Location: Home >> Detail

J Sustain Res. 2025;7(2):e250024. https://doi.org/10.20900/jsr20250024

,

Vu Kien Phuc 2

,

Vu Kien Phuc 2

1 School of Accounting, University of Economics Ho Chi Minh City (UEH), 59C Nguyen Dinh Chieu Street, District 3, Ho Chi Minh City 700000, Vietnam.

2 School of Accounting, University of Economics Ho Chi Minh City (UEH), Vinh Long Campus, 1B Nguyen Trung Truc Street, Vinh Long 850000, Vietnam.

* Correspondence: Pham Quang Huy.

The objective of this investigation is to delve into the relationship between cybersecurity analytics (CSA) and twin transformation capabilities (TTC). This study specifically examines the role of smart climate change management accounting information system (SCCMAS) in mediating the relationship between CSA and TTC. It validates and establishes the correlation between CSA, SCCMAS, and TTC by a sequential exploratory approach that integrates qualitative in-depth interviews, literature review, and a quantitative survey of public sector organizations (PSOs). This study employs a mixed analytical strategy for data analysis, including structural equation modeling (SEM) and fuzzy-set qualitative comparative analysis (fsQCA), based on 739 valid survey responses. An examination of the results shows that CSA has a significant and positive effect on TTC. Moreover, it demonstrates that SCCMAS plays a part in partially mediating the relationship between CSA and TTC. The fsQCA findings additionally disclose causal linkages among the relevant elements. Hence, it is advisable for practitioners to embrace digital transformation, and use national policies, to enhance their organization’s utilization of digital technology in climate change management accounting practices. Furthermore, policy-makers and practitioners can utilize this study to improve their understanding of cybersecurity governance and to clarify strategies, processes, and management for the twin transformation in PSOs.

Building on the perspective of [1], sustainability is a critical concern due to the increasing worldwide demand. The worldwide quest for sustainability has intensified in recent years, indicating significant apprehension among the public, civic society, governments, and academics [1]. Organizations are confronting the issue of evolving into strategic and organizational frameworks that facilitate digital transformation and improve environmental sustainability. An increased emphasis is placed on digital transformation in the public sector organization (PSO) to ensure long-term relevance as well as the plans and missions of PSOs are progressively including sustainable development goals (SDGs) [2]. While sustainability and digitalization efforts were once considered separate pursuits, organizations are now acknowledging the complementary relationship between digital innovation and sustainability [3]. Based on the perspectives of [3], these two factors combine to enable mutually strengthening progress, significantly improving attainable environmental, social, and economic results. Recognizing that technology and sustainability goals are complimentary rather than mutually exclusive, twin transformation promotes an integrated approach that utilizes digital advances to further sustainability objectives and vice versa [4]. Twin transformation approaches facilitate the integration of technical and socio-economic dimensions inside PSOs by acknowledging the diverse stakeholders involved. Nevertheless, leading twin transformation is riddled with difficulties. Although the concept of twin transformation is conceptually persuasive, its implementation is not straightforward. Indeed, implementing transformations is a high-risk and time-consuming endeavor that frequently yields uncertain outcomes. Digital transformation continues to pose obstacles for organizations, leading to significant rates of failure. Moreover, sustainability transformation strives for long-term objectives, primarily non-economic in nature, which adds complexity to achieving successful sustainability transformation [5]. As noted by [6], numerous organizations are deficient in the necessary knowledge and direction to cultivate these crucial twin transformation capabilities (TTC). As such, organizations require dynamic capabilities to adapt their current business practices in order to effectively respond to fast changing market conditions and secure long-term growth and survival [7]. Differently put, in order to successfully achieve mastery in twin transformation, it is necessary to comprehend, cultivate, maintain, and consistently monitor the integrated dynamic capabilities. This will enable the evaluation of the progress of twin transformation and the exploitation of the mutual advantages of digital transformation and sustainability transformation inside the twin transformation [8]. This phenomenon has generated growing interest in the creation of integrated dynamic capabilities, specifically TTC: the individuals and resources required to fundamentally change growth trajectories.

Unfortunately, in light of the escalating public apprehension regarding global warming and climate change, these issues have become central to organizations’ considerations [9]. Global changes in climate policy have progressively necessitated organizations to adopt ecologically sustainable operations. In recent years, there has been a significant increase in the demand for accountability and transparency in the context of social and environmental issues [10]. A multiplicity of constituents is consistently pressuring PSOs to be more transparent in the reporting of environmental issues, driven by increased environmental awareness [11]. Nonetheless, the collection and analysis of climate change data can entail substantial expenditures and time-intensive processes, especially with the acquisition of real-time data from organizational systems, hence hindering effective climate change management. Accounting procedures have significantly contributed to tackling climate-related issues. Integrating climate change management accounting into standard accounting methods is essential to effectively mitigate the risks associated with environmental change. Technological innovations are transforming multiple sectors, including accounting. Thus, identifying efficient methods to leverage technology for assisting organizations in fulfilling contemporary demands helps mitigate environmental deterioration and promote more sustainable operational procedures. Against this backdrop, the deployment of smart climate change management accounting information system (SCCMAS) allows organizations to efficiently tackle the intricacy linked to the use of novel instruments and approaches. The SCCMAS is a system that utilizes artificial intelligence to strategically identify and target the activities and operations that are most susceptible to or make a significant contribution to carbon emissions. Furthermore, it facilitates the organization’s shift towards enhanced management and practices that are in line with the organizational growth and objectives. The effectiveness of a SCCMAS ensures that sustainable practices are not merely transient endeavors but are firmly embedded in the core concepts and operations of the organization. This integration finally results in the enhancement and refinement of the twin transformation.

More importantly, cyberattacks, malicious actions, and fraud in information systems have become ubiquitous global challenges, affecting organizations in a variety of regions and industries [12]. Cyberattacks are proliferating, rendering cybersecurity increasingly vital [13]. The imperative necessity for more sophisticated cybersecurity strategies is underscored by these threats, which threaten operational continuity, brand reputation, and competitiveness [14]. In the absence of effective cybersecurity awareness campaigns, incident management strategies, and adequate risk reduction, the cost of managing cyber risks in the event of an attack could be substantial [15]. Consequently, there is an urgent need for research on the most effective methods for establishing and sustaining secure cyber capabilities within organizations in developing countries. It is imperative for organizations to have a thorough and precise approach to data security and privacy, given the sensitive and confidential character of management accounting information. Cybersecurity analytics (CSA) refers to the application of analytical techniques and tools to analyze and interpret extensive amounts of data in order to identify and mitigate cybersecurity threats and hazards [16]. By doing this, the CSA allows PSOs to enhance and optimize the efficiency and effectiveness of SCCMAS, therefore improving the implementation of procedures and allocation of resources required for a fundamental and transformative shift in twin transformation. The technological facets of cybersecurity are its most recognized attributes; yet the cybersecurity phenomenon extends beyond only identifying technological effects and includes all elements of an organization [13].

Although the twin transformation is gaining increased attention, research in this field is disjointed and there is a conspicuous dearth of studies on the subject within the framework of PSOs. The occurrence of this phenomenon has required a reassessment and development of a comprehensive understanding of the evolving TTC in order to effectively use twin transformation inside the PSO. This disparity in comprehension regarding the effective implementation of twin transformation by PSOs is a critical area of research that is designed to provide PSOs with the requisite strategies to achieve success. It is imperative to investigate novel research questions regarding the factors that affect a PSO’s ability to conduct twin transformation in this endeavor. The objective of this study is to address the dearth of academic work regarding the potential influence of CSA on enhancing TTC. Its primary objective is to investigate how CSA may improve the TTC by means of a SCCMAS. The investigation underlines the possibility of achieving both theoretical and practical progress in this field. Moreover, this theoretical gap gives rise to the following research questions.

RQ1. Does CSA illustrate an impact on TTC?

RQ2. Does SCCMAS mediate the relationship between CSA and TTC?

Based on the analysis of the overall results and chief observations, this study offers contributions both for academician and practitioner communities through bridging many voids. This manuscript is novel as it specifically aims to enhance the existing knowledge on twin transformation in PSOs in developing countries, focusing special attention on TTC. There is an increasing consensus that the current challenges, including the technological revolution and climate change, necessitate a systemic transition to a more digital and environmentally friendly economy [17]. Digital transformation is not limited to the private sector; thus, it is essential to examine it within the public sector setting as well [18]. Since the 1950s, the PSO has undergone transformation through the use of digital technologies, beginning with mainframes, followed by personal computers in the 1980s and 1990s, and culminating in the extensive utilization of the Internet [19]. Nonetheless, the transformation of the PSO has progressed slowly and remains inferior to that of the private sector [18]. This is due to the stability requirements of the PSO [20]. PSO has substantial effects on environmental, social, and economic matters that require effective management [21]. PSOs are crucial in attaining the SDGs due to their profound understanding of community needs and their strategic placement at the forefront of sustainable development efforts [10]. Hence, it is imperative to regard it as a proactive participant in the economic system, engaging in the acquisition, consumption, administration, and disposal of a significant quantity of resources. An extra role of the PSO proposed by authors for twin transformation is its significance as a role model, whereby it should serve as an exemplar of beneficial practices. The public sector exerts control over all other sectors, including the formulation of policies and regulations, and the establishment of the overall direction for the practical implementation of the transition by organizations. Hence, considering the importance and capacity of the public sector in carrying out twin transformation, it is crucial for the PSO to adopt twin transformation principles in their resource management at the organizational level. The emerging generation of digital technologies is essential for fostering a more equitable society and economy in the forthcoming decade, enabling both citizens and organizations in the digital era [22]. Notwithstanding comprehensive studies on digitalization and sustainability, a significant gap persists in comprehending how these two transformational forces might be synergistically utilized within specific domains [4]. Moreover, the technological facets of cybersecurity are its most recognized attributes; yet the cybersecurity phenomenon extends beyond only identifying technology effects and includes all elements of an organization [13]. This study was a sequential exploratory mixed-methods investigation, undertaken in two phases: one qualitative and one quantitative [23]. Mixed methods research incorporates both qualitative and quantitative data gathering and analysis techniques within a single study [24]. The process commenced with a qualitative study to obtain interpretive insights, which established the foundation for the ensuing quantitative phase. This methodology enhances the value of management research by providing the potential to obtain additional information about processes and outcomes [24]. This progressive methodology, wherein each phase informs and improves the subsequent one, guarantees that our findings are solid and realistically pertinent for augmenting the effectiveness of CSA and SCCMAS to achieve the elevated TTC. This research elucidates the elements influencing TTC in this area by a combined analysis of partial least squares structural equation modeling (PLS-SEM) and fuzzy-set qualitative comparative analysis (fsQCA).

Furthermore, the results may motivate researchers to conceive novel concepts that address the increasing need for TTC. Utilizing the insights derived from this study, they can develop sustainable and socially responsible solutions to meet this urgent demand. The findings of this study also extend the existing body of knowledge on twin transformation by showcasing the capacity of CSA to augment the process of twin transformation. Given that conventional defense mechanisms are increasingly insufficient for tackling the complex risks that organizations encounter today [25], this study offers a comprehensive approach to cybersecurity that empowers organizations to prevent and respond to cyber threats as cybercriminal strategies evolve with technological progress. This study clearly delineates essential components of CSA that function as core parts, bolstering and supporting cybersecurity. Consequently, the findings of this study enhance the current body of literature about cybersecurity in the setting of PSOs in developing nations. Moreover, the main originality and significance arises from offering a thorough viewpoint on the mediating function of a SCCMAS in the correlation between CSA and TTC. More importantly, our findings indicate that CSA alone do not substantially improve TTC; however, its combination with SCCMAS does. The mediating effect of SCCMAS highlights its crucial significance in utilizing the integration of digital technology into climate change management accounting information system to enhance TTC.

The study of [26] emphasizes the swift progression of climate change and accounting literature, reflecting the increasing urgency and apprehensions regarding climate change matters. The swift rate and increasing intensity of climate change effects have shown that existing progress-oriented strategies to urgent global socio-ecological issues are inadequate in tackling the fundamental reasons of unsustainable growth [27]. The growing imperative for organizations to engage in accounting and reporting specifically focused on climate is underscored, with the objective of enhancing awareness of the climate catastrophe [28]. Climate change management accounting plays a crucial role in facilitating sustainable strategic and operational decisions about climate change management. With the support of digital technology, SCCMAS provides tools and procedures that enable organizations to comprehend the magnitude of the issue, develop viable solutions, and assure the proper implementation of these solutions for effective climate change management.

From a practical perspective, the results of this paper provide useful information for practitioners to comprehend the extent of sustainable innovation and the requirement of focusing on formulating and developing twin transformation technologies. By providing persuasive evidence on the understanding of CSA and its impact on TTC in PSO, practitioners can use the knowledge gained from this investigation to position themselves as leaders in the practical application of CSA and SCCMAS. This study has also furnished policymakers with insights to help them formulate and implement regulations and policies regarding the twin transformation in PSOs. The current investigation is organized as follows. In Section 2 (LITERATURE REVIEW), a concise overview of the conceptual elements and their theoretical foundation are provided. The third section of the research paper offers the formulation of research hypotheses and the construction of a research model. Section 4 (MATERIALS AND METHODS) provides a detailed overview of research methodology. The findings derived from the study as well as implications on theory and practice are described in Section 5 (INFERENTIAL STATISTICS). The manuscript’s sixth section (CONCLUSION) provides a conclusion as well as valuable suggestions for future studies.

The theory is an expansion of the resource-based view [29], which posits that the reasons for performance differences among organizations are ascribed to their competitive advantages derived from resources that possess the qualities of uniqueness, value, inimitability, reproducibility, and irreplaceability [30]. In recent years, sustainability has gained significant importance in organizational strategy due to the growing awareness of the effects of contemporary consumer behavior and industrialization on climate change [31]. In order to attain sustainability, organizations must adapt and address the varied demands of customers and create their products or services, accordingly, necessitating the possession of dynamic capabilities [32]. The exponential expansion of information technology in organizational operations enables organizations to adapt and transform their dynamic capabilities to achieve sustainability [33]. In their study, [6] utilize dynamic capabilities theory to develop capabilities that optimize the combined potential of digital transformation and sustainability transformation. This approach has the potential to improve organizational performance and generate new value for collective welfare.

Stakeholder theoryOne commonly accepted definition of a stakeholder is any entity or person that has the ability to exert influence on, or be affected by, the accomplishments of an organization [34]. Based on the perspectives of [35], stakeholder theory is a theoretical framework encompassing principles of corporate ethics and organizational management. The fundamental premise is that proper management of stakeholder interactions is very probable to result in successful performance [36]. Although the theory is primarily focused on private-sector institutions, several studies also extend its application to PSOs due to the similarity in managerial roles between the two sectors [36]. Stakeholder theory offers a conceptual structure for comprehending the wider social, environmental, and economic impacts of operational activities in organization [37]. The stakeholders of PSOs are also significant participants in the digital ecosystem to which they are affiliated. With the advent of digital technology, key stakeholders have gained more authority to exert influence on organizations, either directly or indirectly, to advocate for digitalization [38] and achieve sustainability transformation. Hence, stakeholder theory can elucidate the reasons behind the implementation of twin transformation in PSOs.

Conceptual Framework Cybersecurity analyticsSecurity analytics refers to a proactive strategy in cybersecurity that utilizes data gathering, aggregation, and analytical skills to carry out essential security tasks such as identifying, examining, and reducing cyber risks. The concept of CSA has gained attention in the corporate analytics and information security management literature [39]. However, there is still a lack of comprehensive knowledge regarding the fundamental aspects of CSA capabilities [39]. Given that the notion of CSA is at an early stage of development and requires further research [38].

Building on the perspectives of [40], CSA is a proactive strategy in which organizations proactively plan to confront cyberthreats by monitoring and correlating real-time events that may entail harmful activity, rather than waiting for cyberattacks to occur. As such, this methodology depends on Machine Learning algorithms to effectively manage large volumes of data to guarantee comprehensive security of information technology systems and networks [40]. One of the most favored protection mechanisms among systems developed by training Machine Learning algorithms on a pre-collected dataset is the Network Intrusion Detection System [40]. Enhancing the effectiveness of a Network Intrusion Detection System during the initial development phase may be achieved by considering many aspects [40]. Selecting a current and high-quality dataset for training the models, together with rigorous preprocessing of the dataset, are crucial factors for achieving success in constructing machine learning models for intrusion detection [40].

Smart climate change management accounting information systemResearch on climate change in relation to SDG 13 has mostly concentrated on the accounting and reporting of carbon and greenhouse gases [41]. By assessing vulnerability and adaptive capacity, valuing adaptation costs and benefits, and disclosing the risks associated with climate change impacts, [42] proposed that accounting can facilitate organizational climate change adaptation. The study conducted by [43] demonstrated the impact of implementing and distributing carbon accounting tools within a public organization on the behavior of companies. The research conducted by [44] documented the emergence of carbon reduction, energy efficiency, and greenhouse gas emission reduction initiatives among high-polluting firms. The study by [45] investigates the methodologies and tactics employed by airline businesses in the realm of carbon accounting and mitigating their impact on global warming.

The concept of climate change accounting lacks a precise and definitive definition. According to [36], carbon accounting alone addresses carbon emissions, but climate change accounting also includes additional greenhouse gas emissions reductions. [37] defines climate change accounting as the integration of emission accounting, greenhouse gas emissions footprint, carbon capture and storage, and sequestration projections. This study by [38] provides a more comprehensive analysis of the responsibilities of management accountants in relation to climate change. Management accounting is crucial in the formulation of company-level strategy and risk management and can significantly facilitate society endeavors to address climate change [46]. Although initially designed and used in the accounting profession [47], the management accounting system has been extended to various domains owing to its usefulness and advantages. The application of a management accounting system involves compilation and integration of data, producing an informative summary for managers to use in their policy evaluation and decision-making processes [48].

Healthcare sector managers have integrated management accounting systems to enhance the quality of their service offering and delivery [49]. The application of management accounting system in political resource analysis facilitates the identification of change requirements, the acquisition of support for change, and the implementation of change within organization [50]. In essence, the management accounting system extends beyond the realm of accounting and has gained recognition in several sectors of contemporary company and commercial operations [51]. In this research, climate change management accounting practices are considered as a dynamic procedure that encompasses the identification, extraction, classification, consolidation, and presentation of climate change data with the support of artificial intelligence. More precisely, the SCCMAS can be understood as a system with the support of artificial intelligence, strategically developed and implemented to not only ascertain the pertinent information but also to pinpoint the activities and operations that are most vulnerable or significantly contribute to carbon emissions. It also enables the organization to transition towards improved management and practices that align with organizational development and business strategies.

Twin transformationAccording to [52], since the 1990s, the inquiry of the role of digitalization in the ecological transition has been repeatedly posed, however no definitive conclusion has been established. The preliminary connection between digitalization and sustainability may arise from the application of the economic principle of dematerialization to the developing notion of the information society [52]. Digital transformation and sustainability transformation are the primary driving drivers behind change [53]. Digital transformation is a prevalent phenomenon within organizations, characterized by the fundamental transformation of their business models by innovative digital technologies [54]. In the meanwhile, sustainability transformation entails a fundamental shift in organizational processes towards total sustainability, including environmental, social, and economic aspects [55]. This transformation serves as the basis for future resilience [56]. Twin transformation refers to the synergistic interaction between digital transformation and sustainability transformation initiatives, where an organization enhances its operations by using digital technologies to promote sustainability and utilize sustainability to drive digital advancement [6].

The twin transformation technique combines the issue spaces of digital transformation and sustainability transformation, resulting in a composite solution space at their interface. The different transformations provide distinct problems inside these problem spaces, which are then handled in an integrated manner within the twin transformation solution space. Rapid developments in digital technology have propelled digital transformation, resulting in significant effects on individuals, organizations, and society (e.g., [57,58]). The progress of emerging digital technologies, including digital platforms and artificial intelligence, is enhancing the capacity to gather and analyze increasingly bigger amounts of data, construct forecasts using that data, and produce solutions. Contemporary research on digital transformation mostly concentrates on the examination of how technological advancements alter the routes of value creation and the associated positive and negative effects at various levels of analysis [57,59]. Concurrently, market dynamics are influenced by worries over environmental degradation, social inequality, and economic instability, which have also intensified debates on digital sustainability and digital resilience [56,60]. Digital technology, particularly artificial intelligence-enabled systems, have a crucial role in solving environmental and societal issues to promote the creation of new solutions and systemic changes, hence facilitating sustainability transformation [61]. Technology, despite its numerous benefits, can also perpetuate harassment, violence, and dishonor by incentivizing hackers to specifically attack computer systems [62]. The dual nature of technological advancements give rise to concerns pertaining to cybersecurity and personal security [63].

The advancement and growth of natural language processing models and large language models exhibit human-like attributes in problem-solving, perception, focus, and innovation, enabling humans to overcome operational obstacles [64]. Furthermore, the vast potential of artificial intelligence has concurrently augmented the cyber-attack skills of hackers and the defensive and security capabilities of network managers to a great extent [64]. The field of cybersecurity encompasses the study of cyber attackers and their range of cybercriminal attacks [65]. Cybersecurity refers to the implementation of methods aimed at safeguarding computers and networks from unauthorized access and hostile actions, including instances of data theft and destruction [66]. The integration of cybersecurity and analytics facilitates enhanced network visibility [67]. The implementation of CSA is the use of analytical methods and tools to examine and interpret large volumes of data for the purpose of detecting and addressing cybersecurity threats and risks [16]. In doing so, the CSA enables PSOs to improve and enhance the efficiency and effectiveness of twin transformation. Building upon the previously considered grounds, the hypothesis in this study is postulated as follows.

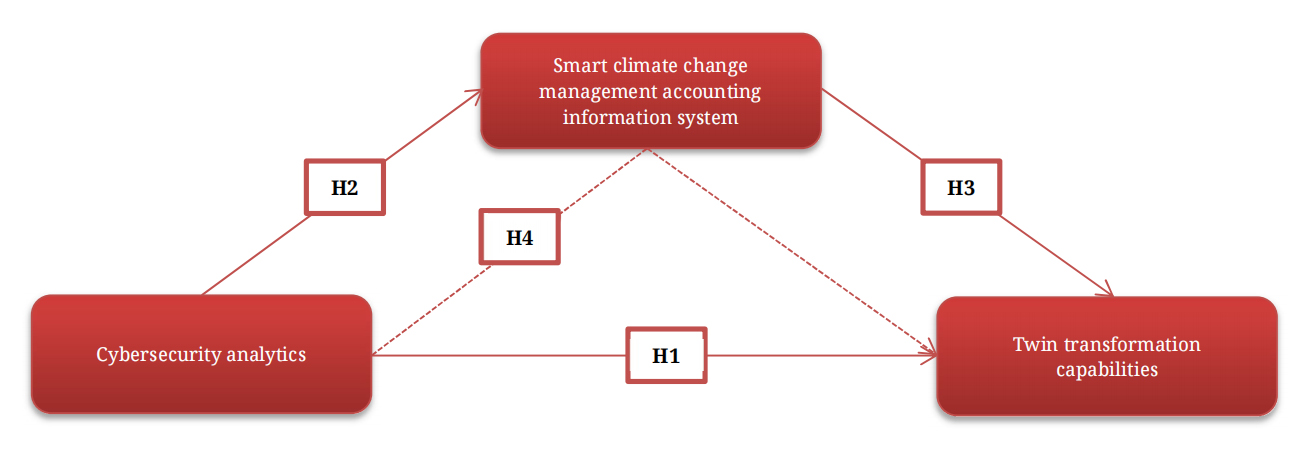

Hypothesis 1 (H1). CSA is likely to affect TTC in a significant and positive manner.

Given the crucial role that data plays in the success of any organization, safeguarding and ensuring the security of such data has become a paramount concern in the current era of the fourth industrial revolution [68]. Expanding upon the viewpoint of [69], a cyberattack can target financial, personal, contact, intellectual property, data related to an organization’s information technology infrastructure, data related to clients, and other categories of sensitive information. This further demonstrates the indispensability of cybersecurity in maintaining the security, robustness, and efficiency of information systems. Data and information security is of paramount significance in the face of assaults [69]. Cyber security refers to the protocols and procedures implemented to avoid unwanted access to, or exposure of confidential data held in digital format [70]. The objective is to prevent unauthorized access, utilization, and abuse of electronic information in a systematic and structured manner. In order to maintain the proper functioning of the systems and information contained within them, as well as to protect personal information, suitable security measures and procedures are implemented. It is well recognized that cybersecurity plays a crucial role in accounting information and systems [71]. Organizations must have a meticulous and comprehensive strategy to data security and privacy due to the sensitive and confidential nature of management accounting information. The implementation of CSA is the use of analytical methods and tools to examine and interpret large volumes of data for the purpose of detecting and addressing cybersecurity threats and risks [16]. In doing so, the CSA enables PSOs to improve and enhance the efficiency and effectiveness of SCCMAS. Building upon the previously considered grounds, the hypothesis in this study is postulated as follows.

Hypothesis 2 (H2). CSA is likely to affect SCCMAS in a significant and positive manner.

Climate change is a multifaceted phenomenon that affects several aspects of the ecological, environmental, socio-political, and socio-economic fields on a worldwide scale [72]. External uncertainty resulting from climate change might undermine the sustainability investment and environment, social, and governance performance of organizations, therefore impacting their sustainable development [73]. Effective execution of planning and policy tools is crucial for achieving success in climate change adaptation [74]. In their study, [75] investigate the potential of enhancing the advancement of the 17 UN SDGs through the utilization of emerging technologies such the internet of things, big data analytics, and artificial intelligence. In the meanwhile, advanced artificial intelligence algorithms and machine learning methods have the capability to analyze extensive climate data, improve weather prediction, and facilitate well-informed decision-making in plans for adapting to and mitigating climate change [76]. Building on the standpoints of [77], there is a need for further investigation into the interplay of digital sustainability, climate change, and information systems solutions.

Artificial intelligence holds great promise for enhancing management accounting information systems. Additionally, [78] delves into the integration of artificial intelligence technology in management accounting information system. Indeed, this integration radically changes the role played by management accountants, reducing routine tasks and enhancing their strategic role in the organization [79].

Twin transformation frequently entails the adoption of novel technologies and the implementation of creative procedures. With the support of artificial intelligence, the techniques of climate change management accounting prioritize the establishment of quantifiable objectives and the ongoing monitoring of operations. This is consistent with sustainability initiatives, which necessitate monitoring and reporting on environmental and social performance. Climate change management accounting is a developing field that improves openness and accountability in accounting and reporting procedures related to climate change. It delivers precise and dependable data by systematic measurement, analysis, and reporting of climate change and associated organizational expenses. The implementation of a SCCMAS enables organizations to effectively address the complexity associated with adopting new tools and methodologies. The effectiveness of SCCMAS guarantees that sustainable practices are not only temporary initiatives but are deeply ingrained in the fundamental principles and activities of the organization. This integration ultimately leads to the improvement and enhancement of TTC. Building upon the previously considered grounds, the hypothesis in this study is postulated as follows.

Hypothesis 3 (H3). SCCMAS is likely to affect TTC in a significant and positive manner.

Climate change transcends borders [80]. The diverse economic implications of climate change can impact organizations in numerous ways and may compel them to adapt to evolving circumstances. Climate change and the imperative of reducing carbon emissions have ascended on the priorities of global policymakers [81]. A study by [82] investigated the prevailing trend of digitalization aimed at enhancing environmental sustainability. The researchers examined nine cases across different countries utilizing emerging technology to tackle climate change adaptation. They claimed that digital transformation could mitigate the effects of climate change in urban areas. Recently, PSO has experienced significant responses to climate change, with stakeholders exerting more pressure to formulate operational strategies and efficiently deploy resources to mitigate negative externalities. SCCMAS is a system augmented by artificial intelligence, designed and executed to identify relevant information and to detect activities and processes that are most susceptible or substantially contribute to carbon emissions. It facilitates the organizations’ shift towards enhanced management and practices that correspond with organizational development and business strategy.

The digital transformation of organizations is a prevailing trend in the global economy; yet, cybersecurity represents a fundamental tension that must be addressed [83]. Cybersecurity concerns can affect the confidentiality, integrity, and availability of data related to twin transformation, as well as the safety and reliability of all systems represented by this transformation. Climate change poses a direct threat to organizational operations, as cyberattacks compromise equipment installations, communication networks, and supply chain management. These disruptions undermine operational readiness and expose sensitive data across all systems to potential cyber threats. Organizations can enhance their preparedness for potential environmental implications of cybersecurity by ensuring collaboration between all the departments of the organization to incorporate climate change concerns into security strategies. Consequently, it is imperative to consider the design of smart cybersecurity systems that address contemporary requirements. Cybersecurity encompasses many procedures and technologies that guarantee the confidentiality, integrity, and availability of data while protecting digital assets [84]. To address contemporary cyber dangers, industries and organizations must adopt a more proactive and predictive strategy, attainable through the utilization of CSA. This entails the implementation of suitable cybersecurity measures, processes, and technology to protect the organization from potential cyber risks, including unauthorized access, data breaches, and other criminal activities. Building upon the previously considered grounds, the hypothesis in this study is postulated as follows.

Hypothesis 4 (H4). SCCMAS is likely to mediate the relationship between CSA and TTC.

Therefore, all the aforementioned hypotheses and variables were illustrated in Figure 1 as shown below:

Figure 1. Hypothesized model.

Figure 1. Hypothesized model.

In line with the perspectives of [85], the current study employed a sequential mixed methods design to achieve the study’s objectives. It adhered to a pragmatist tradition that emphasized the utility of knowledge rather than a ‘pure’ paradigmatic approach [86]. A mixed-methods research design was a systematic approach for gathering, analyzing, and integrating both quantitative and qualitative methodologies within a single study or a series of studies to comprehend a research issue. Connecting qualitative and quantitative data was essential for hypothesis creation and construct selection, as well as for result interpretation. Consequently, the amalgamation of diverse research methodologies mitigates the issue of generalizability in qualitative studies and addresses the deficiency of comprehensive contextual data in quantitative research [87].

This study was a sequential exploratory mixed-methods investigation, undertaken in two phases: one qualitative and one quantitative [23]. The process commenced with a qualitative study to obtain interpretive insights, which established the foundation for the ensuing quantitative phase. This progressive methodology, wherein each phase informed and improved the subsequent one, guaranteed that our findings were solid and realistically pertinent for augmenting the effectiveness of CSA and SCCMAS to achieve the elevated TTC. Initially, the qualitative portion of this study was conducted to explore possible areas for enhancing TTC from the perspectives of PSOs. The survey facilitated the generalization of the qualitatively validated findings regarding areas that needed development. Responses were generated by the examination of both qualitative and quantitative data sets to help PSOs enhance the TTC.

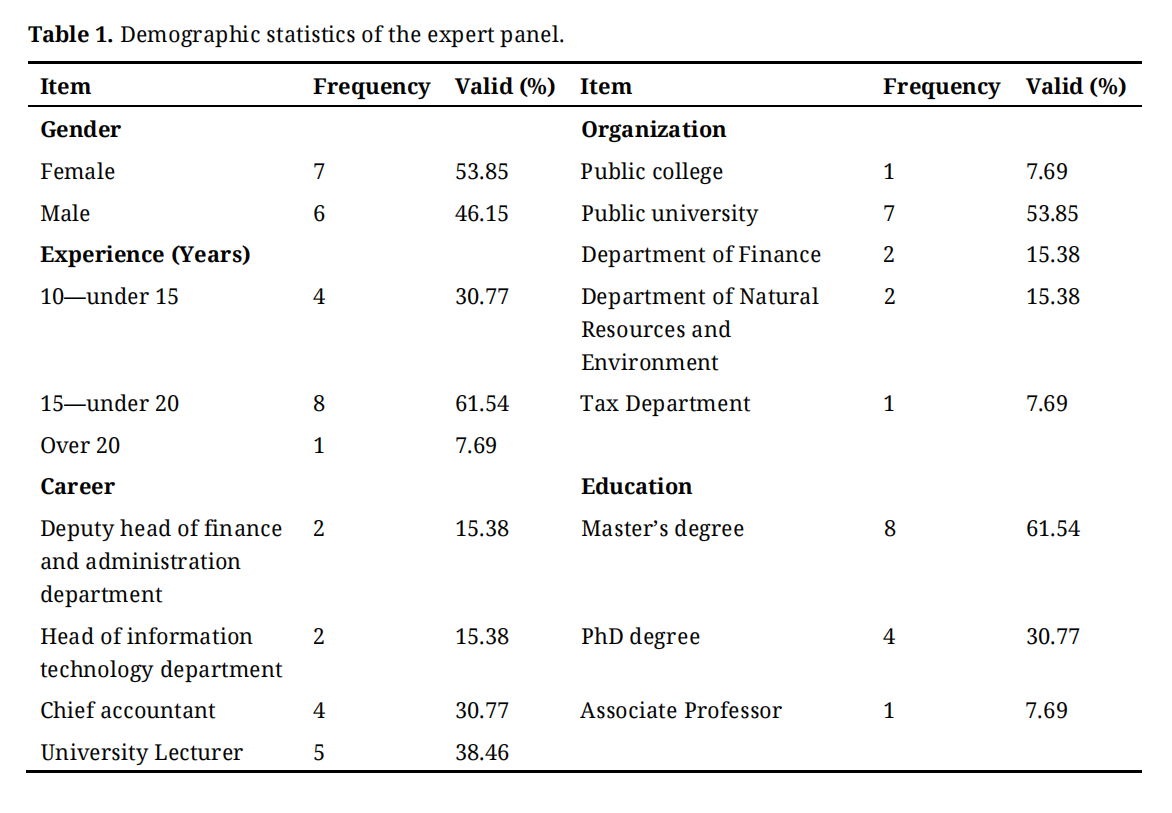

Qualitative Research MethodIn Phase 1, to ensure rigor in this study, we employed a qualitative method to collect the opinions and perspectives of participants from PSOs. This was conducted to ascertain the relationships between CSA, SCCMAS, and TTC. We utilized thematic analysis [88] to analyze the qualitative data, exploring interviewees’ perspectives on CSA, SCCMAS, and TTC, while also identifying the interconnections between these elements. In the initial phase, we conducted comprehensive interviews utilizing a semi-structured format, employing an interview guide to direct the participants, with each respondent receiving identical questions in the prescribed sequence (see to Appendix).

The research targeted lecturers in public colleges and public universities, the chief accountants, the head of finance and administration department, and the head of information technology department in PSOs in Vietnam. Data collection included non-probability sampling by purposive approach. The sample size utilized relatively small samples due to its in-depth nature; we continued sampling until no new insights emerged regarding these parameters, resulting in information saturation [89]. The interviews culminated in a saturation point with 13 participants, comprising 5 conducted at the interviewees’ offices and 8 via online platforms, including telephone calls and the Zalo app, lasting between 45 minutes and 60 minutes. The interviews were carried out from September 2023 to December 2023, with comprehensive notes taken for each session. The demographic statistics of the expert panel were presented in Table 1.

Table 1. Demographic statistics of the expert panel.

Table 1. Demographic statistics of the expert panel.

Subsequently, we analyzed the qualitative data derived from 13 in-depth interviews, coding them by emphasizing recurring words, phrases, and sentences. We examined the generated codes to formulate themes and discern patterns among them [90], followed by a review of the themes to identify any omissions or modifications, and subsequently applied these themes to the data itself. Finally, the findings were written up [91].

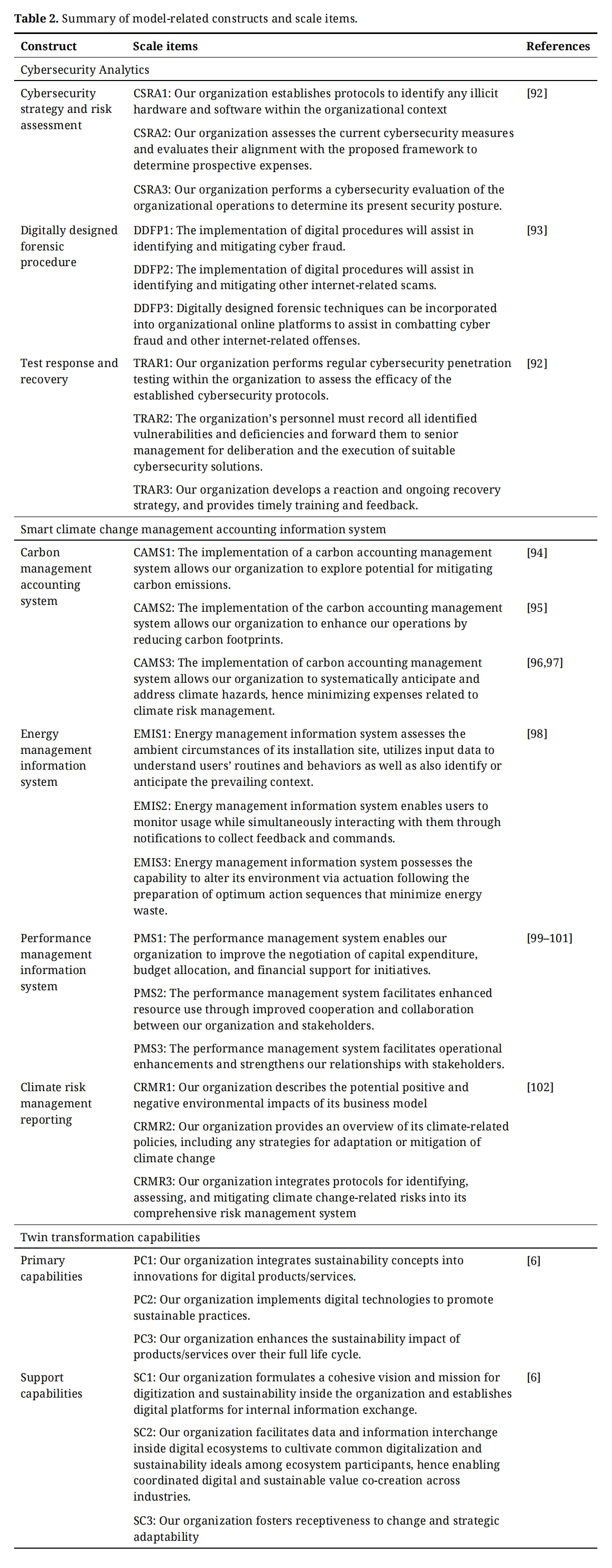

Quantitative Research MethodIn order to accomplish the objectives of the study, an extensive literature analysis was carried out to determine the research constructions. Subsequently, multiple items from each construct were identified to design the preliminary questionnaire. The survey was composed in the English language and verified by linguists to ensure its precision, acceptability, and interpretability. The survey questionnaire was translated from English to Vietnamese by multilingual experts. These experts then reverse-translated the survey questionnaire. The two English questionnaires were subsequently compared to verify the consistency of the survey items. The survey used in the research underwent content and face validity assessments. Prior to data collection, a pilot test was carried out on 50 respondents to verify that the research participants did not encounter any problems with the wording, design, or format of the questionnaire. The reliability of the instrument was assessed using Cronbach’s coefficients, which indicated the internal consistency of the items used to formulate scales. The results of the internal consistency reliability testing established that the Cronbach’s alpha value surpassed the threshold of 0.7, therefore confirming that the questionnaire had accurate and coherent items. The results of the pilot testing indicated that the items met the criteria for establishing reliability, and all of the items were kept for additional analysis. The summary of constructs with corresponding scale items was demonstrated in Table 2. All items were evaluated using a 7-point Likert scale, with anchors ranging from 1: strongly disagree to 7: strongly agree.

Table 2. Summary of model-related constructs and scale items.

Table 2. Summary of model-related constructs and scale items.

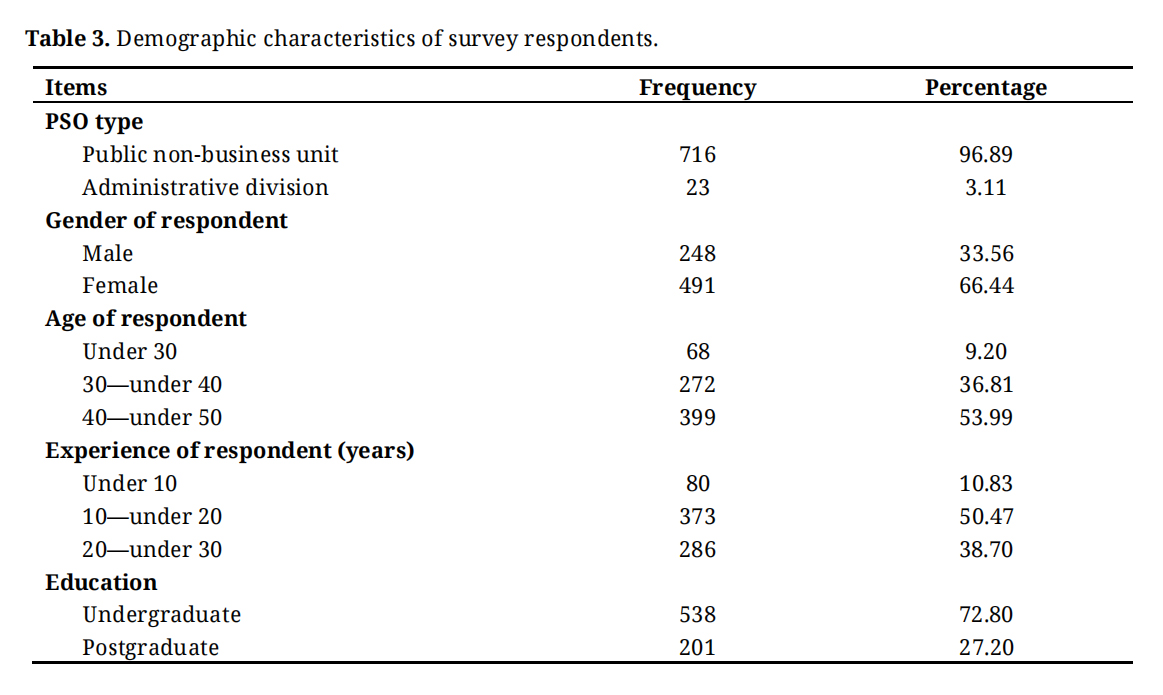

Two sample units were employed to acquire the primary data for this investigation. The secondary sampling unit was organizational accountant, while the primary sample unit was organization. The current investigation concentrates on Vietnamese PSOs. The accountants were accountable for the organization’s strategic planning and the implementation of control mechanisms. The convenience sampling and snowball sampling approaches were employed to generate the sample for this study, as a result of the investigation’s temporal and financial constraints. Convenience sampling was the primary method of non-probability sampling, focusing on obtaining data from participants who are easily accessible to the researcher. Snowball sampling was a non-probability sampling approach wherein existing subjects actively recruit more subjects for inclusion in the sample. This method enabled engagement with individuals who were hitherto unreachable, thereby providing access to those who were previously unidentified. The target audience was initially reached via convenience sampling. These individuals could provide researchers with access to a far bigger pool of potential subjects who meet the study’s criteria. The researchers sought authorization from the senior management of the relevant organizations to get the accountants’ contact information prior to inviting them to partake in the study.

Prior to distributing the surveys to respondents in person, the researchers secured their informed consent. This would diminish the probability of participants providing erroneous responses to surveys, and allow researchers to guarantee the confidentiality and anonymity of the study’s conclusions. Participation in the study was voluntary, and individuals were guaranteed confidentiality and anonymity. They may withdraw at any moment and for any rationale. The study primarily focused on the accounting personnel of PSOs in Vietnam. To determine eligibility, the following criteria were established: (i) Participants must be presently employed in PSOs; (ii) They must possess a minimum of six years of professional experience; (iii) They must have knowledge of climate change; (iv) They must have knowledge of cybersecurity; (v) They must have knowledge of twin transformation; (vi) They must be willing to engage in the research. Participants recruited for the study who failed to meet the qualifying requirements were excluded. This sample size also satisfied the “10 times rule” approach, which was a commonly used method for estimating the minimum sample size in PLS-SEM. This method was based on the assumption that the sample size should be at least 10 times larger than the maximum number of connections between latent variables in the inner or outer model [103].

Data was collected from the beginning of April 2024 to the beginning of September 2024. After screening and examining the questionnaires, a final sample size of 739 valid responses with a data loss rate of 14.50 percent. Given that PLS-SEM was based on regression methodologies, it was constrained by restrictions including causal symmetry and net effects. To mitigate these constraints and enhance comprehension of the data, the study additionally utilized fsQCA, an asymmetric methodology [104]. The fsQCA facilitated the simultaneous evaluation of several causal configurations [105]. PLS-SEM findings were augmented by fsQCA, which investigated the combinations of causal factors (independent variables) that resulted in identical outcomes (dependent variable) [106]. As such, to improved the predicted accuracy of our study, we employed a comprehensive data analysis strategy that integrated both linear (PLS-SEM) and non-linear (fsQCA) methodologies. This strategy was acknowledged for its capacity to enhance the accuracy of results [107]. The model fit indices were assessed in this research using covariance-based structural equation modeling with the support of AMOS version 28. The SmartPLS version 4.1.0.8 was utilized for PLS-SEM analysis, whereas fsQCA version 4 were employed for fsQCA analysis, respectively. Table 3 showed a thorough description of the demographic data collected from the survey.

Table 3. Demographic characteristics of survey respondents.

Table 3. Demographic characteristics of survey respondents.

We disseminated a research information cover letter that provided an overview of the instructions for participation, emphasized the voluntary nature of involvement, ensured the anonymity of participants, clarified that the data would be utilized solely for the purposes of academic research, and reaffirmed the participants’ right to withdraw from the study at any time in the event that they encountered any discomfort. Furthermore, in order to conceal the identification of any particular construct and reduce the likelihood of response patterns, we randomized the sequence in which the questionnaire items were presented. The Harman one-factor test was employed and discovered that the first factor explained around 20.641% of the variance, which was below the 50% criterion. The guideline of [108] was also employed in this research. The variance inflation factor scores, which ranged from 1.558 to 2.609, were lower than the recommended cutoff of 3.3. According to [108], these values highlighted that common method bias did not pose any substantial problems in the sample. In the nutshell, there was no apparent presence of common method bias in our study.

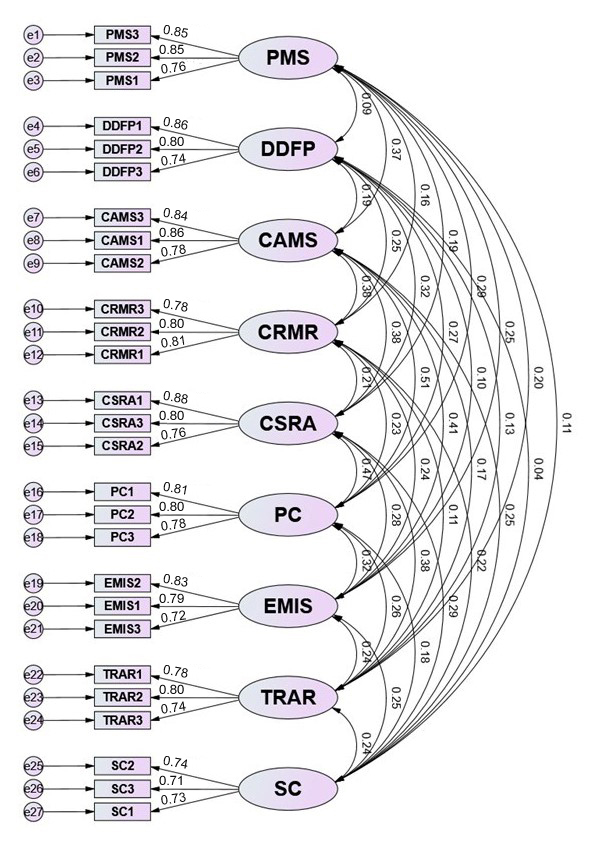

Confirmation Factor AnalysisThe results of CFA in Figure 2 confirmed that the measurement of this research perfectly suited the gathered data as all of the indices’ values met the threshold suggested by [109]. More concretely, Chi-square/df = 1.414; TLI = 0.984; CFI = 0.987; GFI = 0.961; RMSEA = 0.024.

Figure 2. CFA result. Note: Chi-square/df = 1.414; Chi-square = 407.256; RMSEA = 0.024; GFI = 0.961; TLI = 0.984; CFI = 0.987; df = 288; p = 0.000.

Figure 2. CFA result. Note: Chi-square/df = 1.414; Chi-square = 407.256; RMSEA = 0.024; GFI = 0.961; TLI = 0.984; CFI = 0.987; df = 288; p = 0.000.

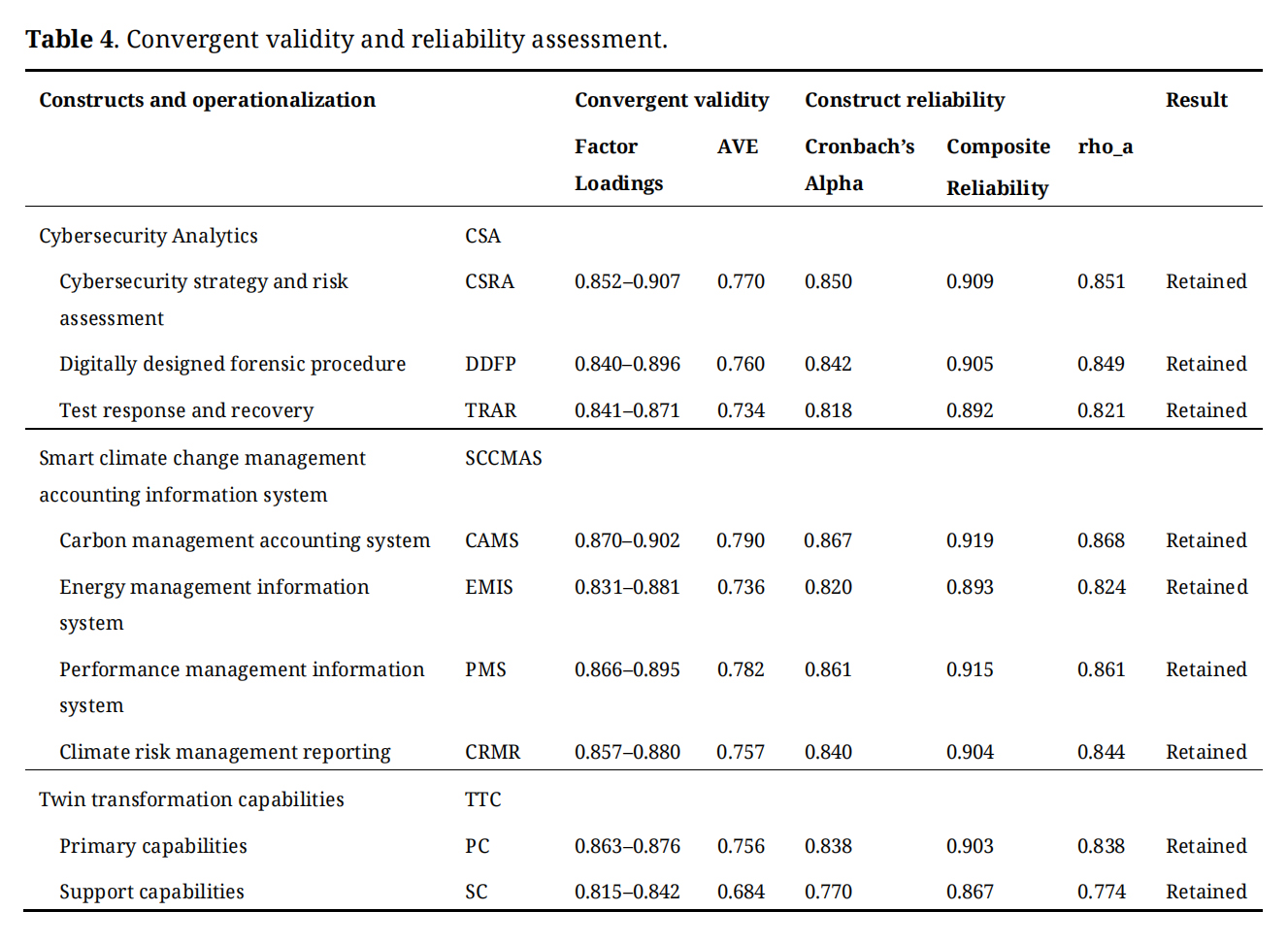

In accordance with the recommendations of [110], we evaluated the psychometric characteristics of all measuring scales by examining their indicator reliability, construct reliability, and validity. The evaluation entailed the examination of explicit statistical tests [110]. Initial assessment of the indicator’s reliability was conducted by examining the factor loadings of each item. The validity assessment in this work analyzed the results of outer loading, which should surpass a threshold of 0.7 [111]. Furthermore, we assessed the internal consistency reliability of each construct by employing Cronbach’s alpha (α) and Composite Reliability (CR). In this situation, it was imperative that both the Cronbach’s alpha and CR above the threshold of 0.7 [110]. Furthermore, the Dijkstra-Hensele’s rho evaluation was used at this step. The Dijkstra-Hensele’s rho value should exceed 0.7, indicating reliable internal consistency of the framework [112]. Furthermore, this study utilized a validity test that evaluated the average variance extracted (AVE) values, which ought to be greater than 0.5 [113]. The obtained findings in Table 4 revealed that the proposed framework met the requirements of reliability and convergent validity.

Table 4. Convergent validity and reliability assessment.

Table 4. Convergent validity and reliability assessment.

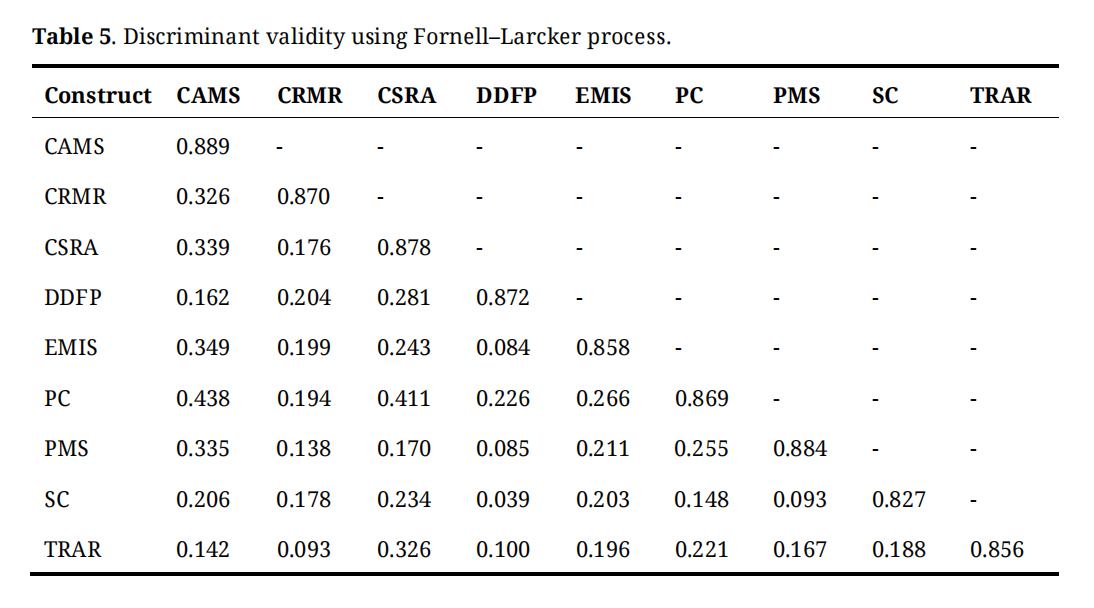

To assess the discriminant validity, the Fornell Larcker criteria [114] and the heterotrait-monotrait ratio (HTMT) [115] were employed. The Fornell Larcker criterion yielded results that satisfied the threshold value for all constructs. Table 5 indicated that AVE square root of each latent variable exceeded the highest coefficients of any other variables.

Table 5. Discriminant validity using Fornell–Larcker process.

Table 5. Discriminant validity using Fornell–Larcker process.

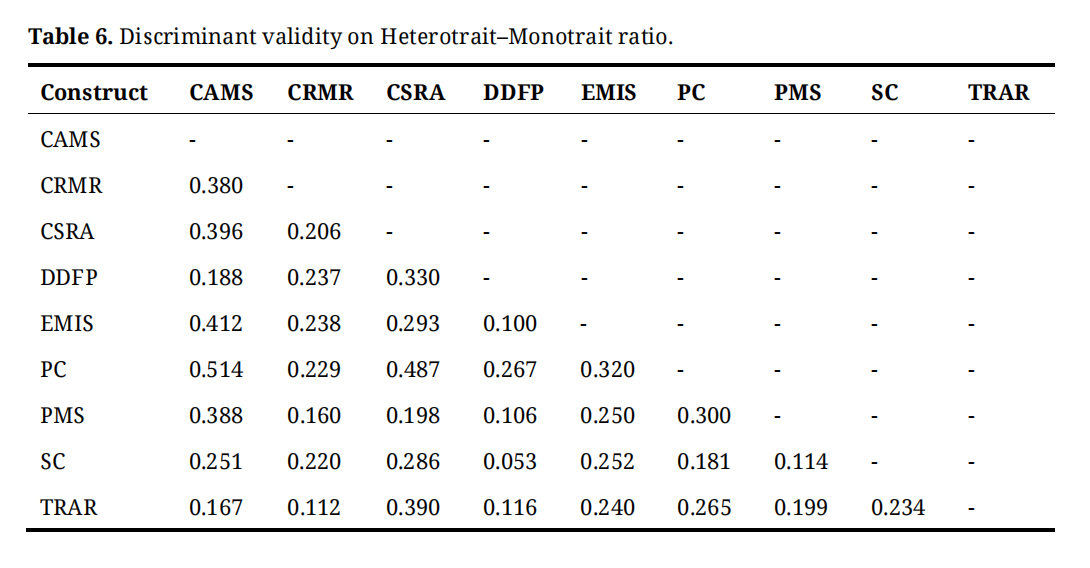

Furthermore, the HTMT results in Table 6 showed that the value of each construct was below the threshold of 0.85 as defined by [115]. Hence, with respect to the need of discriminant validity, the two criteria can be regarded as sufficiently satisfying the suggested model.

Table 6. Discriminant validity on Heterotrait–Monotrait ratio.

Table 6. Discriminant validity on Heterotrait–Monotrait ratio.

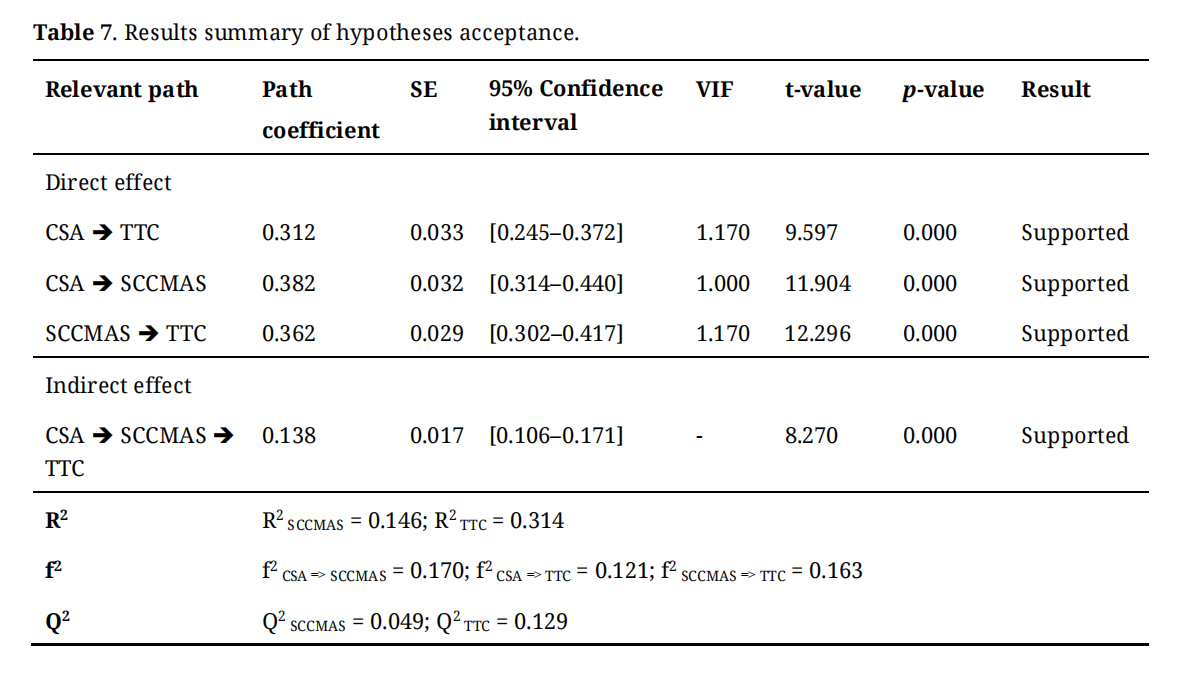

Based on the bootstrapping outcomes (10,000 resamples) in Table 7, the statistical outcomes revealed that CSA induced a significant and positive impact on TTC (β = 0.312; t-value = 9.597; p-value = 0.000) and SCCMAS (β = 0.382; t-value = 11.904; p-value = 0.000). In the same vein, SCCMAS was found to induce a significant and positive impact on TTC (β = 0.362; t-value = 12.296; p-value = 0.000). Therefore, H1-H3 were supported.

Indirect effectThe significance of CSA’s indirect effect on TTC through SCCMAS was gauged. Given that the direct effect of CSA on TTC was also supported and that the indirect effect was notable (β = 0.138; t-value = 8.270; p-value = 0.000), it disclosed that SCCMAS partially mediated the relationship between CSA and TTC [110]. To that end, these obtained outcomes confirmed partial mediation.

Based on the statistical results in Table 7, the value of R2 for SCCMAS and TTC were 0.146 and 0.314, respectively. As presented in Table 7, each variable in the proposed model had the significance of f2 changing from small to medium. The value of Q2 for TTC and SCCMAS were 0.129 and 0.049, respectively. All of these values were well above zero.

Table 7. Results summary of hypotheses acceptance.

Table 7. Results summary of hypotheses acceptance.

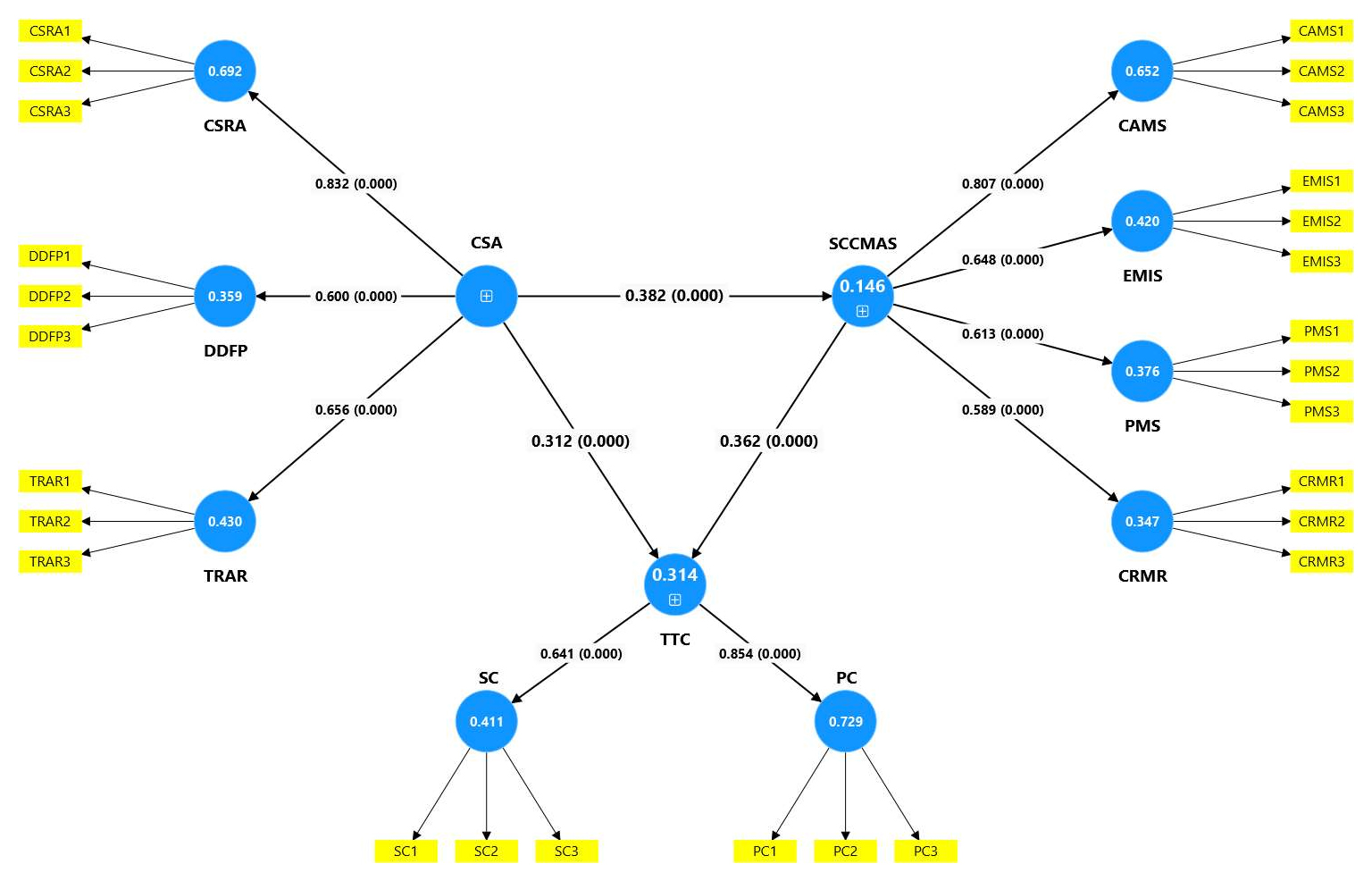

The structural model was employed to evaluate the hypothesized correlations in Figure 3.

Figure 3. Structural model.

Figure 3. Structural model.

We corroborated the PLS-SEM findings with fsQCA 4.0 to identify the sufficient and required causative conditions that contributed to twin transformation capabilities in PSOs. During the calibration phase, the standardized latent variable scores of all constructs were converted into fuzzy set scores via the direct calibration method. The initial phase of fsQCA entailed calibrating the data, which consisted of transforming raw data into set membership scores that ranged from 0.0 to 1.0 [116]. All variables in this study were assessed using a 7-point Likert scale. In calibrating these measures for fsQCA, this study adhered to the methodology established by [117], designating three qualitative anchors: the full membership threshold encompassed 95% of the data values; the full non-membership threshold encompassed 5% of the data values; and the crossover point encompassed 50% of the data values. This study modified the calibration approach in fsQCA [118] by adopting the procedure utilized by [118]. This calibration approach utilized three qualitative anchors: the full membership threshold, the full non-membership threshold, and the crossover point threshold, which were derived using a 7-point Likert scale survey. According to the suggestion of [119], the full membership threshold was established at a rating of 6, the full non-membership threshold at a rating of 3, and the crossover point at 4.5. This work established the full non-membership threshold at 3, in contrast to the threshold of 2 employed by [118]. This methodology was founded on the sample’s data values and contextual understanding [116]. Vietnamese employees exhibited a tendency to favor the right side (strongly agree) of the scale when responding to survey questionnaires [119].

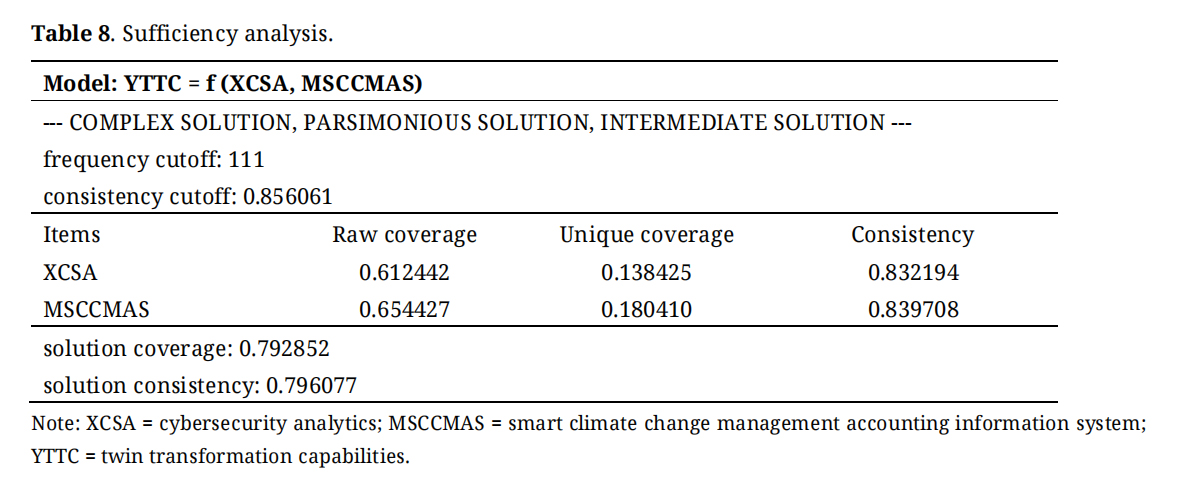

Sufficient conditions analysisBased on [117] recommendation, a consistency threshold should not be less than 0.75, this study chose a threshold of 0.80. Consistency and coverage must be more than 0.80 and 0.20, respectively, to demonstrate the sufficiency of a causal configuration or a single condition [120]. The results from fsQCA were shown in Table 8, revealed that the three fsQCA solutions yielded the same configurations. The score of consistency and coverage of cybersecurity analytics and smart climate change management accounting information system were higher than the recommended thresholds (Consistency > 0.80, Coverage > 0.20). It implied the parameter fit of observed configurations to produce high-level twin transformation capabilities consistently. As such, cybersecurity analytics and smart climate change management accounting information system were two sufficient conditions that explained twin transformation capabilities in PSO. Thus, these fsQCA findings were congruent with the SEM findings.

Table 8. Sufficiency analysis.

Table 8. Sufficiency analysis.

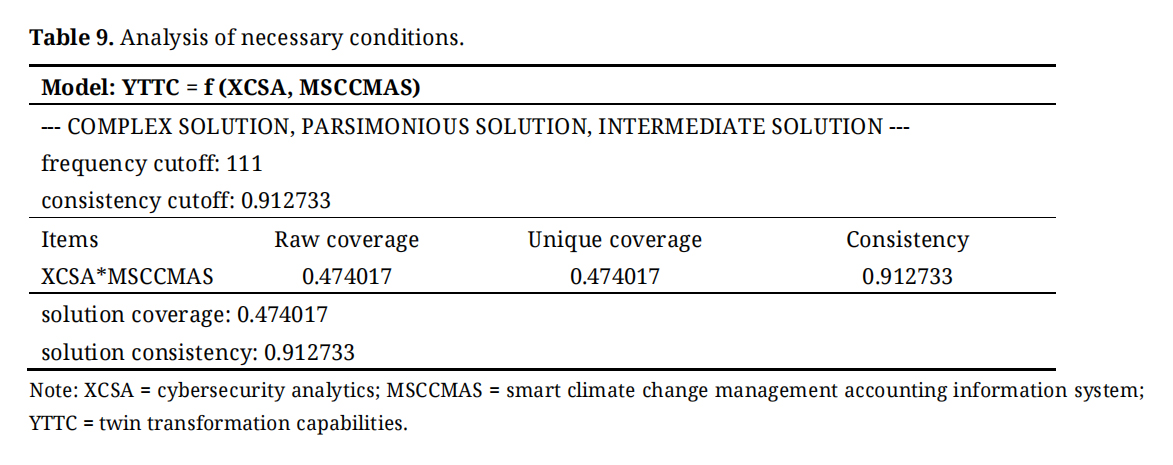

In the subsequent phase, a necessary condition analysis was conducted. This constitutes an INUS condition (insufficient but required component of a condition) that was unneeded yet sufficient for the outcome; [121]. The necessary condition evaluated if a configuration or an individual antecedent condition was essential for achieving the desired results [122], indicating the need to assess whether the distinct impact of each antecedent condition was requisite for the conclusion. A system consistency exceeding 0.9 often indicated that the antecedent conditions were requisite for the outcome [123]. The fsQCA findings were presented in Table 9. An in-depth analysis of the configurations indicated that the combination between cybersecurity analytics and smart climate change management accounting information system existed. This suggested that organizational managers will not succeed in obtaining twin transformation capabilities without accounting for both cybersecurity analytics and smart climate change management accounting information system.

Table 9. Analysis of necessary conditions.

Table 9. Analysis of necessary conditions.

Our findings indicate that the augmentation of CSA markedly improves and enhances TTC within PSOs. This obtained findings significantly enhances both academic knowledge and practical application, as the current literature on cybersecurity in PSOs, particularly prior studies, corroborates the influence of cybersecurity on the efficacy of digital transformation (i.e., [69,124–128]). Cybersecurity is essential for robust digital operations [129]; hence, organizations must enhance their cybersecurity practices through suitable strategies and cyber defensive capabilities [130] to address the increasing complexity of cyberattacks. They assert that cybersecurity competence is a paramount concern for organizations and governments globally in their digital transformation efforts. Cybersecurity has increasingly emerged as a critical concern for organizations due to the rise in cybersecurity incidents and cyber-attacks affecting entities worldwide [131] and hindering their digital transformation initiatives. This research is among the very few studies demonstrating that CSA positively influences TTC; prior research has not empirically examined this concept within the public sector setting. Twin transformation is the worldwide phenomena, garnering attention across many industries and inciting significant investment. Nevertheless, the inherent complexity of twin transformation necessitates cybersecurity awareness as an essential requirement. Overseeing twin transformation transcends mere technological considerations. It also involves a disturbance of organizational structure, culture, and leadership, hence presenting significant problems regarding skills and capabilities. The twin transformation primarily concerns individuals and the enhancement of digital capabilities and competences that synchronize all operations, processes, personnel, and culture, aligning them with specific organizational objectives. In line with 13 in-depth interviews in a qualitative phase, the interviewees also placed emphasis on this point of view, according to the Deputy Head of finance and administration department, “The simultaneous transformation of sustainability and technology in an organizational context is the hallmark of twin transformation. This pervasive transformation has also introduced substantial technological risks that pose a threat to the digital environment. There are numerous types of cyberattacks, each with its own unique objective; the most prevalent types are theft and devastation. Data security is frequently a component of sustainable objectives in the digital environment, as evidenced by the 2030 agenda, which emphasizes data-driven governance. Thus, an increasing number of organizations are investing in cybersecurity training to address the growing technological challenges. This training is evolving in tandem with the hazards it is attempting to mitigate” (P02, Deputy Head of finance and administration department).

The qualitative and quantitative outcomes put accent on the significance of SCCMAS in the relationship between CSA and TTC, and elucidate the rationale for PSO to incorporate such a system into their considerations. In line with 13 in-depth interviews in a qualitative phase, the interviewees also placed emphasis on this point of view, according to the lecturer in public university, “The environmental, economic, and societal implications of the climate crisis are multifaceted. Because cyberattacks impact equipment installations, communication networks, and supply chain management, climate change also poses a direct danger to operations. Damage to operational preparedness and exposure of sensitive data across all systems to cyber-attacks are both caused by these disruptions” (P05, Lecturer in public university). The global climate crisis compels nations and international organizations worldwide to implement actions and strategies to effectively address climate change, aiming to reduce greenhouse gas emissions while preparing for its adverse impacts [132]. The swift digitalization of settings and vital infrastructure is occurring and may facilitate the timely or even expedited achievement of objective goals [133]. This research is among the very few studies casting light on how SCCMAS partially mediates the relationship between CSA and TTC; prior research has not empirically examined this concept within the public sector setting. In line with 13 in-depth interviews in a qualitative phase, the interviewees also placed emphasis on this point of view, according to the chief accountant in public college, “Climate change management accounting plays a crucial role in facilitating sustainable strategic and operational decisions about climate change management. Climate change management accounting provides tools and procedures that enable organizations to comprehend the magnitude of the issue, develop viable solutions, and assure the proper implementation of these solutions for effective climate change management” (P08, Chief accountant in public college). Based on the perspectives of [134], climate changes are occurring more rapidly now than at any previous time. Global changes in climate policy have progressively necessitated organizations to adopt ecologically sustainable operations. Management accounting is essential for formulating organizational level strategy and risk management, and it can significantly aid societal initiatives to address climate change [46].

Implication in practiceThe findings from this manuscript have practical significance for PSOs who are interested in utilizing various resources to enhance their twin transformation and adjust to the evolving business landscape. Empirical evidence indicates that CSA is the main determinant of TTC in PSOs. Succinctly put, attaining success in twin transformation requires significant investments in CSA. Thus, PSOs’ leaders should enhance their cognitive skills and give priority to the significance of CSA and its contribution to boosting TTC. The results indicate that including SCCMAS in PSOs can serve as a catalyst for attaining TTC. Nevertheless, PSOs are now encountering myriad challenges that hinder their complete realization of their potential. To expedite the implementation of SCCMAS in PSOs, it is advisable to concentrate on concrete resources such as infrastructure, digital platforms, human resource and other essential resources for carrying out this effort. Concretely, all leaders in PSOs should carefully assess their specific situations to implement the required measures to improve organizations’ technological proficiency, promote a proactive exploration for technological solutions and provide appropriate training program on climate change management accounting practices for accounting staff.

Policy-makers have played a crucial role in the digital transformation of PSOs. Government support would equip PSOs with the essential resources and resolve to surmount the obstacles posed by digitization. This aim might be achieved by the government implementing appropriate rules, incentives, and programs, as well as providing guidance and support at all stages of PSO digital transformation and sustainability transformation. The government may enhance the effectiveness of PSOs by providing public officials with opportunities to engage in digital education or training. Concurrently, the government may provide support to PSOs in developing a digital learning and training platform for their staff, therefore enabling the PSO to reduce costs associated with recruiting and training new team members. Furthermore, the International Public Sector Accounting Standards Board should give priority to address the processes involved in conducting climate change management accounting practices and provide guidelines in preparation and presentation of climate change management reporting.

Given the escalating severity of digital and climate threats, including cyber-attacks and catastrophic weather occurrences, digital transformation and sustainability transformation have become imperative for nearly all organizations [8]. Intricate challenges related to digitalization and sustainability necessitate cohesive solutions, as isolated thinking overlooks the synergistic potential of the relationship between digital and sustainability transformations [6]. This study sought to clarify the intricate linkages among CSA, SCCMAS, and TTC within the frameworks of dynamic capabilities theory and stakeholder theory. The study utilizes PLS-SEM and fsQCA as complimentary approaches for data analysis, hence improving the precision of the results relative to prior research. In conclusion, our data emphasizes that TTC is influenced by intricate interdependencies between CSA and SCCMAS rather than by a singular factor. We anticipate that our work will motivate future research to transcend individual elements and examine how combinations of situations synergistically contribute to the twin transformation in PSO.

While this work has met its objectives and produced significant results, some limitations must be recognized and addressed in future research. The current study was cross-sectional due to time constraints, signifying that it assessed all proposed constructs at a singular point in time. The achievement of digital transformation and sustainable transformation necessitates that PSOs develop new perspectives in their operations. The longitudinal method is the most appropriate answer for this objective. Secondly, this study collected data from PSOs in Vietnam. Future researchers may expand the geographic scope by conducting studies in different countries to evaluate the applicability of the study paradigm across various cultures. Thirdly, the study utilized convenience and snowball sampling methods, thereby limiting the generalizability of the results. Therefore, future researches should employ random sampling techniques to improve generalizability and validity. The research utilized a constrained sample size. Future research may be augmented by utilizing a larger sample to get increased data representation. Moreover, an additional limitation of the study related to the data collection methods. The study utilized a self-administered survey questionnaire for data collection, suggesting the possibility of response bias among participants, despite the application of requisite measures to identify this concern. In light of the aforementioned constraints, it is advisable that subsequent study investigates diverse data collection approaches. This study investigated the function of SCCMAS as the exclusive mediator in the relationship between CSA and TTC. Therefore, future researchers should include more factors as mediator to improve understanding of the relative importance of each element.

The dataset of the study is available from the authors upon reasonable request.

Conceptualization, PQH; Methodology, PQH; Software, PQH and VKP; Validation, PQH and VKP; Formal Analysis, PQH and VKP; Investigation, PQH and VKP; Writing—Original Draft Preparation, PQH; Writing—Review & Editing, PQH; Visualization, PQH; Supervision, PQH.

The authors declare that they have no conflicts of interest.

This work was supported and funded by the University of Economics Ho Chi Minh City (UEH) in Vietnam.

Interview Guide

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

62.

63.

64.

65.

66.

67.

68.

69.

70.

71.

72.

73.

74.

75.

76.

77.

78.

79.

80.

81.

82.

83.

84.

85.

86.

87.

88.

89.

90.

91.

92.

93.

94.

95.

96.

97.

98.

99.

100.

101.

102.

103.

104.

105.

106.

107.

108.

109.

110.

111.

112.

113.

114.

115.

116.

117.

118.

119.

120.

121.

122.

123.

124.

125.

126.

127.

128.

129.

130.

131.

132.

133.

134.

Huy PO, Phuc VK. Leading Twin Transformation and Sustainability: Unveiling the Role of Cybersecurity Analytics at Smart Climate Change Management Accounting System. J Sustain Res. 2025;7(2):e250024. https://doi.org/10.20900/jsr20250024.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions