Location: Home >> Detail

J Sustain Res. 2026;8(1):e260028. https://doi.org/10.20900/jsr20260028

,

Mária Szalmáné Csete

,

Mária Szalmáné Csete

Department of Environmental Economics and Sustainability, Faculty of Economic and Social Sciences, Budapest University of Technology and Economics, H-1111 Budapest, Hungary

* Correspondence: István Vokony

Large multinational energy companies face a strategic trilemma in balancing growth, strategy, and sustainability, which are often difficult to integrate and insufficiently supported by measurable performance indicators. Despite the extensive literature on Sustainability Balanced Scorecard (SBSC) models, prior frameworks remain limited in their ability to differentiate human-related performance drivers, to embed risk management logic structurally, and to reflect sector-specific characteristics of the energy industry. This study aims to develop a structured, metrics-based framework that strengthens sustainability-oriented strategic planning and decision-making. Adopting a design science research perspective, the study proposes an enhanced Balanced Scorecard model, the Sustainable Six-Perspective Balanced Scorecard (HEX-BSC). Building on the Sustainability Balanced Scorecard, the framework expands the traditional four perspectives to six: financial, external customer, internal customer (employee), corporate culture, internal processes, and sustainability. A human-centred structure separates employee satisfaction from organizational culture to improve diagnostic precision. A 4T risk-management module—Transfer, Terminate, Tolerate, Treat—is embedded within each perspective to support dynamic and responsive performance management. Qualitative feedback from senior leaders in the Hungarian energy sector indicates that the HEX-BSC is both conceptually robust and practically interpretable. By explicitly linking outcomes across perspectives–such as assessing how product launches affect sales, customer experience, employee workload, processes, and sustainability—the model enhances strategic alignment, transparency, and organizational learning. The novelty of the HEX-BSC lies in its explicit separation of employee and corporate culture perspectives, the integration of a 4T risk-management logic across all dimensions, and its energy-sector-specific design.

4T, Transfer, Terminate, Tolerate, Treat; BI, Business Intelligence; BMC, Business Model Canvas; BPR, Business Process Reengineering; BSC, Balanced Scorecard; CAC, Customer Acquisition Cost; CEO, Chief Executive Officer; CLTV, Customer Lifetime Value; CPI, Cost Performance Index; CRM, customer Relationship Management; CSR, Corporate Social Responsibility; EEI, Employee Engagement Index; EPS, Earnings per Share; ERM, Enterprise Risk Management; ESG, Environmental, Social and Governance; GDP, Gross Domestic Product; HEX-BSC, Sustainable, Six-Perspective Balanced Scorecard Framework; HR, Human Resources; KPI, Key Performance Indicator; MRI, Magnetic Resonance Imaging; NPS, Net Promoter Score; P/E ratio, Price-to-Earnings Ratio; R&D, Research and Development; RBV, Resource-Based View; ROA, Return on Assets; ROE, Return on Equity; ROI, Return on Investment; SPI, Schedule Performance Index; TEM, Transmission Electron Microscopy; TGF, Transforming Growth Factor; TLBMC, Triple Layered Business Model Canvas; TOC, Theory of Constraints; TQM, Total Quality Management

Nowadays, it is not enough for an energy company to achieve or maximize profit. It must also meet soft expectations that are opposite or point in the opposite direction to profit maximization: corporate culture [1], customer focus [2], and sustainability [3]. These are basic building blocks for a modern corporate strategy [4] and not just checkmarks in the administration.

The Balanced Scorecard (BSC) was introduced by Kaplan and Norton in 1992 [5] as a major advance. It measures organisational results across four key perspectives: (i) financial performance, (ii) customer satisfaction, (iii) internal business processes and (iv) learning and growth—helping to translate strategic objectives into operational metrics and to achieve a balance between tangible and intangible elements in corporate evaluation.

However, the implementation of the BSC and other traditional performance measurement systems has encountered numerous problems [6]. Common issues include selecting appropriate Key Performance Indicators (KPIs), losing focus due to an excessive number of metrics, lack of management commitment, and poor data quality [7]. A critical obstacle is that the traditional BSC does not involve all stakeholders or factors. For example, its four standard perspectives do not sufficiently emphasise employees as a distinct stakeholder group and do not explicitly address risks or external environmental impacts either [8]. Consequently, several organisations fail to achieve the desired outcomes with the BSC; and in some cases, the system’s rigidity and closed mindset even hinder innovation and collaboration between companies [9].

Thus, performance measurement systems continue to evolve. New models, such as the Performance Prism, have emerged to overcome the limitations of the BSC and to evaluate organisations by involving a broader range of stakeholders (e.g., suppliers, society) [10].

In recent years, the rise of sustainability and digitalisation has placed additional pressure on performance measurement. Companies are expected to integrate environmental and social considerations into their strategies, not only for ethical reasons but because their long-term competitiveness depends on it. Consequently, numerous organisations have introduced a fifth sustainability dimension alongside the original four BSC dimensions [11]. This step reflects changes in the global business environment and increasing societal expectations—namely, the notion that companies must consider the long-term environmental and social impacts of their activities. Under the integrated “triple bottom line” perspective, corporate success is now measured in three areas: financial performance (profit), social responsibility (people) and environmental impact (planet) [12].

Despite the growing body of literature on Sustainability Balanced Scorecard (SBSC) frameworks, several structural limitations remain [13,14]. First, most SBSC models treat employee-related outcomes and deeper organisational culture drivers as a single dimension, limiting diagnostic precision in human-centred performance management. Second, risk management is typically addressed through parallel governance systems rather than being structurally embedded within performance measurement perspectives. Third, many sustainability-oriented scorecards remain generic and insufficiently adapted to the regulatory, infrastructural and capital-intensive characteristics of the energy sector. These limitations highlight a research gap in the design of performance management systems that simultaneously integrate human-centred differentiation, embedded risk logic and sector-specific requirements.

Accordingly, the present study addresses how sustainability considerations, human-centred performance dimensions and risk management logic can be structurally integrated into an enhanced Balanced Scorecard framework tailored to the energy sector. The objective of this paper is to design and conceptually justify a six-perspective, sustainability-oriented Balanced Scorecard framework tailored to the energy sector, and to refine its structure through qualitative expert validation. The evaluation system proposed here addresses these challenges: it simultaneously provides a holistic view of the company’s operations, supports strategic decision-making, and aligns with 21st-century expectations—including sustainable development goals.

This paper adopts a design science research approach to address a structural gap in sustainability-oriented performance management systems in the energy sector. Rather than empirically testing performance outcomes, this study follows a design science research logic and focuses on the conceptual development, structural coherence and expert-informed refinement of a performance management artefact. Following the design science research paradigm, the study focuses on the development and conceptual validation of a performance management artifact rather than the empirical testing of causal relationships. In this context, the HEX-BSC framework represents the central artifact, designed to address structural limitations identified in existing Sustainability Balanced Scorecard models. The design process builds on established theoretical knowledge, integrates sector-specific managerial requirements, and incorporates qualitative expert feedback to refine the framework’s structure and interpretability. This approach aligns with the core objective of design science research: generating practically relevant and theoretically grounded solutions to complex organisational problems.

The Literature Review section summarises the key management, performance-measurement, sustainability and business-model concepts that form the foundation of the proposed framework. The Methods section details the procedures followed during the creation of the HEX-BSC system. The Results section introduces the HEX-BSC system, detailing its six perspectives and the integrated 4T risk-management logic. The Discussion section evaluates the framework’s added value, contrasts it with traditional models and discusses initial validation considerations. Finally, the Conclusions and Further Steps section synthesises the main insights and outlines practical implications and avenues for future research.

This section presents those performance measurement systems that were relevant for the development of a new, enhanced scorecard system.

Management Theoretical FoundationsIn his impactful article, Koontz (1980) [15] described the developed theoretical diversity in management as a “management theory jungle”, pointing out that the science of management encompasses numerous schools (classical school, human relations school, systems approach, contingency theory, etc.). A common insight from these diverse approaches is that a purely financial focus in management is insufficient; organisational behaviour, culture, innovation and alignment with the external environment are also critical to success [16,17].

Recent decades have seen the rise of strategic management theories such as Michael Porter’s competitive strategies and an increasingly influential stakeholder theory, all emphasising that corporate performance must be interpreted in a multidimensional way [18]. The stakeholder approach, for example, draws attention to the fact that not only should shareholder value be maximized [19,20], but also the needs of customers, employees, suppliers and, more broadly, society must be met to ensure long-term success [18].

Performance Measurement and Scorecard ModelsIn the performance measurement literature, the Balanced Scorecard (BSC) has received prominent attention [21]. The BSC is a strategic management framework that supplements financial metrics with three additional perspectives (customer, internal processes, learning and growth) [22], thereby providing a balanced view of the company’s operations. Since Kaplan and Norton’s original 1992 concept [5], the BSC has been widely used for communicating and decomposing strategy. The advantage of the BSC is that it links operational activities to corporate strategy and provides managers with comprehensive insight into the value-creation processes [3].

The BSC’s four perspectives—(i) Financial, (ii) Customer, (iii) Internal Processes and (iv) Learning and Growth—cover the main dimensions of a company’s operations, encouraging management to focus not only on immediate financial outcomes but also on customer relationships, process efficiency and long-term capacity development [23,24]. This approach acknowledges that measuring and developing intangible assets (such as knowledge or organisational culture) leads to improved financial performance in the long run [25].

However, criticisms of the BSC have been raised by researchers [6–9]. They note, for example, that the BSC concept does not define a clear causal relationship between the metrics and organisational performance, and its standard perspectives omit certain stakeholder groups (e.g., suppliers, communities) [26–29]. Furthermore, because the original BSC has four fixed categories, it can sometimes be inflexible [30]: there is a danger that managers think only within this framework, overlooking success factors or risks outside it. In the literature [8], successive “generations” of the BSC have appeared (2nd generation—adding strategy maps [31]; 3rd generation—networks of objectives and measures, etc. [32]), which attempted to address conceptual deficiencies, but in practice there remain significant differences in implementation success [28,30]

These criticisms have given rise to alternative models. For example, the Performance Prism [10] uses five perspectives, explicitly emphasising stakeholder satisfaction and contribution so that companies explicitly analyses what stakeholders expect from them and what they expect from stakeholders [27]. Similarly, the Denison model of organisational culture focuses on the link between corporate culture and performance, evaluating culture in four main dimensions (Adaptability, Mission, Involvement, Consistency) [33]. Denison and Mishra (1995) [33] empirically demonstrated that organisations with strong, well-balanced cultures have better financial indicators, innovative capacity and customer satisfaction [34]. The practical tool of the Denison model, the Denison Organizational Culture Survey, is a widely used questionnaire that quantifies culture and has found strong correlations with metrics like ROE (Return on Equity), ROI (Return on Investment), sales growth or quality [33]. This theoretical foundation supports the idea that corporate culture—as a performance driver—should be included in evaluation systems.

Centralised versus decentralised corporate governance also provides important theoretical context for system design. Different organisational structures affect performance in different ways [35]. Classic organisational theory [36] suggests that mechanistic (centralised, highly formalised) structures are efficient in stable environments, whereas organic (decentralised, flexible) forms are more effective in volatile environments, as they foster innovation and rapid adaptation. Today’s global companies often use hybrid structures [37], combining the benefits of centralisation (economies of scale, unified control) with decentralisation (local decision-making, flexibility).

Some research [38] suggests that centralisation can reduce costs and improve operational efficiency in certain areas (for example, lower logistics costs in the supply chain) and can standardise processes, which increases control. However, excessive centralisation may inhibit creativity and local-level innovation, which is why many authors emphasise the importance of an ambidextrous (dual-capability) organisation that can be efficient and innovative at the same time [39].

In summary, organisational structure and governance models influence how successful a performance measurement system will be. In a decentralised organisation, for example, responsibility for KPIs can be shared more broadly, whereas a centralised model allows for a strong central oversight of KPIs.

Corporate Processes and OptimisationPerformance measurement is closely intertwined with process management and improvement [40]. The theoretical roots of analysing organisational processes reach back to Frederick Taylor’s scientific management, which aimed at maximising efficiency. Later, the philosophies of Total Quality Management (TQM) [41] and continuous improvement (Kaizen) emphasised involving workers at all levels and continuously refining processes to improve quality and efficiency.

The Business Process Reengineering (BPR) offered a more radical approach: according to [42] processes need to be fundamentally rethought and redesigned to achieve breakthrough improvements in performance indicators (cost, quality, service level, throughput time, etc.). The definition of BPR is a fundamental rethinking and radical restructuring of business processes to deliver significant [43] improvements across critical modern performance indicators [44]. This approach brought significant results in many companies during the 1990s, although its excessive radicalism often led to failures.

In the past two decades, Lean management [45] and Six Sigma methodologies [46] have proven successful in process optimisation: Lean focuses on eliminating waste and improving flow, while Six Sigma uses data-driven problem solving to minimise defects [47]. Both approaches have numerous case studies and research [48,49] showing their efficiency-enhancing effects across industries from manufacturing to services. The literature indicates [50,51] that well-defined and optimised processes not only reduce operational costs, but also increase customer satisfaction (through faster, more reliable service) and employee engagement (by providing transparent, meaningful workflows) [52].

The theory of constraints (TOC) [53,54], for example, reminds us that system performance is determined by its most constraining bottleneck, so a measurement system must be able to identify these critical points in order to enable targeted improvement interventions [55].

Sustainability and Corporate EfficiencyIntegrating sustainability into corporate management has become one of the key management trends of the 2000s [56]. Since John Elkington’s Triple Bottom Line concept (1997) [57], it has been understood that economic, environmental and social performance together determine a company’s long-term sustainability. Initially, many believed [58,59] that sustainability investments would reduce financial performance, but a number of studies have contradicted this. For example, a comprehensive meta-analysis (NYU Stern, 2021) [36] found that nearly 60% of studies showed a positive correlation between ESG (environmental, social and governance) metrics and financial performance, and only a negligible share showed a negative correlation [60]. These findings suggest that companies integrating sustainability into their strategies can gain a competitive advantage: resource efficiency improves (using less energy and material, thereby lowering costs), and brand and customer loyalty strengthen (consumers appreciate responsible companies), while risks decrease (e.g., compliance with regulations, avoidance of scandals) [61].

Porter and Kramer’s (2011) [36] shared value creation theory argues that corporate competitiveness and societal well-being can be linked—that is, sustainability innovations embedded in business models provide advantages on both fronts. This is exemplified by the spread of circular economy principles, where reducing waste and recycling not only protect the environment but also save costs for companies [36].

In this context, linking sustainability and efficiency becomes even more direct. Companies must cooperate with municipalities and other institutions to optimise resource use (for example, smart grids to reduce energy consumption, or improving public transportation to enhance workers’ mobility) [62]. A sustainable company does not operate in isolation but is part of a larger ecosystem, and thus its performance is partly judged by how much it contributes to community goals (such as reducing carbon emissions or improving urban quality of life) [28].

In the academic literature, the concept of a Sustainability Balanced Scorecard (SBSC) appears increasingly, integrating environmental and social metrics into the traditional BSC. For example, Figge et al. (2002) [57] developed a theoretical framework to create a link between sustainability management and business strategy. This perspective filters down to the corporate level as well, since a company operating in the energy sector would benefit from aligning its own scorecard with the objectives (for example, participating in energy efficiency programmes [63], supporting community initiatives, and applying digital innovations in its operations).

Business Model Canvas and Balanced ScorecardThe Triple Layered Business Model Canvas (TLBMC) is an extension of the traditional Business Model Canvas (BMC) [64], enabling the analysis of a business model in three interlinked layers: economic, environmental and social [64]. Its goal is to interpret business value creation not only from a financial perspective, but by considering the full impact system of the company. In the TLBMC, the original BMC constitutes the economic layer [65], to which two new layers are added: the environmental layer, which structures environmental impacts across the life cycle, and the social layer, which examines the company’s stakeholder-based social impacts. The tripartite structure reflects the different types of value and the relationships between them [66].

The significance of the TLBMC lies in providing an integrated framework that supports the exploration of sustainability aspects, the identification of innovation opportunities, and the development of the business model. The model clearly increases corporate transparency and helps align economic, environmental and social impacts, thus making strategic decision-making better informed. Its environmental layer—based on life-cycle analysis—and its stakeholder-oriented social layer make it particularly suitable for companies that are developing and evaluating new business model alternatives during the sustainability transition [67].

The BSC and TLBMC can be well integrated, as the two tools capture different yet complementary aspects of value creation. The BMC—and its extension, the TLBMC—describes the logical construction of the business model, i.e., how the company creates, delivers and captures value. The BSC, by contrast, is a performance management system that supports the operational implementation of strategy through KPIs and strategic objectives. The elements described in the TLBMC can be easily mapped onto the BSC perspectives: the value proposition and customer segments align with the Customer perspective [68]; key activities and resources align with the Internal Processes and Learning–Growth perspectives; while the revenue and cost structure corresponds to the Financial perspective.

In summary, the literature review clearly shows that the evaluation system to be introduced here is supported by numerous theoretical pillars. On the one hand, strategic management frameworks (such as the BSC [5] and the Performance Prism [10]) ensure a holistic perspective and strategic alignment. On the other hand, organisational behaviour and culture theories (e.g., Denison and Mishra, 1995) [33] emphasise the importance of human factors in performance. Sustainability concepts incorporate the external challenges of the 21st century into corporate governance. Together, these theories establish the foundation for a new scorecard system that is not only a measurement tool but also a catalyst for organisational learning and adaptation [69].

The HEX-BSC framework was developed using a design science research approach, meaning it was built as an artifact grounded in existing theory and practical needs and then refined through evaluation. The classic BSC has four perspectives, but Kaplan and Norton [70] themselves note that these perspectives are not rigid and can be expanded to meet specific organizational needs. Building on this insight, prior researchers have successfully introduced new perspectives to the BSC–for example, Figge et al. (2002) [57] added a fifth “environmental and social” perspective to incorporate sustainability considerations. Such adaptations demonstrate that adding dimensions to the BSC is an accepted method for enhancing its strategic relevance.

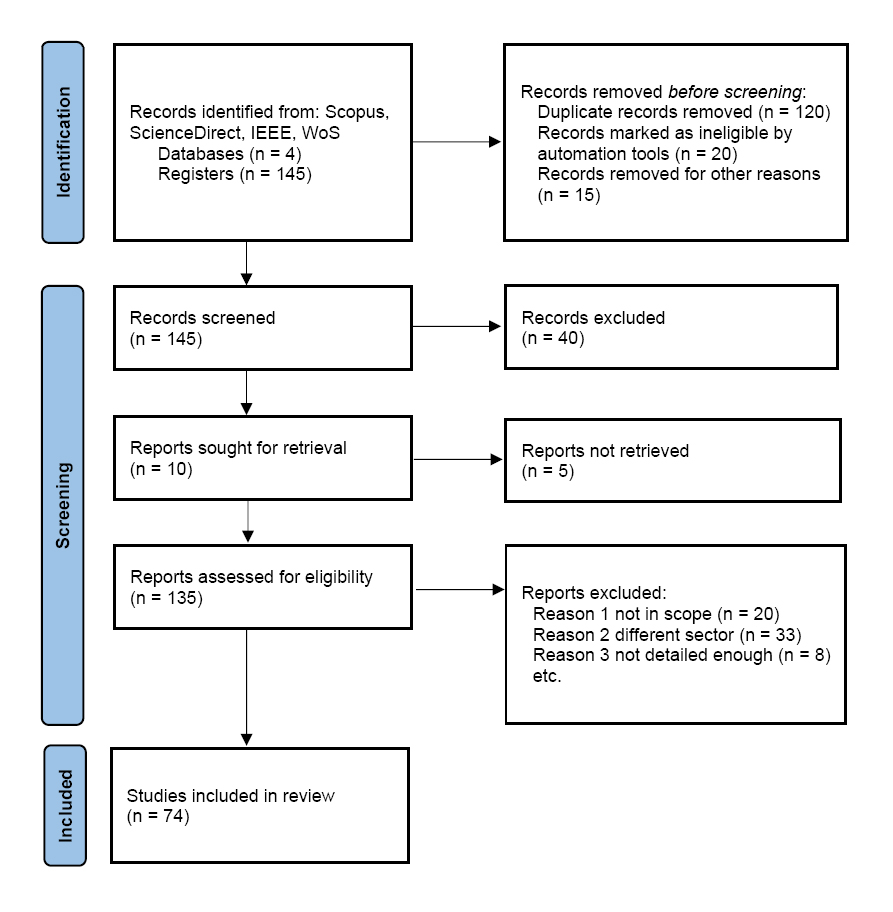

To enhance methodological transparency, the research process is illustrated in Figure 1, which presents the integration of the systematic literature review and design science research approach. Furthermore, Figure 2 links the identified research gap and research questions to the applied methodological steps and the resulting HEX-BSC artifact. The systematic literature review process itself is documented using a PRISMA 2020 flow diagram (Figure 3), ensuring traceability and reproducibility of the literature selection procedure.

Figure 1. Research methodology framework.

Figure 1. Research methodology framework.

Figure 2. Alignment of research gap, methodology and outcomes.

Figure 2. Alignment of research gap, methodology and outcomes.

Figure 3. PRISMA flow diagram.

Figure 3. PRISMA flow diagram.

In our case, two new perspectives were introduced to address areas that the traditional BSC did not explicitly cover: sustainability and organizational culture. Figge et al. [57] showed that sustainability (encompassing environmental, social, and long-term governance concerns) have become integral components of modern corporate strategy and performance management. It has been emphasized that integrating Environmental, Social, and Governance (ESG) objectives into performance frameworks is increasingly crucial for aligning strategy with stakeholder expectations. Likewise, organizational culture and human capital are now recognized as key drivers of success, warranting their inclusion in strategic measurement systems. In fact, Rühle and Wagner (2017) [12] demonstrated a modified BSC with an additional culture-focused perspective, arguing that giving organizational culture its own perspective can positively impact overall business performance. This idea was grounded in a thorough literature review and a case study, underscoring the methodological soundness of deriving new BSC dimensions from research and empirical insight. By following a similar evidence-based design process, we ensured that the new sustainability and culture dimensions of HEX-BSC are well-founded in theory and practice rather than arbitrary additions.

Methodologically, the extension of the BSC was executed with rigor and justification. We treated the HEX-BSC as a design artifact, using the knowledge base (academic literature on BSC and sustainability/culture integration) to inform its structure. The decision to add exactly two perspectives was guided by documented needs: one for Sustainability (reflecting the growing importance of sustainable strategy and risk management), and one for Corporate Culture/People (reflecting the human and organizational capital aspects). For instance, a study in the banking sector [71] proposed adding “Risk” and “Agility” perspectives to the BSC to address the fast-changing environment of banks. Similarly, our HEX-BSC extension addresses the evolving context of the energy sector by explicitly incorporating sustainability and cultural factors, which are critical for long-term strategic success in energy industry. We relied on established concepts like the Sustainability Balanced Scorecard (SBSC), which integrates environmental and social goals into performance management, and on organizational development research highlighting culture as a strategic performance driver. By citing and building upon these frameworks, we ensured the HEX-BSC’s additional dimensions are methodologically justified and supported by prior studies rather than being invented in isolation.

Finally, the name “HEX-BSC” reflects the framework’s six perspectives (hexagonally extended BSC). Expanding the scorecard to six dimensions yields a more comprehensive tool—one that still encompasses the original financial, customer, internal process, and learning & growth perspectives, but now augmented with sustainability and culture. This holistic design is intended to capture a wider range of value drivers and strategic objectives relevant in today’s business environment.

To support the validity and practical relevance of the proposed HEX-BSC framework, qualitative input was collected from key industrial stakeholders in the energy sector. Semi-structured expert interviews were conducted with senior executives from EON Hungaria, Opus Global, MVM Group, and MOL Group. The interviews were recorded, transcribed, and systematically analysed using thematic evaluation techniques. Their primary objective was to assess the conceptual soundness, managerial interpretability, and sectoral applicability of the HEX-BSC perspectives and KPI logic, as well as to provide feedback on the completeness and usability of the proposed metric system. Insights derived from this evaluation process were directly incorporated into the refinement and finalisation of the HEX-BSC metrics and perspective structure. In the present paper, these empirical insights are only referenced at a high level to support the conceptual positioning of the framework; a detailed empirical analysis of the interview material and its sector-specific implications will be reported in a dedicated follow-up publication.

The proposed corporate scorecard system, HEX-BSC, is an integrated framework that evaluates corporate performance across multiple dimensions and combines traditional KPI-based metrics with risk management aspects. While the starting point was the Balanced Scorecard logic, the system has been significantly expanded and tailored to today’s needs. The structure of the system includes the following main perspectives: Financial, External Customer (Client), Internal Customer (Employee), Corporate Culture (Denison model), Internal Processes and Sustainability. Below, each of these perspectives are described in detail.

Moreover, the indicators were designed to be collected and analysed centrally (digitalised reporting, BI dashboard), but also to be assignable at the organisational level. For example, each indicator has a responsible department head who evaluates the results monthly.

Financial PerspectiveThis perspective includes traditional financial performance metrics, such as the revenue growth rate, profitability indicators (e.g., ROE—return on equity, ROA—return on assets), market value indicators (P/E ratio, EPS—earnings per share), and indicators of financial stability (debt-to-equity ratio, liquidity ratio). These financial dimension metrics answer the question of how well the company’s strategy leads to the desired economic outcomes.

In selecting the indicators, it was also considered that they align with sustainability—for example, metrics indicating long-term value creation are prioritised over short-term profit. One of the innovations in the HEX-BSC is that within each perspective—including the financial—the 4T risk management strategies [72] are defined. For example, in the financial perspective:

●

●

●

●

This dimension measures how satisfied the company’s customers are and how successful the company’s market presence is. Key indicators include, for example, the Net Promoter Score (NPS), which indicates whether customers would recommend the company to others; the customer retention rate, which reflects the proportion of loyal customers; the Customer Acquisition Cost (CAC); and the customer lifetime value (CLTV), which together measure the efficiency of marketing and sales. Customer service performance is also important (e.g., number of complaints, average response time, first-contact resolution rate). These KPIs indicate the company’s degree of market orientation and customer-centricity—since customer satisfaction and loyalty are prerequisites for long-term financial success.

The innovation in HEX-BSC is that within this perspective the 4T logic also appears:

●

●

●

●

This way, the HEX-BSC ensures that risks and opportunities related to customers are not ignored. For example, if the number of complaints increases (a negative KPI), the system provides a framework to consider whether to treat or transfer this risk (for instance, by outsourcing the call centre).

Internal Customer (Employee) PerspectiveIn the traditional BSC, measures related to employees appear under the Learning and Growth perspective, but in the HEX-BSC proposed here, they are treated as a separate dimension focusing on internal customers, i.e., employee satisfaction and engagement. The theoretical basis for this decision is that employee satisfaction has a direct impact on corporate performance (e.g., service quality, innovation, turnover costs). Key indicators include the Employee Engagement Index (EEI), which assesses motivation and commitment at work; the turnover rate (proportion of voluntary exits); absenteeism and sick days, which signal workplace climate and health; the results of 360-degree evaluations; and the rate of internal promotions, which indicate the success of talent management. These indicators give management insight into how strong internal loyalty and human capital development are, forming the basis for becoming a learning organisation.

This dimension also incorporates the 4T elements:

●

●

●

●

The methodology in this area also draws on elements of the Denison culture model [73]—for example, by measuring the dimensions of Involvement and Consistency. The data collected here are not only used for HR feedback but are also incorporated into strategic evaluation, indicating that human resources are a key factor in strategy execution.

Corporate Culture PerspectiveAlthough corporate culture and employee satisfaction are closely related, the system treats culture as a separate dimension in order to make it measurable at a strategic level. The four cultural components from the Denison model are integrated into the HEX-BSC:

●

●

●

●

This approach results in culture becoming a measurable and manageable element of corporate governance, instead of being regarded only as a background factor.

Internal Processes PerspectiveThis perspective evaluates the company’s operational efficiency and the effectiveness of its processes. The main indicators come from project management and production: for example, the project success rate (the proportion of projects completed on time and within budget), lead times in key processes, process quality (defect rate, rework rate), ROI of capital projects, as well as cost-performance indices (CPI, SPI) for projects. Also included are resource utilisation metrics (e.g., capacity utilisation of machines and human resources), and indicators of innovation processes (time to market for new products, percentage of R&D expenditure).

The measurement of internal processes relies on lean and BPR principles, that is, simplifying and standardising processes wherever possible and organising them around customer value creation. The 4T model is applied here as follows:

●

●

●

●

This methodology’s advantage is that by connecting internal process metrics with risk management strategies, management not only sees where problems are (for example, recurring defects on a production line) but also immediately receives suggestions for the appropriate type of response (e.g., to Treat—initiate a maintenance project, or to Transfer—engage a specialised subcontractor for that subprocess).

Sustainability PerspectiveThis perspective explicitly includes environmental and social performance metrics, aligning the system with the Sustainability Balanced Scorecard approach. The main indicators here come from the key areas of environmental impact and social responsibility: for example, annual carbon dioxide emissions (carbon footprint), energy consumption and efficiency metrics, water consumption, and waste recycling rates, all of which signal environmental impact.

On the social side, important metrics include workforce diversity (gender and ethnic diversity within the organisation, inclusivity indices), employee well-being (health and safety indicators, number of training hours), community contribution (CSR spending, volunteer hours) and ethical conduct (e.g., incidents of code-of-ethics violations, corruption risks). These KPIs measure how responsibly and sustainably the company operates, and how much it contributes to the welfare of the broader community.

The integration of the sustainability perspective into the scorecard reflects the view that long-term business success is inseparable from sustainability, and that the company must regularly measure and improve its own “people” and “planet” performance as well. Of course, the 4T model is also applied here:

●

●

●

●

As a result, sustainability performance becomes an integral part of the company’s strategic monitoring—not in a separate CSR report, but as part of the corporate governance dashboard. The 4T framework ensures that both sustainability risks (such as a potential environmental incident) and opportunities (such as green innovations) have predefined response plans.

Summary of HEX-BSCIn the system proposed here, the main indicators and metrics of the system were thus chosen along the above perspectives, covering several dozen measures in total. In the design, it is ensured that each metric aligns with a strategic objective and, where possible, is based on objective, measurable data.

An important methodological feature is that the HEX-BSC aligns with existing models without adopting them mechanically, but rather in an integrative way. The Balanced Scorecard perspectives provide the skeletal structure, which is then expanded (for example, the Learning and Growth perspective effectively splits into separate employee satisfaction and culture perspectives). The Denison model provides deeper insight into culture within the learning/growth domain, which is why culture is treated separately. Adding the sustainability dimension conforms to international trends, where environmental-social performance appears as the fifth column of the BSC. The incorporation of the 4T risk management framework can be likened to extending strategy maps with risk considerations or integrating Enterprise Risk Management (ERM) —the novelty here is that it explicitly names the possible responses (transfer, terminate, tolerate, treat) and displays them in every perspective. Methodologically, this sends the message that for any domain (whether finance or HR) multiple strategic responses to problems exist, and it is worthwhile to consider them during the planning phase.

In sum, the main innovation of the HEX-BSC system is its multidimensional integration: it does not treat the domains of finance, customer, human, process, culture, and sustainability as isolated factors, but brings them into a common framework, creating opportunities for causal linkages among them (for example, improving culture increases employee satisfaction, which improves customer experience, which in turn increases revenue—all in a sustainable manner). The methodology provides a clear system of metrics while remaining flexible: the weighting and target values of metrics can be customised to a given company’s strategy and the challenges of the environment.

Building on the comparative findings and the identified value added of the proposed HEX-BSC framework, the following section synthesizes the main insights and reflects on their broader implications for corporate performance management. The results highlight both the strengths and the practical considerations that must be addressed when implementing this extended, risk-aware scorecard in complex organisational settings. Accordingly, the next chapter presents the key conclusions and outlines future research and development directions.

Innovations and Added ValueThe greatest innovation of the presented HEX-BSC is its holistic approach, which integrates all essential aspects of corporate performance into a single framework. While the traditional Balanced Scorecard is limited to four perspectives, HEX-BSC encompasses six dimensions (Financial, External Customer, Internal Customer, Culture, Processes, Sustainability—plus risk management responses in every perspective). The added value lies in providing corporate management with a more comprehensive picture. For example, HEX-BSC allows managers not only to see that financial results are worsening, but immediately to investigate the causes in the other perspectives (unhappy customers? weak innovation? poor culture?), and through the risk management module to receive suggestions on how to intervene. The system synthesises the best of management theory—uniting strategic planning, operational control and risk management.

The main conceptual differences can be summarized as follows. Compared to traditional solutions, the HEX-BSC differs in several respects:

●

●

●

●

The HEX-BSC system is currently in a prototype or pilot phase. Based on preliminary feedback, the following potential benefits can be highlighted:

●

●

●

For validation, it is necessary to perform rigorous analysis over time. For example, a company implementing this evaluation system could be compared with control companies. In addition, internal validation of the system is important: for example, do the scorecard metrics correlate with actual financial results or other success indicators? One challenge of the integrated system is that it collects a huge amount of data—the task is to determine which among these are the best predictors of corporate success.

A recurring question in research on the Balanced Scorecard is whether an empirically verifiable causal link can be shown between scorecard use and improved performance. One forward-looking validation approach could involve simulations: for example, a stress test where an external shock hits the company (such as a drop in market demand) to see how well the system quickly identifies problems on all fronts and reacts with the 4T strategies.

Separation of External Effects and Process Improvement ImpactThe separation of external effects and process improvement impact raises an important measurement and analysis problem. When a company’s indicators improve, how can one determine whether this was caused by external factors (e.g., a booming economy, a competitor’s downturn) or by internal process improvements? The scientific approach to this question is to use controlled comparisons. For example, by incorporating industry benchmark data, one could compare the scorecard results to the industry average: if the company’s metrics improve more steeply than the industry trend, that points to internal initiatives. Furthermore, statistical methods (such as time-series analysis or regression) can be used to examine how much of the performance change is explained by external variables (e.g., GDP growth, market demand indices), with the remaining variance attributed to internal changes.

The scorecard system itself can assist in this separation by including lead and lag indicators [74]. For instance, improvements in process-perspective lead times (lead indicators) may precede improvements in financial results (lag indicators), so one can see in advance how an internal improvement affects the outcome, independently of the external environment. Similarly, when an external shock hits the company (e.g., a spike in raw material prices), it typically produces a distinct pattern in the indicators (first costs rise and profit falls, followed by other secondary effects), whereas an internal process improvement generates a different pattern (gradual, multi-area improvements).

With sufficient historical data, the system’s dataset would allow the use of analytical tools such as causal networks or structural equation modelling, with which the relationships between performance indicators can be mapped. In addition, the impact of 4T risk management actions can also be measured: for example, if in one quarter multiple ‘Terminate’ actions occur (e.g., the closure of a loss-making division), one could isolate their effect (perhaps a short-term revenue decline but cost savings, and longer-term improved profit margin) from external trends. Of course, this requires that the system records these actions and retrospectively assesses their outcomes—something that should be done as an action-based feedback supplement to the scorecard.

LimitationsWhile this study makes a conceptual contribution by proposing the HEX-BSC framework, its findings and implications should be interpreted in light of several limitations inherent to the chosen research design. The study follows a design science research logic, with the primary objective of developing and theoretically grounding a novel performance management artifact tailored to the energy sector. As a result, the paper does not aim to empirically test causal relationships or quantify performance impacts. Instead, the contribution lies in addressing structural gaps identified in existing sustainability-oriented Balanced Scorecard frameworks through a coherent conceptual design. Consequently, claims regarding organizational or financial performance improvements remain indicative and require empirical verification in future research.

The qualitative expert validation incorporated into the framework development provides initial insights into practical relevance and interpretability; however, this evaluation remains exploratory. The expert feedback was drawn from a limited number of senior professionals within the energy sector and reflects a specific institutional and regional context. While this supports the plausibility and managerial logic of the HEX-BSC, broader validation across different organizational settings, regulatory environments, and cultural contexts would be necessary to strengthen the generalizability of the findings. Further studies involving multi-case applications or longitudinal implementations could provide deeper insight into how the framework performs in practice over time.

The sector-specific focus of the HEX-BSC represents both a strength and a limitation. By explicitly addressing characteristics such as regulatory intensity, capital-intensive assets, long investment horizons, and sustainability constraints, the framework is well aligned with the strategic reality of energy companies. At the same time, this tailoring may limit the immediate transferability of the model to other industries without adaptation. Future research could therefore explore how the six-perspective, risk-integrated structure might be modified or simplified for use in sectors with different strategic and operational conditions.

Additionally, the integration of the 4T risk management logic into each scorecard perspective, while conceptually enhancing responsiveness and decision support, increases the overall complexity of the framework. Successful implementation would likely depend on organizational maturity in performance measurement, data availability, and managerial capabilities in risk governance. Similarly, the explicit separation of Internal Customer (employee-related) and Corporate Culture perspectives enables more nuanced diagnostics of human and cultural drivers, but it also raises challenges related to the measurement and interpretation of inherently qualitative constructs. Despite grounding the culture perspective in established theoretical models, consistent operationalization across organizations remains an area for further methodological refinement.

Taken together, these limitations suggest that the HEX-BSC should be understood as a theoretically robust and conceptually advanced framework rather than a fully empirically validated management system. Future research focusing on applied case studies, quantitative impact assessment, and digital tool-supported implementations would provide a natural next step in consolidating and extending the framework’s contribution.

Overall, the enhanced scorecard system (HEX-BSC) can better align with the strategic goals of a modern company and ensure more resilient operations. However, practical implementation and the gathering of empirical evidence are crucial to substantiate the real added value. Early experiences may be encouraging—especially for organisations that operate in complex environments and must perform on business, technological and sustainability fronts simultaneously. Further research may also examine digital implementations of the HEX-BSC through BI dashboards and data-driven monitoring environments.

This study introduced a corporate performance measurement system, the HEX-BSC, which is a consciously designed, innovative framework that combines the most contemporary elements of management theory in practice. The system addresses the challenges of traditional approaches: it is both balanced and extended in the directions of sustainability and culture, while also being dynamic through risk management integration. This new system reflects that a company’s success does not only rely on financial stability, customer-centricity and engaged employees but also on strong culture, efficient processes and sustainable operations.

The HEX-BSC’s holistic perspective ensures that management does not see these areas in isolation but rather in context. For example, the impact of a strategic decision can be tracked on all fronts: a new product launch becomes measurable not only in sales figures, but also in customer satisfaction, employee workload, process performance and sustainability indicators. This complete feedback—providing the full picture—is the basis of becoming a learning organisation, as the company can refine its strategy based on learning from its own operations.

Some practical recommendations can be formulated for other organisations:

●

●

●

●

●

The scientific examination of the HEX-BSC requires further research. Some suggested directions include:

●

●

●

From a design science research perspective, the HEX-BSC represents a theoretically grounded and practically interpretable artefact that contributes to the evolving field of sustainability-oriented performance management systems.

No data were generated from the study.

Conceptualization, IV; methodology, IV and MSC; writing—original draft preparation, IV; writing—review and editing, IV and MSC; supervision, MSC. All authors have read and agreed to the published version of the manuscript.

The authors declare that they have no conflicts of interest.

This study was funded by the Sustainable Development and Technologies National Programme of the Hungarian Academy of Sciences (FFT NP FTA).

1.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions