to backing environmental initiatives and demonstrating a dedication to ethical investment and environmental conservation.

Islamic banks have been in the forefront of incorporating sustainability into their financial products, particularly home finance. An example worth mentioning is the creation of green sukuk to finance environmentally friendly housing developments, providing a Shariah-compliant investment option that benefits the environment [43]. Islamic banks prioritize ethical and socially responsible investment, in line with sustainable development objectives, more than conventional banks. Conventional banks are beginning to incorporate green financing principles, but Islamic banks’ distinctive risk-sharing and asset-backed financing approach offers a unique way to support sustainable housing projects, showcasing a comprehensive dedication to financial inclusion and environmental responsibility [45,46].

The literature study on housing finance examines many aspects such as infrastructure, demand, and the functions of financial institutions. There is no particular research on the involvement of Islamic banks in sustainable home financing in Chittagong Division, Bangladesh. This study intends to address the research gap concerning the role of Islamic banks in sustainable housing finance. The study examines the extent to which Islamic banks effectively fulfill borrower requirements and address the need for sustainable housing financing, providing a unique analysis of their role in promoting environmentally friendly housing options. This study examines how Islamic banks can contribute to promoting sustainable housing finance in Bangladesh by analyzing borrower satisfaction with green financing options and the banks’ effectiveness in meeting the demand for sustainable housing finance. The study seeks to investigate the role of Islamic banks in promoting ecologically sustainable housing options, evaluating their influence on customer satisfaction and meeting the need for green housing financing in the nation. To align with the concept of sustainable housing finance, the study proposes hypotheses to investigate the impact of Islamic banks on this sector in Bangladesh:

H01: Islamic banks have no significant impact on sustainable housing finance in terms of borrower satisfaction.

H02: Islamic banks play no significant role in fulfilling the sustainable housing finance demand in Bangladesh.

Conversely, the alternative hypotheses posit:

Ha1: Islamic banks significantly contribute to sustainable housing finance, enhancing borrower satisfaction.

Ha2: Islamic banks play a crucial role in meeting the demand for sustainable housing finance in Bangladesh.

The research design adopted for the study is both descriptive and analytical in nature. In pursuance of the objectives and hypotheses, following methodology will be adopted. The universe of the study comprising of the borrowers of 8 Islamic banks of Chittagong Division in Bangladesh. The researcher selected 7 districts and 8 Islamic banks in those districts as they widely provided loan for housing. Borrowers were selected from last 10 years i.e., 2011–2018 as they had a reasonably long experience as a beneficiary. Cochran equation used to find out the sample size. Multistage sampling technique was followed.

To ensure a thorough understanding of the methods used in this study, we have adopted a mixed-methods approach, combining both qualitative insights and quantitative data analysis. This methodology allows for a comprehensive examination of the role of Islamic banks in promoting sustainable housing finance in the Chittagong Division. A detailed flowchart of the research process is included (see Figure 1), illustrating the sequential steps from the initial data collection through to the final analysis. This visual representation aids in clarifying the study’s design and helps articulate the interconnections between different phases of research.

Figure 1. Research Process Flowchart.

Figure 1. Research Process Flowchart.

The potential of this methodological approach lies in its ability to capture a wide array of data points, offering a robust analysis of borrower satisfaction and bank performance. However, it is important to acknowledge the limitations associated with this approach, including the potential for response bias and the challenges of generalizing findings across different regions or banking systems. By acknowledging these limitations, we aim to provide a balanced view of the strengths and weaknesses of our study, setting the stage for future research to build upon our methodology.

400 surveys were sent to borrowers using sustainable home financing alternatives from Islamic banks in Bangladesh, and all were completed, resulting in a 100% response rate. The data was examined using SPSS software to examine borrowers’ satisfaction with green finance options and their influence on encouraging sustainable housing practices. This method provides valuable information on how Islamic banks contribute to ecologically friendly home construction by offering financial solutions.

Socio-Economic Profile of RespondentsThe study in the sustainable housing financing sector showed a variety of demographics among borrowers from Islamic banks in Bangladesh, with a notable number falling in the 41–50 age group, suggesting a stage of advanced financial decision-making. Most of them were male, which aligns with the conventional gender norms related to financial obligations for housing. The majority of responders were married, reflecting a preference for secure family housing. The majority of the educational background was at the postgraduate level, demonstrating a strong understanding of home financing in Islamic banking. The employment situation was diverse, with most individuals being employed, indicating a reliable income for long-term home investments. Income levels were diverse, with a significant part in the upper-middle-class category, demonstrating the availability of Islamic banking’s sustainable house financing across various socioeconomic situations.

Borrowers Information Regarding Housing Loan from Islamic BanksThe data shows a diverse distribution of consumers across Islamic banks in Bangladesh, with loans mostly used for housing reasons including buying or building houses. Loan amounts mostly fell between 25–50 lacs, with a considerable number of borrowers choosing loan tenures of 6–10 years. The collateral predominantly included houses and flats, suggesting that loans were mainly requested for residential purposes. Payment installments varied significantly, indicating a range of financial capabilities among borrowers. Islamic banks play a crucial role in providing sustainable housing financing by giving flexible solutions to cater to various borrower requirements and encouraging ecologically responsible housing developments.

Descriptive AnalysisThe socio-economic profile of the respondents in our study indicates a predominant age group of 41–50 years, comprising 49.8% of the total, reflecting a mid-career stage prevalent among borrowers. Notably, males constitute 87% of the respondents, underscoring a significant gender disparity in accessing housing finance through Islamic banks. The marital status data reveal that a vast majority, 98.5%, are married, suggesting that family responsibilities might influence the decision to secure housing finance. Educational background analysis shows that 43.8% of borrowers hold postgraduate degrees, indicating a high level of awareness and understanding of Islamic banking products among educated individuals. Employment status is predominantly salaried (51.8%) or self-employed (39.8%), highlighting the economic diversity of the borrowers. The income profiles further classify 32% of respondents in the upper-middle income bracket, with monthly incomes exceeding Tk 120,000.

Loan data from Islamic banks reveals varied borrowing patterns, with 22.5% of the respondents’ obtaining loans from IBBL, indicating a preference or trust in specific banks. Loan amounts are generally within the 25–50 lacs range for 49.8% of borrowers, aligning with middle-class financial capabilities. The loan tenure predominantly ranges between 6 to 10 years (33%), suitable for long-term financial planning. Regarding collateral, buildings and flats are the most common (87.8%), supporting the primary purpose of these loans in purchasing or building homes. Monthly installments vary, with 30.3% of borrowers paying between Tk 31,000 and Tk 40,000, reflecting the financial obligations tied to middle and upper-middle-class borrowers. This comprehensive socio-economic and financial data provides critical insights into the demographics and behaviors of clients utilizing Islamic banking for housing finance in Bangladesh, illustrating the sector's reach and the financial habits of its clientele.

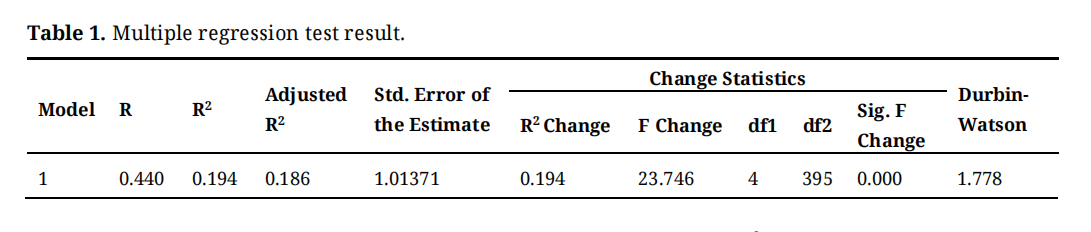

Inferential StatisticsAnalysis shows the results of the regression of independent variable against the dependent variable ‘Role of Islamic banks of Bangladesh in housing finance’. From the results, in Table 1, R (0.440) is the correlation of the independent variable with the dependent variable.

Table 1. Multiple regression test result.

Table 1. Multiple regression test result.

The coefficient of determination (R2) is used to investigate the contribution of an independent variable on the variance of the dependent variable. The result of the regression test on variables used in this research. According to the result of R2 which is 0.194 found by regression analysis shown in the table where p = 0.000 significant (R2 = 0.194, significance level or p-value, 0.000). The results also shown that 0.194 of the variances (R square) in Role of Islamic banks in housing finance in Bangladesh has been significantly explained by the independent variable. It shows that there is a poor correlation between the dependent and the independent variables. It indicates that Role of Islamic banks in housing finance in Bangladesh can only be explained by the independent variable at 19.4% while the rest at 80.6.0% is still left unexplained. There could be other factors or variables that could lead to the role of Islamic banks Bangladesh in housing finance.

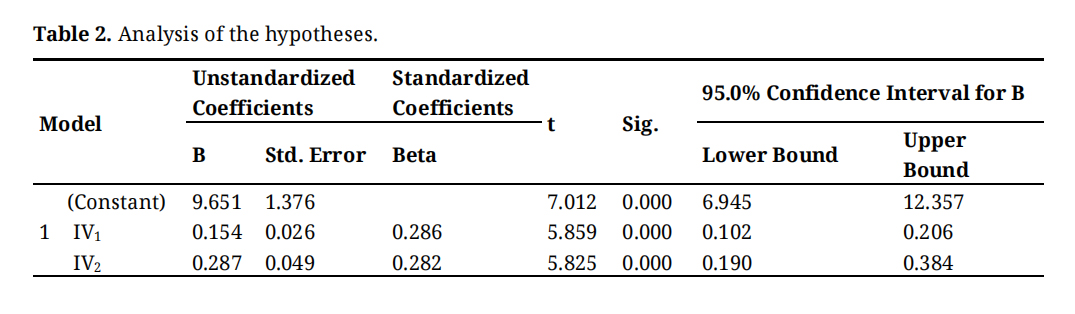

Table 2 presents the regression analysis results for two independent variables on the dependent variable. Both independent variables have significant positive effects, with unstandardized coefficients of 0.154 and 0.287, respectively, and p-values (Sig.) of 0.000. The analysis shows that the model’s constant is also significant, with a coefficient of 9.651.

Table 2. Analysis of the hypotheses.

Table 2. Analysis of the hypotheses.

Table 3. Result of the analysis of the hypotheses.

Table 3. Result of the analysis of the hypotheses.

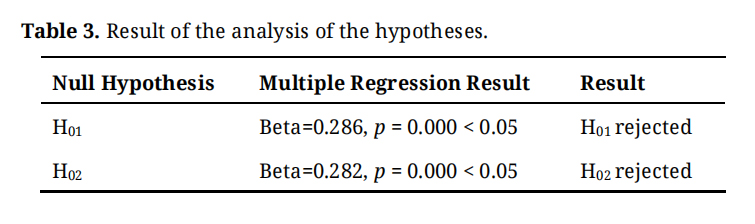

In Table 3, for H01, Beta = 0.286, p = 0.000 < 0.05 that means Null Hypothesis rejected and alternative hypothesis accepted. It can be interpreted as independent variable (Satisfaction of housing finance borrowers) has significant effect on the dependent variable (The role of Islamic banks of Bangladesh in housing finance) and for H02, Beta = 0.282, p = 0.000 < 0.05 that means Null Hypothesis rejected and alternative hypothesis accepted. It can be interpreted as independent variable (Demand-Supply) has significant effect on the dependent variable.

The regression results revealed that the role of banks of Bangladesh in housing finance has significant relation with borrower’s satisfaction. The direct relationship was supported by the effects of borrower’s satisfaction towards role of Islamic banks of Bangladesh in housing finance (p (0.05) > 0.000). However, in this study, the effect of borrower’s satisfaction on the role of Islamic banks of Bangladesh in housing finance is supported. Thus, H0 is rejected and Ha accepted.

The regression results revealed that Supply-Demand of housing finance has a significant relation with role of Islamic banks in housing finance in Bangladesh. The direct positive relationship was supported by the effects of Supply-Demand of housing finance towards role of Islamic banks in housing finance in Bangladesh (p = 0.05 > 0.000). Thus, H02 is rejected.

The findings align with recent studies that emphasize the critical role of Islamic finance in enhancing sustainability initiatives. For example, a study by Jan et al. [5] found similar impacts of Islamic finance on housing sustainability in Indonesia. However, our study advances this understanding by demonstrating that in Bangladesh, the specific practices of Islamic banks, such as their risk-sharing and asset-backed financing, directly influence the effectiveness of sustainable housing finance solutions. This comparative analysis not only corroborates the global relevance of Islamic financial principles but also highlights the unique regulatory and market dynamics in Bangladesh that might affect these outcomes.

The analysis confirms the hypothesized positive impact of Islamic banks on sustainable housing finance, underscoring the necessity for continuous improvement in banking practices and regulatory frameworks to fully exploit the potential of Islamic finance in promoting sustainability.

This study is groundbreaking in examining sustainable housing financing in the Chittagong division of Bangladesh and has important implications for improving green housing finance solutions. The study examines important elements that impact borrower satisfaction and demand fulfillment, providing guidance for Islamic financial institutions to improve their green financing solutions. The results have wide-ranging implications for the housing finance sector, guiding government, public, and private entities on developing policies and products to enhance the accessibility, affordability, and efficiency of sustainable home financing options in Bangladesh.

The implications of our study are profound, suggesting that policy interventions aimed at enhancing the regulatory framework for Islamic finance could further leverage its potential to support sustainable housing projects. Aligning with findings from Alam et al. [39], who discussed the potential of green sukuk in the Middle Eastern markets, our study suggests similar opportunities could be cultivated in Bangladesh through targeted policy reforms. These changes could encourage a more substantial investment in green infrastructure, potentially transforming the landscape of housing finance to better meet the sustainable development goals (SDGs).

This study emphasizes the involvement of Islamic banks in providing sustainable housing financing in Bangladesh, specifically examining borrower satisfaction in the Chittagong division within the sustainable finance housing sector. The research encountered difficulties such as respondent hesitation, budget and time restrictions, and a narrow emphasis on Islamic banking in Chittagong, while successfully fulfilling its objectives. Future study should expand to include different financial institutions and locations in order to have a thorough understanding of sustainable housing financing. Islamic banks should focus on improving service transparency, lowering costs, and diversifying green financing offerings to enhance accessibility and support sustainable housing objectives. Government initiatives might standardize profit rates and introduce more flexible collateral requirements to help poor and middle-income groups obtain sustainable home financing.

This study delves into the role of Islamic banks in fostering sustainable housing finance in Bangladesh, focusing on how borrowers perceive green financing options. Our findings demonstrate that Islamic banks are pivotal in supporting sustainable housing projects, significantly enhancing borrower satisfaction. The research carried out in the Chittagong Division underscores the profound positive impact of Islamic banking on sustainable home financing. It highlights how these banks are adapting their operations to align with both the environmental and financial preferences of their clients, emphasizing their integral role in the sustainable housing finance sector.

Through a comparative analysis with global and regional practices, this research illustrates how Islamic banks in Bangladesh uniquely contribute to the housing finance sector. Unlike broader international practices where diverse green financing methods like green sukuk are more prevalent, Bangladesh shows a focused commitment to sustainable housing finance. This commitment, while at an early stage compared to global standards, provides a crucial foundation for policymakers to formulate strategies aimed at amplifying the capacity of banks to support broader environmental and sustainable objectives. Our study suggests a significant potential for aligning Islamic banking practices with global sustainability standards, potentially propelling advancements in eco-friendly housing finance across Bangladesh.

Recognizing its limitations, this research sets a precedent for more in-depth studies into the impact of Islamic banking on sustainable housing financing. There is a need for comprehensive exploration across various sectors and financial institutions to deepen our understanding and facilitate ongoing discussions on how Islamic banking can promote sustainable housing options. Future research should focus on developing countries, examining the policy frameworks that can enhance the effectiveness of sustainable finance. These studies could offer new insights and strategies for integrating Islamic finance principles with sustainability goals in housing finance, thereby contributing to a holistic approach to environmental and economic sustainability.

The contributions of Islamic banks in Bangladesh to enhance sustainable home financing and increase borrower satisfaction are significant. This study emphasizes the necessity for ongoing research and policy development to fully leverage the potential of Islamic banking to meet the evolving demands of sustainable housing finance. Our findings lay a foundation for both academic and practical advancements, marking a pivotal moment for future research initiatives aimed at merging Islamic finance with sustainable housing projects.

No data were generated from the study.

SMS (Sardar Mohammed Shoaib), BKD and WS designed the study. SMS (Sardar Mohammed Shoaib) and SA collected data, and SMS (Sabrina Maria Sarkar) analyzed the data. SMS (Sardar Mohammed Shoaib), BKD, WS, SA and SMS (Sabrina Maria Sarkar) wrote the paper. BKD worked for proof reading.

The authors declare that there is no conflict of interest.

The authors acknowledge the use of various digital tools and software, including ChatGPT, for their roles in proofreading and refining the form during the preparation of this manuscript. Their utility in enhancing the clarity and readability of the text was notable.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

Shoaib SM, Dhar BK, Suengkamolpisut W, Ahmed S, Sarkar SM. Sustainable Housing Finance: Role of Islamic Banks in Bangladesh. J Sustain Res. 2024;6(2):e240020. https://doi.org/10.20900/jsr20240020

Copyright © 2024 Hapres Co., Ltd. Privacy Policy | Terms and Conditions