Location: Home >> Detail

J Sustain Res. 2024;6(1):e240005. https://doi.org/10.20900/jsr20240005

,

Olha Vysochan, Alla Yasinska

,

Olha Vysochan, Alla Yasinska

Department of Accounting and Analysis, Institute of Economics and Management, Lviv Polytechnic National University, Lviv 79013, Ukraine

* Correspondence: Vasyl Hyk.

The creation of theoretical and practical approaches to understanding the principles of accounting in a circular economy and sustainable development and the establishment of scientific foundations in this area is becoming increasingly important due to the growing information interest of stakeholders. This article contributes to bridging the gap between academic research focusing on accounting and business implementation of the circular economy. Based on this, it is important to present complete information about the current state and recent trends in publishing activity, which can be achieved through the use of bibliometric methods. The purpose of this study is to conduct a bibliometric analysis of the keywords “(Circular economy) AND (Accounting)” to visualize the scientific landscape. The search query for analysis was performed in the Scopus scientometric database between 2004–2021. Data selection was carried out according to the standard methodology using PRISMA in several stages: identification, screening, included and the information obtained was exported for processing into the computer program R (bibliometrics package). As a result, 934 publications were received, most of which are scientific articles. The analysis of publications over the years showed an increase in their number, which confirms the high level of interest among accountants and the importance of this topic. Based on the obtained data, it was possible to form tables, graphs and bibliometric maps, which allowed us to identify the leading scientists who study this topic, to establish countries, journals and main directions of research shortly. The originality of the conducted research is manifested in the fact that it should create a basic foundation and present a new idea about the role of accounting in the conditions of a circular economy of sustainable development. The article addresses the gaps in qualitative scientific research on this issue, and the given conclusions will help to expand the knowledge of researchers through an overview analysis of the results of the conducted research.

CE, circular economy; CCA, Coalitie Circulaire Accounting

The Global Goals, adopted by Member states of the United Nations in 2015 as a universal call to all countries, have formed the basis of United Nations policy and funding for the 2030 Agenda for Development. They are comprehensive and indivisible and balance the three dimensions of sustainable development: economic, social and environmental. Sustainable development and the concept of a circular economy based on the principles of reduction, reuse and utilization of energy, materials and waste is seen as a viable alternative development strategy to reduce the conflict between national economic development and environmental protection [1].

One of the indicators of sustainable development is the reduction of waste generation through recycling and reuse of resources. Accordingly, to achieve the goal of sustainable models of resource consumption and production, the current imperative is a circular economy, which should gradually replace the linear model, which is the basis for the economy of most countries [2]. The circular economy is restorative and closed; waste, materials, residues are reused, that is in contrast to the linear economy, the principle of “take, make, reuse” is applied. The circular economy is characterized by minimizing the consumption of primary raw materials and processed resources, reducing waste and disposal costs.

Since sustainable development and the circular economy are not only theoretical concepts but also practical, one of the key factors in this transformation is accounting [3].

Material flow accounting answers only a few questions, but concerns about the possibility of applying its theoretical foundations to the concept of sustainable development and the circular economy remain an open question [4]. Sustainability accounting requires companies to pay special attention to environmental, social and governance issues by disclosing non-financial information about activities and their results [5,6]. At the same time, the lack of guidelines, the difficulty of determining the number of indicators that reflect the state and dynamics of changes in the components of the natural and social environment, make it difficult for enterprises to introduce sustainable development accounting [7]. Accounting requires a systematic approach and providing internal and external users with new means to measure the performance of the enterprise in the context of sustainable development and circular economy at the organizational, sectoral, or national level. At the same time, accounting has an important informational value to help businesses move from a resource-based accounting concept to a function-based or life-cycle accounting. The study of the concept of sustainable development accounting can, in particular, contribute to the standardization and unification of financial and non-financial reporting of the company’s performance in the context of sustainable development and the circular economy, limiting the possibility of incomplete, incorrect, inaccurate, or redundant information. In practice, special attention is required to observe the quality characteristics of useful financial information, in particular relevance, materiality, and truthful presentation, which also affects the regulation of legal aspects of accounting and reporting. Thus, the relevance of the study of the impact of sustainable development and the circular economy on accounting is of particular importance.

Theoretical principles and practical aspects of the implementation of the circular economy in the context of sustainable development are actively studied in the works of scientists such as Abou Taleb et al. [8], Geissdoerfer et al. [9], Goyal et al. [10], Halog and Anieke [11], Manea et al. [12], Martinho and Mourão [13], Ruiz-Real et al. [14], Siryk et al. [15], Shpak et al. [16], Türkeli et al. [17] and many others.

Features of accounting in terms of sustainable development and circular economy are considered by the following scientists: Di Vaio et al. [18], Gusc [19], Hyk et al. [20], Larrinaga and Garcia-Torea [21], Nadeem et al. [22], Scarpellini et al. [23], Vegera et al. [24], Vysochan et al. [25], Wang et al. [26], Zyznarska-Dworczak [27] and others.

Thus, Larrinaga and Garcia-Torea [21] considered the problems of modern concepts of circular economy and COVID-19 in terms of sustainability and studied the critique of accounting interventions in both areas. A crucial element of this critique is the deep interaction with ecology, biology and earth science. Scarpellini et al. [23] identified and measured the environmental opportunities that apply when a circular economy is implemented in enterprises. Vegera et al. [24] investigated the problematic issues of determining the technological cycle of the stage of industrial waste and identifying the objects of accounting that arise at these stages for further development of recommendations. Nadeem et al. [22] identified factors and barriers to the transition from current linear business models to a circular economy, considering macro-, meso-, and micro-levels, including the role of accountant interventions and the need to improve accounting.

Some scholars have focused on the problematic issues of displaying information about the processes occurring in the circular economy. In particular, Wang et al. [26] investigated the quality of circular economy accounting disclosure and conducted an empirical analysis of the relationship between the quality of circular economy accounting disclosure and corporate property management and institutional pressure according to institutional theory and corporate governance theory. A study by Di Vaio et al. [18] aims, among other things, to answer the question “what is the role of accounting and reporting for the circular economy and waste?”.

Individual scientists-accountants give in their scientific works various proposals for the development of accounting. Thus, Gusc [19], researching on improving the accounting to ensure the principles of the circular economy, focuses on the following aspects: improving reporting by the needs of the circular economy; determining the value of products (works, services) in the circular economy; change of accounting methods for the needs of the circular economy.

Zyznarska-Dworczak [27] offers an author’s concept of sustainable development accounting, which is based on positive and normative theories of accounting. According to the author, accounting theories not only help to formulate new concepts, methods and models, but also can explain new phenomena that arise in practice. The theoretical approach is the basis for studying the features and prospects of accounting in any direction (Industry 4.0 and 5.0, digitalization, circular economy), as such an approach covers scientific, practical, functional, informational, political, legal, ethical, social and many other components.

Scarpellini et al. [23] investigated whether the circular scope of business, which is related to the degree of development of their capabilities, affects environmental and financial performance. The results indicate a positive relationship between firms’ circular scope, their environmental accounting practices, and the level of corporate social responsibility (CSR) and accountability.

Organizations and institutions are also actively involved in solving the outlined problem. For example, in 2019 Circle Economy and the NBA (Royal Netherlands Institute of Chartered Accountants) together with such institutions as KPMG, Rabobank, Impact Center Erasmus and Sustainable Finance Lab and others joined forces to form the Coalitie Circulaire Accounting (CCA) [28]. Through case studies, the group develops guidelines to help businesses adapt to circular design.

Thus, it can be stated that accounting issues in the conditions of a circular economy of sustainable development are becoming more and more relevant. Without diminishing the value of scientific achievements of scientists, we note that the complexity of the accounting process in terms of sustainable development and circular economy raises the question of further research. Summarizing the existing approaches to accounting to ensure the principles of the circular economy, it should be noted that this area of research is relatively new, and therefore requires additional research.

For a thorough study, we used a bibliometric analysis of scientific works on the development of the circular economy. Bibliometrics is a quantitative method of research analysis that uses publications as an indicator to evaluate research. Such metrics are widely used in the quantitative approach to research evaluation [29]. The objects of study in the bibliometric analysis of science are publications grouped by different characteristics (document flow segments, microflows): authors, journals, thematic sections, countries, etc. This method is used, firstly, to analyze the effectiveness of scientific research, and secondly, to map research. The direction of the performance analysis consists in establishing the most researched works that made a significant contribution to the topic in terms of keywords, researchers, etc. Mapping makes it possible to visually present the results of the work, to examine the authors’ work in a retrospective aspect, and to establish directions for future research.

It is worth noting that literature reviews on the use of the bibliometric method were used in some studies [30–32], but we did not find articles that directly related to accounting in the context of the circular economy of sustainable development. Therefore, we believe that this article will help to eliminate gaps in scientific research on this issue. Thus, the article aims to analyze the concept of circular economy and identify the presence of an accounting component in its structure in terms of sustainable development.

According to the goal, the key task (RQ) of the research was formed, which consists of determining the total number of publications, establishing the keywords that are used most often, determining the most authoritative authors, and international cooperation on the subject of accounting in the conditions of a circular economy of sustainable development.

This paper uses a systematic review of the literature using bibliometric methods. Bibliometrics is the use of mathematical and statistical methods to study the flow of scientific documents (books, periodicals, etc.) to identify trends in the subject areas, features of authorship and the mutual influence of publications [33]. The analysis in this study was performed using the open-source bibliometrics R program [34]. The choice of this particular software product was not accidental, since R (bibliometrix package) is considered a universal tool for conducting quantitative research in scientometrics and bibliometrics, which includes all the main bibliometric methods of analysis [34]. It has been widely used in similar studies [35]. In the R program, the total conceptual structure is worked out with the help of the Multiple Correspondence Analysis (MCA) and K-means clustering methods, which have been successfully used in past our research [36,20].

For research efficiency, citation analysis includes a wide range of methods for reviewing bibliometric data, including keyword frequency analysis, citation analysis, and article counts by country, university, author, and journal [37]. The assessment of research performance is measured quantitatively and qualitatively using the FCC contribution indicator [38]. Another plane of bibliometric analysis is scientific mapping, which provides a new perspective on FCC by revealing scientific boundaries and dynamic structures of the research field through visualization techniques [39].

Material Collection and SelectionIn this study, we used the Scopus database for scientific research and obtaining bibliometric data. Its choice over other databases is justified by the fact that it is considered the most authoritative database worldwide, as it includes a wide range of publications from different disciplines and fields of research [40].

In the research, we considered various types of publications, not only articles, but also reviews, conference proceedings, editorial notes, book chapters, book reviews, extended theses, and others. The selection of articles was based on two exclusion criteria and one inclusion criterion [35,41]. According to the first exclusion criterion, the authors reread the abstracts, which selected those related to the topic. According to the second criterion all articles were screened to ensure their relevance and suitability. Materials that were not directly related to the research topic were removed. Finally, the inclusion criterion refers to the integration of contributions that were not found through the research line and/or included in the selected academic database, but have been cited in the FCC literature [39,42–47].

The search query in the Scopus scientometric database was conducted using the terms “Circular economy” and “Accounting” in the title, abstract and keywords. The scope was narrowed to the scientific field of “Business, Management and Accounting” and in the period between 2004–2021. Accordingly, the following parameters (filters) were set for searching the database:

TITLE-ABS-KEY (circular AND economy) AND TITLE-ABS-KEY (accounting) AND PUBYEAR > 2004 AND PUBYEAR < 2021.

The content was selected and analyzed on January 27, 2022, as a result of which the data was obtained using the “Data Export” function and are in the data set.

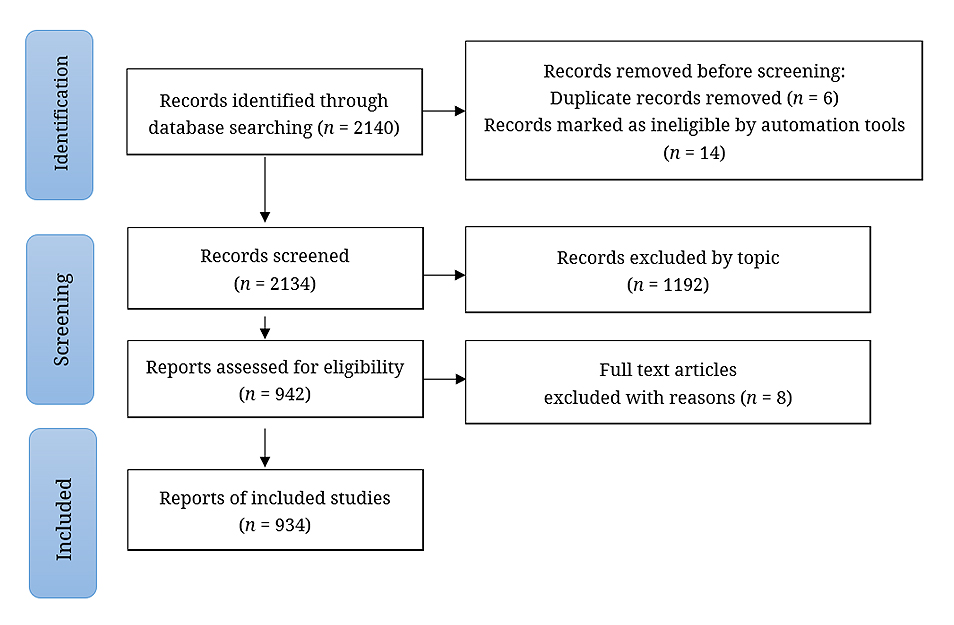

The document selection scheme using PRISMA was carried out as follows (Figure 1):

Figure 1. PRISMA 2020 diagram (Adapted from [48]).

Figure 1. PRISMA 2020 diagram (Adapted from [48]).

The obtained file data was downloaded to the universal software R (bibliometrics package). Bibliometrics is open-source software written in R that is widely used by scientometrists to analyze and visualize bibliometric data [49].

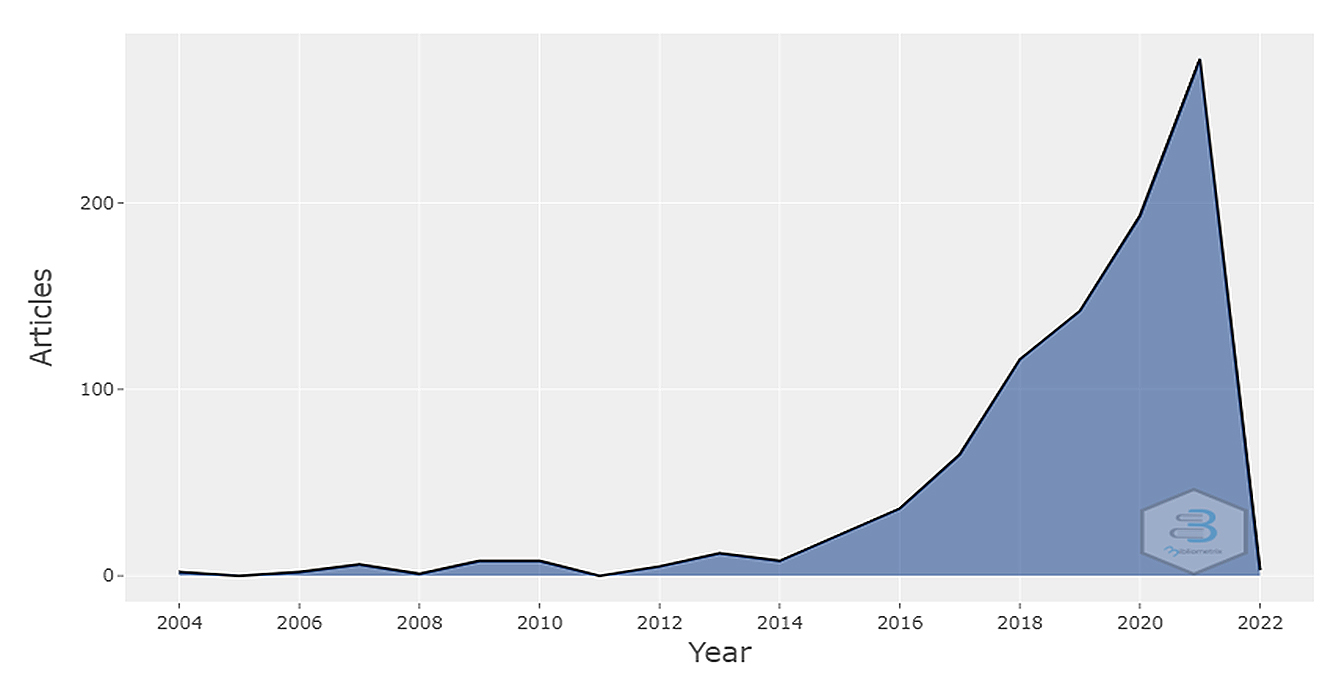

As a result of the content analysis for 2004–2021, 934 publications were found for the following types of documents: articles—775, proceedings papers—136, book chapters—12, editorial materials—7, data papers—3 and corrections—1. Generalized data on the number of publications are shown in Figure 2.

Figure 2. Annual scientific production. Source: formed by the authors using R software.

Figure 2. Annual scientific production. Source: formed by the authors using R software.

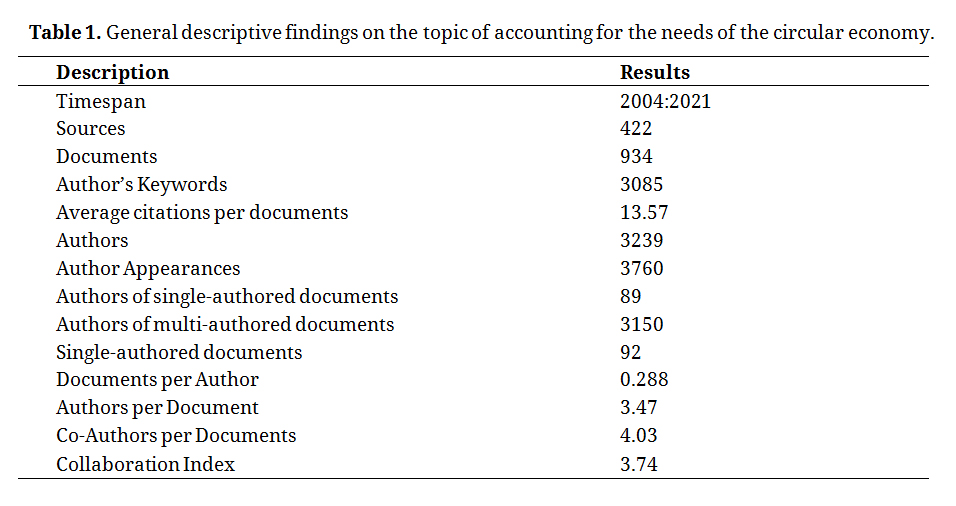

According to the data presented in Figure 2, the total cost of research papers on the needs of the circular economy is growing every year, indicating this study's relevance. A special increase was observed since 2018 when the number of articles exceeded the mark of 100 units, and at the end of 2021 approached 300 units. We also consider it necessary to provide basic information about the results of the study, which is given in the Table 1.

From the Table 1 shows that during the analyzed period 3239 authors met 3760 times on the topic of accounting for the needs of the circular economy. We also found that the authors published 934 publications in 422 different sources (journals, conference proceedings, books, etc.). There is a fairly large volume of references—13.57 citations per publication. The average number of citations per article is calculated by dividing the total number of citations by the total number of articles and can be a very useful indicator for estimating the average impact of a journal or author. With most publications (97.25%) published by several authors. Literary studies accounted for 3.47 authors per publication, and the total number of authors in these studies was 4.03. An important relative indicator in the bibliometric analysis is the value of the Collaboration Index (taking into account the average number of authors in several authors’ publications), which in our case was 3.74. It was also found that the number of publications per author was 0.288.

Table 1. General descriptive findings on the topic of accounting for the needs of the circular economy.

Table 1. General descriptive findings on the topic of accounting for the needs of the circular economy.

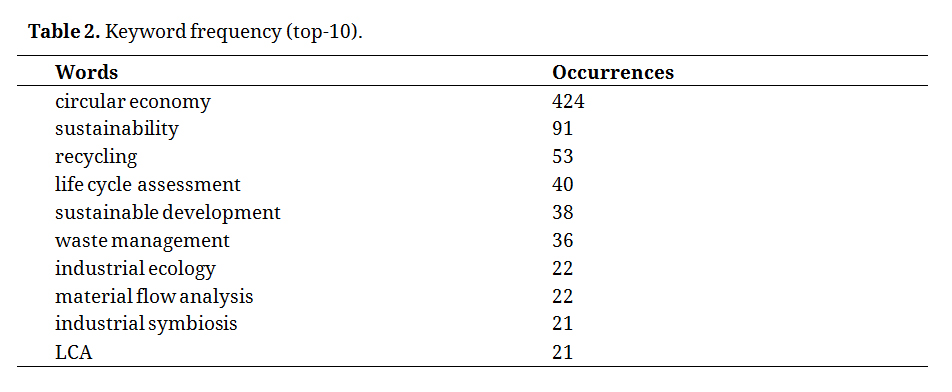

Quantitative analysis by keywords was conducted to establish the main research topics. As a result, we determined how often the authors used certain concepts (Table 2).

Table 2. Keyword frequency (top-10).

Table 2. Keyword frequency (top-10).

This analysis was conducted to establish the use of concepts (common words) by scientists-accountants in scientific publications. The visual results of the obtained integration circuits are shown in Figure 3.

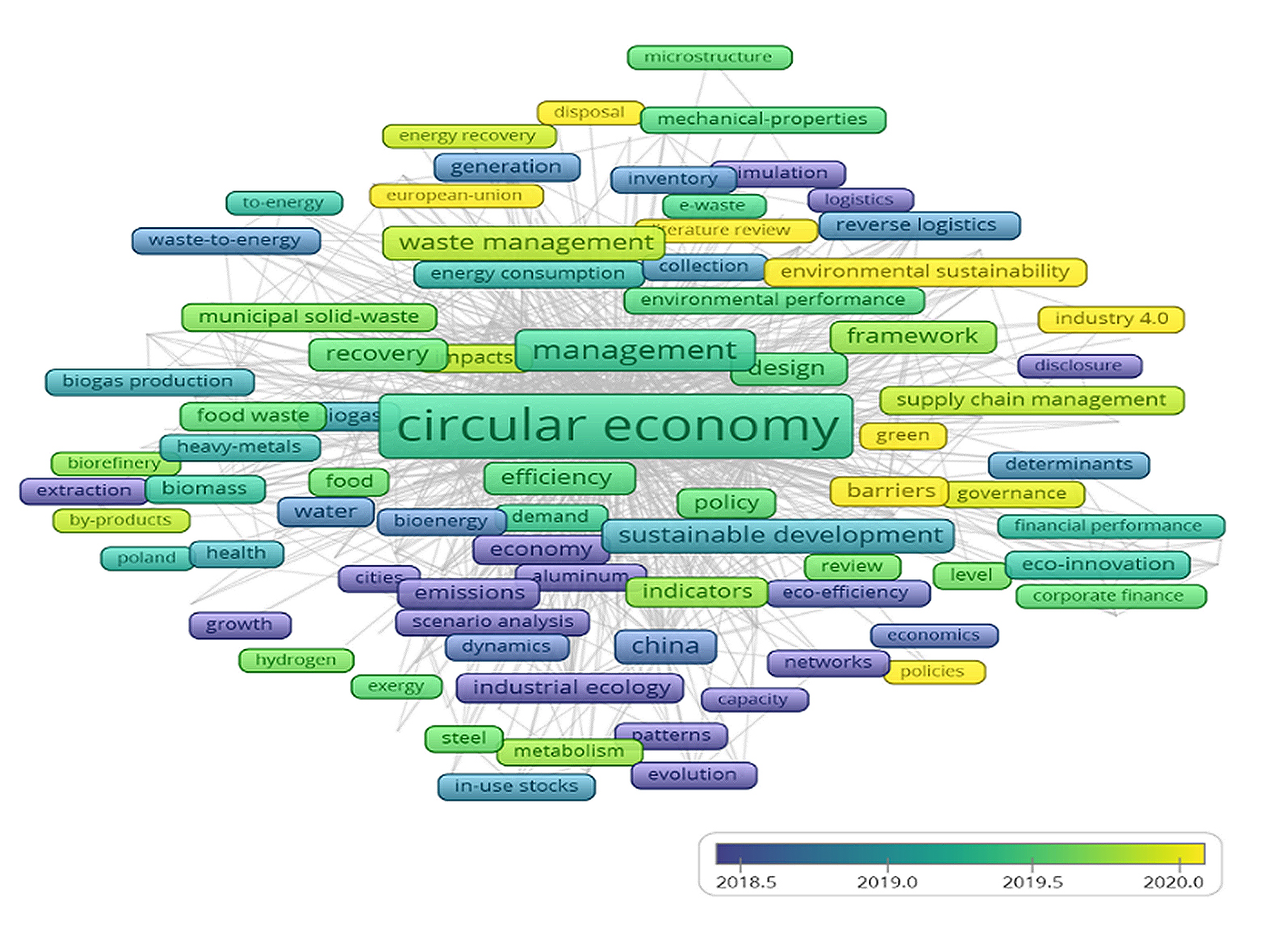

Figure 3. Visualised map by frequency of mention of words on the topic of accounting for the needs of the circular economy. Source: formed by the authors using R software.

Figure 3. Visualised map by frequency of mention of words on the topic of accounting for the needs of the circular economy. Source: formed by the authors using R software.

The larger the font of the highlighted word, the more often it is used, and the standard colour indicates the cluster. Also, as shown in Figure 3, the connections between words are connected by nodes [50]. According to the obtained data of Figure 3 it can be stated that research in the field of accounting for the circular economy in recent years is associated with the study of sustainable economic development, life cycle assessment, environmental and economic indicators, energy saving, energy efficiency, bioeconomics, waste management processes and etc.

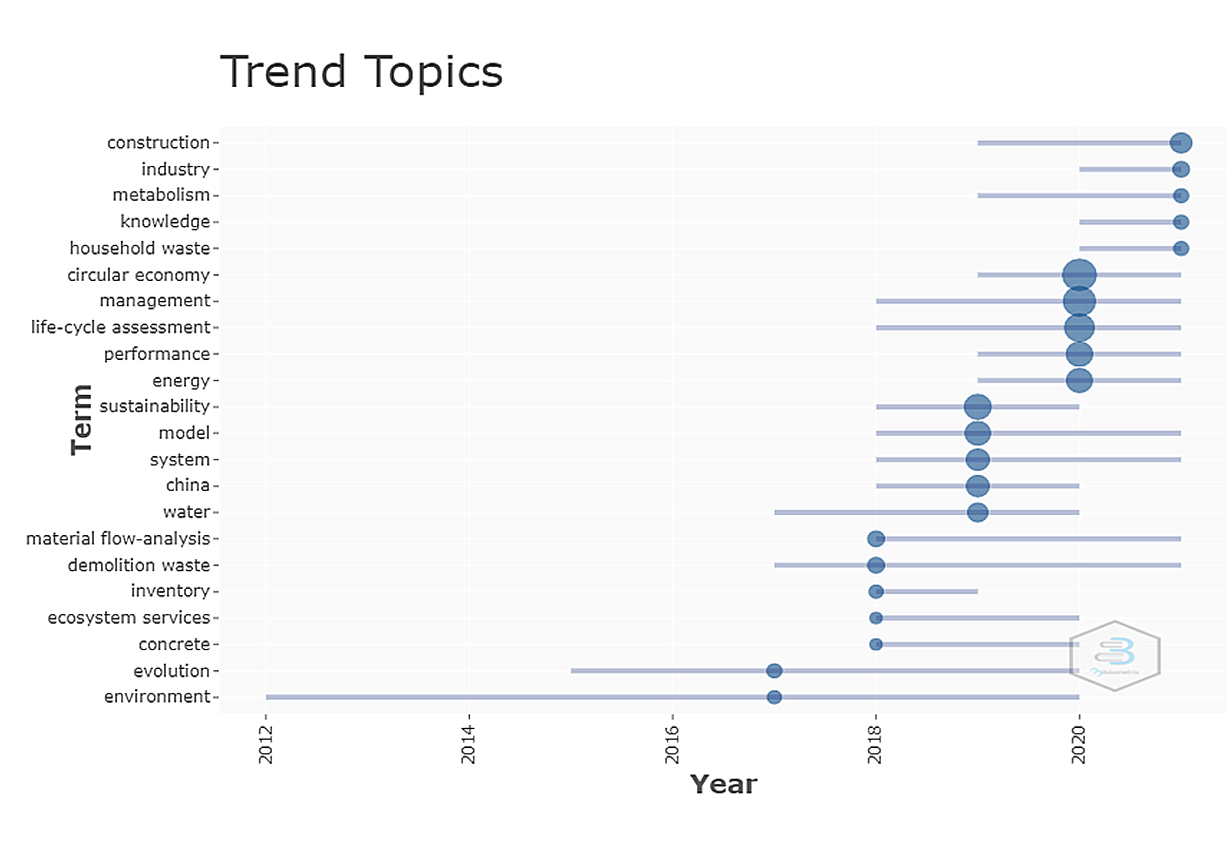

The frequency of keyword use is important and makes it possible to follow trends over the years. Figure 4 shows which trend themes (words) were used by the authors in terms of years.

Figure 4. Trend topic of accounting for the needs of the circular economy. Source: formed by the authors using R software.

Figure 4. Trend topic of accounting for the needs of the circular economy. Source: formed by the authors using R software.

The use of keyword selection by filter (Word Minimum Frequency = 5, Number of Words per Year = 5) made it possible to observe trends in this topic during the analyzed period. Within the selected range of keywords, it was noted that research topics such as circular economy, management, life-cycle assessment, performance and energy remained important. In addition, research topics such as household waste, industry and metabolism are popular in recent years. Analysis of the number of references makes it possible to establish the most cited works of authors on this topic (Table 3).

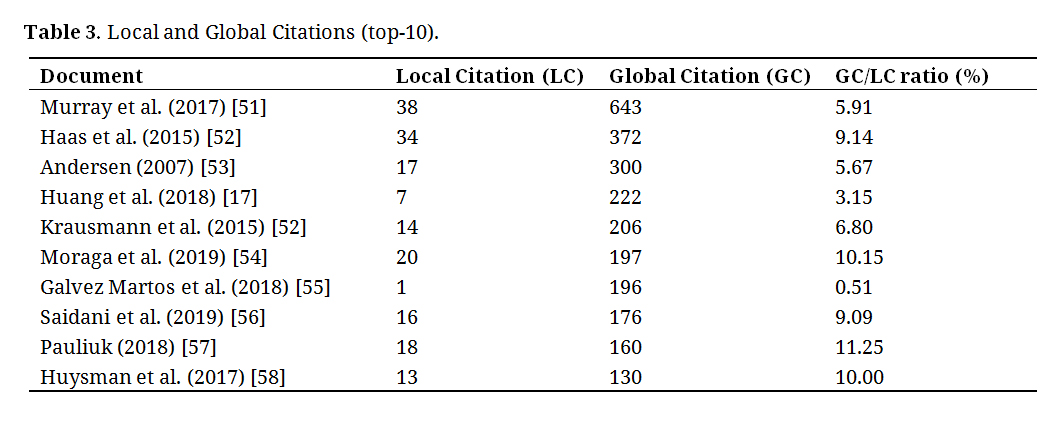

Table 3. Local and Global Citations (top-10).

Table 3. Local and Global Citations (top-10).

In the Table 3 shows the number of citations within the study, the number of citations from all disciplines and calculated the GC/LC ratio (%). The works of Murray et al. [51] and Haas et al. [52] differ significantly from other studies in Local Citation (LC) and Global Citation (GC). However, according to the GC/LC indicator, which demonstrates that the article receives citations outside the study of the topic, the situation is somewhat different: the works of Pauliuk [57], Moraga et al. [54] and Huysman et al. [58] are more cited, and their values are greater than 10.00%.

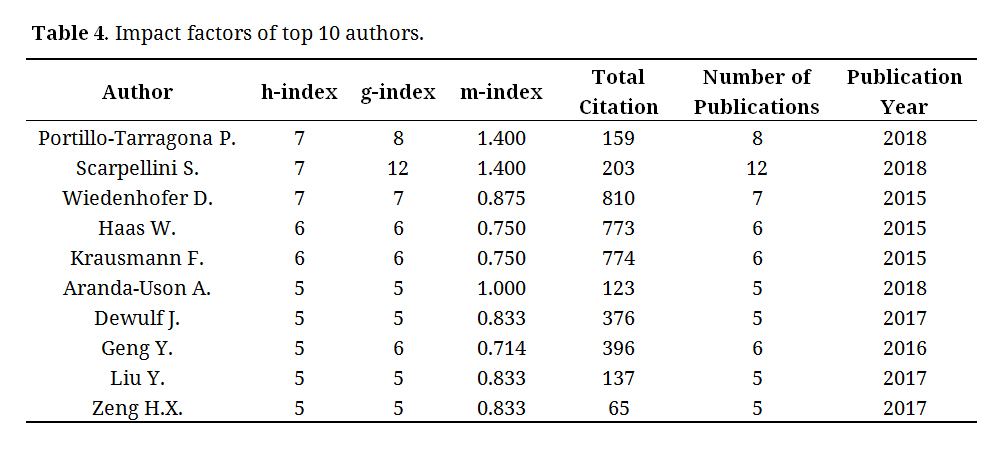

Findings for AuthorsOne of the key indicators widely used around the world to evaluate the work of researchers and research teams in the citation index. The values of the impact factor (IF) of the authors on the subject are given in the Table 4.

As can be seen from the Table 4 most cited authors on the h-index, which is one of the most important quantitative characteristics of a scientist’s productivity, are Portillo-Tarragona P. (n = 7), Scarpellini S. (n = 7) and Wiedenhofer D. (n = 7). They also have the largest number of publications. It is worth noting that all these publications were published relatively recently between 2015 and 2018, but have already received a large number of citations. Wiedenhofer D. (n = 810), Krausmann F. (n = 774) and Haas W. (n = 773) have the largest number of citations among scientists.

Table 4. Impact factors of top 10 authors.

Table 4. Impact factors of top 10 authors.

It should be noted that the above-mentioned authors paid the main attention in their works to the problematic issues of expanding financial accounting, taking into account information covering environmental, social, and economic impact, preparing reports on the company’s interaction with society and the natural environment, and disclosing financial and non-financial information about the results of activities about society and the environment. According to the results of scientific research, it can be stated that their authors mainly associated the development of the concept of accounting in the conditions of a circular economy of sustainable development with the establishment of the role of accounting in ensuring sustainable development, improving the preparation and submission of reports, and disclosing information about the environment for decision-making.

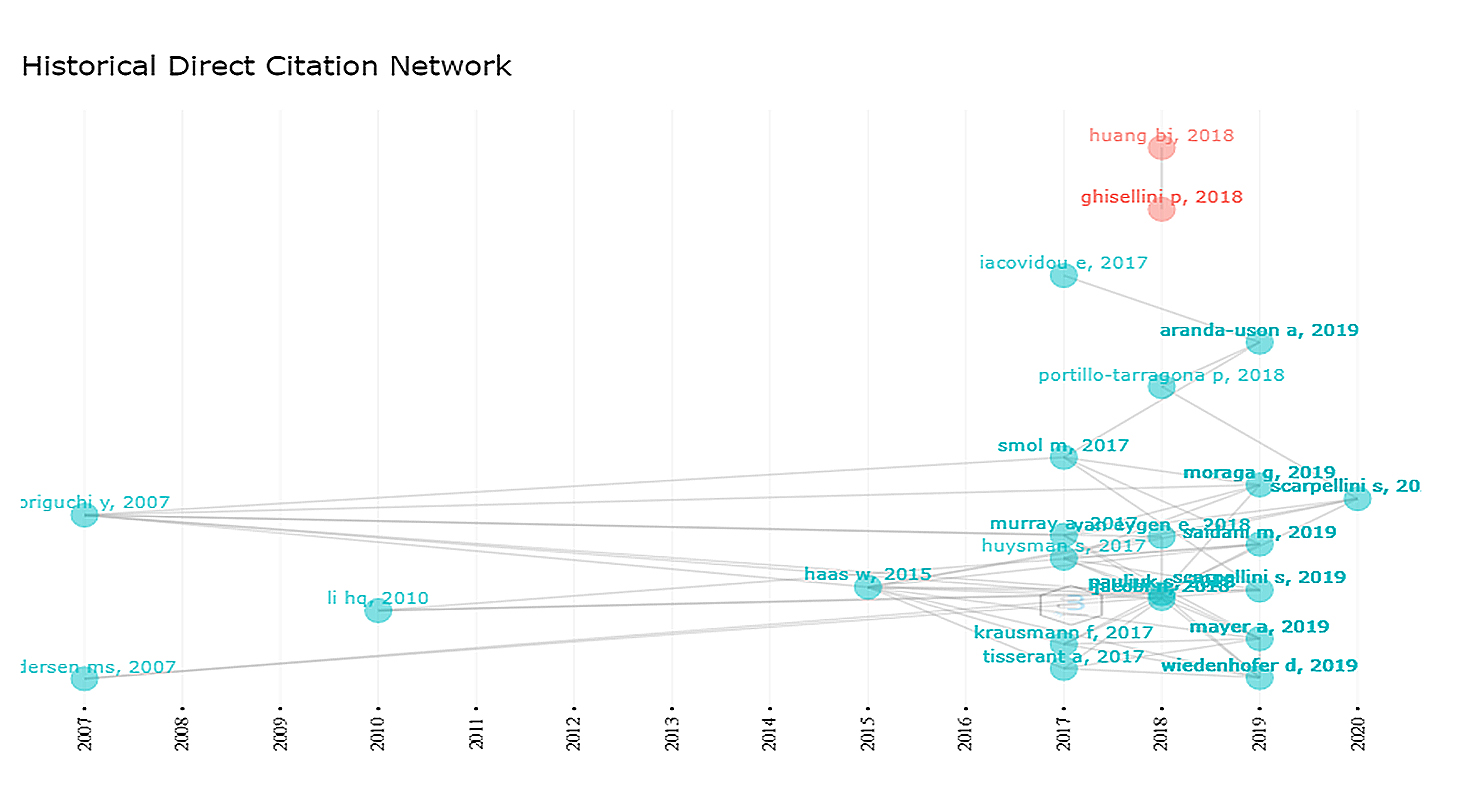

Although the importance of the impact factor gives a general idea of the authors, their important influence on the development of current issues, it should be recognized that this indicator is not enough. Accordingly, the level of influence of the authors in the historical period can be done using the indicator Historical Direct Citation (Figure 5).

Figure 5. Historical direct citation. Source: formed by the authors using R software.

Figure 5. Historical direct citation. Source: formed by the authors using R software.

From Figure 5 shows that Andersen [53], Moriguchi [59] and Li et al. [60] were the first published scientific papers in this field and after a significant number of years remained fundamental (supporting) because they lead to lines on the citation map. Visualization of the research network of the scientific landscape from a historical perspective also revealed the regularities of citations between scientists in the field of research.

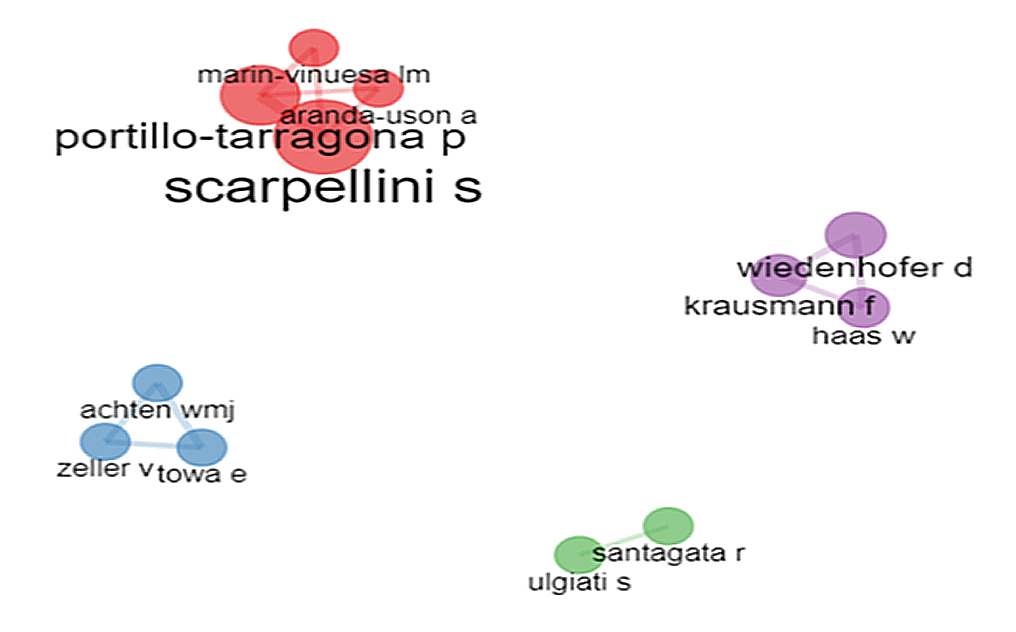

Findings for CollaborationsThe analysis of cooperation between authors provides an opportunity to establish links between the institutions of these authors and cooperation between countries. Nodes with several connections were taken into account when forming the cooperation network, and inefficient nodes were not taken into account. As a result of network analysis, a matrix of frequencies and adjacencies will be formed (Figure 6).

Figure 6. Collaboration networks for authors. Source: formed by the authors using R software.

Figure 6. Collaboration networks for authors. Source: formed by the authors using R software.

Thus, the network map was visualized and consisted of 12 authors divided into 4 clusters. Association was used by the normalization method, and Leuven’s algorithm was used for clustering. The largest and impact is the red cluster, which includes representatives of the University of Zaragoza (Spain): Pilar Portillo-Tarragona and Sabina Scarpellini. Slightly smaller purple cluster, presented by scientists from the University of Natural Resources and Life Sciences (Austria): Dominik Wiedenhofer, Willi Haas and Fridolin Krausmann. The other two blue and green clusters, which are approximately the same size, are represented by scientists from different countries and educational institutions, namely: Vanessa Zeller, Edgar Towa, Wouter Achten M.J.; Remo Santagata, Sergio Ulgiati.

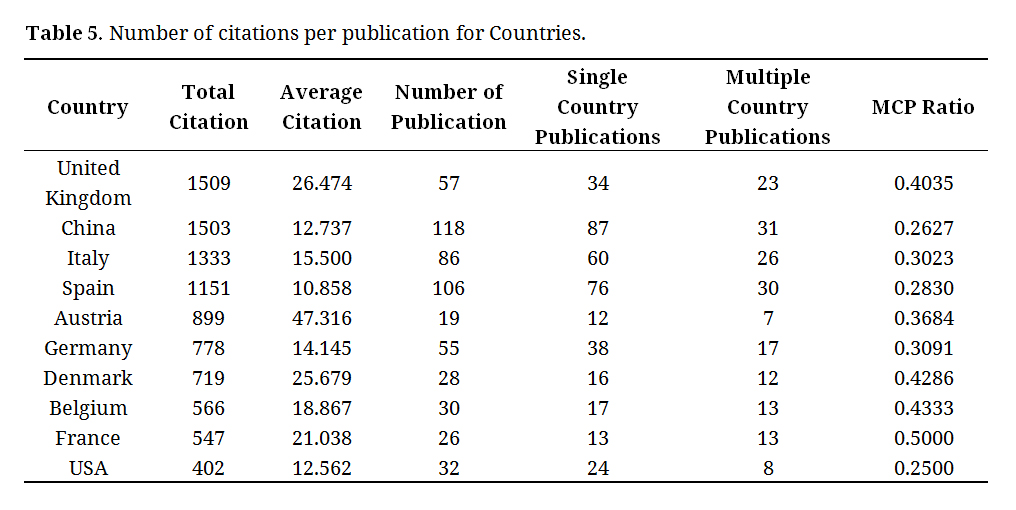

To carry out bibliometric analysis, it is important to study publications on the subject in different countries. Quantitative results of citations of authors by country are given in the Table 5.

Table 5. Number of citations per publication for Countries.

Table 5. Number of citations per publication for Countries.

From the data given in the Table 5 shows that the total number of citations stands out in 4 countries: the United Kingdom (1509), China (1503), Italy (1333) and Spain (1151). If we talk about the Average Citation, then we should highlight Austria (47.316), the United Kingdom (26.474) and Denmark (25.679). China (118) and Spain (106) had the largest number of publications on the topic. The MCP Ratio, which takes into account the collaboration of authors from one or more countries, is highest in France (0.5000), Belgium (0.4333) and Denmark (0.4286).

Based on this, a visual network of cooperation between countries on this topic was formed (Figure 7).

Figure 7. A map of scientific publications on accounting for the needs of the circular economy in the context of the world. Source: formed by the authors using R software.

Figure 7. A map of scientific publications on accounting for the needs of the circular economy in the context of the world. Source: formed by the authors using R software.

The volume of scientific publications of each oceanic country affects the size of the node. We were able to identify the countries in which accountants were able to make the greatest contribution to this topic. From Figure 7 it is clear that the red cluster is dominated by China, the sky-blue cluster by Spain, the purple cluster by the United Kingdom (England), and the green cluster by Italy.

Therefore, in our opinion, improving communications to stimulate collaborations between authors, countries, and institutions in the system of scientific research is an important task aimed at increasing the efficiency of the scientific process, stimulating cooperation between researchers, improving the dissemination of scientific knowledge and ensuring more successful implementation of scientific achievements in practice. It is effective cooperation that allows you to combine knowledge and a practical component to achieve common scientific goals and solve complex accounting problems in the conditions of a circular economy of sustainable development.

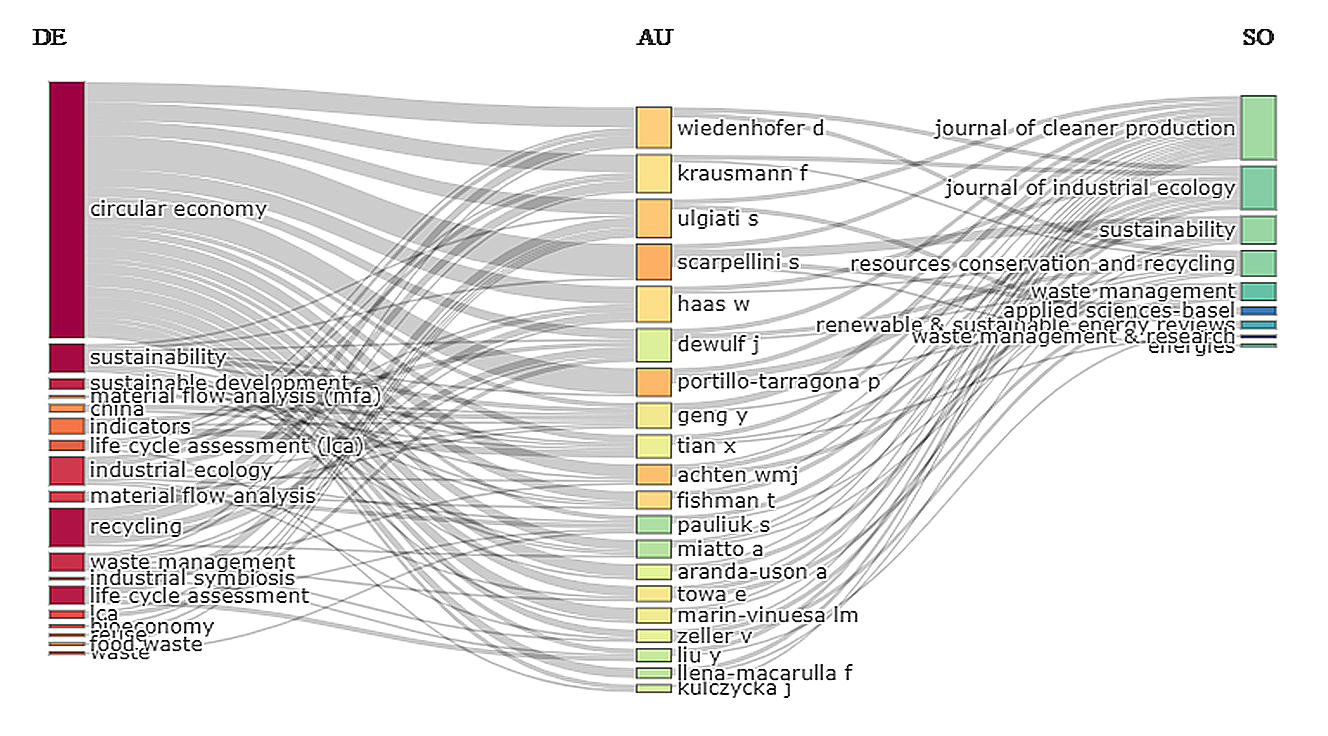

Sankey Diagrams: Three Field PlotsSankey diagrams are traditionally used to represent information in multiple networks and procedures. The formation of the Three-fields plot makes it possible to establish the flow of connections between various features (authors, journals, thematic headings, countries, etc.) [61]. The analysis of the social network of communication between keywords, authors and journals in this field is shown in Figure 8.

Figure 8. Three-fields plot (keywords-authors-source). Source: formed by the authors using R software.

Figure 8. Three-fields plot (keywords-authors-source). Source: formed by the authors using R software.

In Figure 8 shows a rectangular diagram used to represent the corresponding elements in different colours about the relationship between the keyword (left), author (middle) and source (right). The analysis found that scholars such as Wiedenhofer D., Krausmann F., Ulgiaty S., Scarpellini S. and Haas W. mainly used the following keywords: circular economy, sustainability, sustainable development and published in high-ranking journals: Journal of Cleaner Production, Journal of Industrial Ecology and Sustainability (Switzerland).

This article analyzes the latest trends, the current state of publishing activity and priority areas of research in the field of accounting for the needs of the circular economy in terms of sustainable development. Bibliometric analysis was performed using the program R package “bibliometrics” in the subject field for 2004–2021. In this study, the selection was conducted by key field (Circular economy) AND (Accounting) in the title, abstract or keywords. The study revealed 934 publications, including: articles—775, proceedings papers—136, book chapters—12, editorial materials—7, data papers—3 and corrections—1.

Publication activity has increased significantly in recent years and shows a scientific interest in this topic. A total of 3239 authors met in publications 3760 times and published 934 articles. It is also possible to emphasize the value of the indicator average citations per document, which was 13.57 and indicates the high quality of research. Most of the articles have been co-authored and suggest that the authors have often collaborated to make an even greater contribution to the development of the problem area.

It was found that the largest share in the total number of publications were articles that researchers tried to publish in prestigious journals of high level and impact factor. Trends among keywords indicate that in lately, issues related to the study of sustainable economic development, life cycle assessment, environmental and economic indicators, energy saving, energy efficiency, bioeconomics, waste management processes, etc. have received special attention. There are prerequisites that this trend will continue for future periods.

It was found that the articles Andersen (2007) [53], Moriguchi (2007) [59] and Li et al. (2010) [60] despite a large number of years remained fundamental. According to Local Citation (LC) and Global Citation (GC) research by Murray et al. (2017) [51] and Haas et al. (2015) [52] differ significantly from other studies. Wiedenhofer D. (n = 810), Krausmann F. (n = 774) and Haas W. (n = 773) have the largest number of citations among scientists.

As a result of the analysis of cooperation between the authors, 4 clusters were obtained: red cluster (Pilar Portillo-Tarragona, Sabina Scarpellini), purple cluster (Dominik Wiedenhofer, Willi Haas and Fridolin Krausmann), blue cluster (Vanessa Zeller, Edgar Towa, Wouter Achten M.J.) green cluster (Remo Santagata, Sergio Ulgiati).

Geographically, the countries which produced the most articles: were China, Spain and Italy, while the number of citations was slightly different: United Kingdom, China, Italy and Spain. The magazine in which the authors published their articles were also identified—the Journal of Cleaner Production, and the Journal of Industrial Ecology and Sustainability (Switzerland).

The most difficult challenge for the development of accounting in the conditions of a circular economy of sustainable development is the combination of economic, ecological, and social results, as well as established, established principles of accounting and reporting and ensuring their reliability. The results of this study are intended to help and facilitate scientists to better understand the current state and development prospects for scientific research on the topic of accounting in the conditions of a circular economy of sustainable development. Nevertheless, the elaborated scientific sources and generalized conclusions presented in this article provide scientists with a better vision of the topic and make it more understandable and open. In the future, researchers will be able to focus on problematic issues for deeper and more detailed research in this field. In addition, the originality and usefulness of this study lie in the fact that it provides an opportunity to summarize and generalize the scientific output on the topic during previous periods, enabling other scholars to use the results as a starting point for their research.

In conclusion, it can be noted that the scientific literature is still insufficiently considering the development of accounting in the transition from linear to the circular economy, taking into account economic, environmental and social aspects of sustainable development. Given the assessment of the current state of scientific support of the circular economy and the need to implement EGD (European Green Deal), a promising area of research is the development of accounting software for the circular digital economy, which will promote sustainable development.

The dataset of the study is available from the authors upon reasonable request.

OSV, VH—methodology; OSV, VH, AY, OOV—formal analysis, review and editing; OSV, VH, AY—conceptualization, original draft preparation.

The authors declare that there is no conflict of interest.

This study was conducted on 2 scientific topics: “Accounting in the context of sustainable economic development” (code of R&D work—OA-16) and “Formation and distribution of information flows between the subjects of the accounting system of the enterprise” (code of R&D work—OA-20).

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

Vysochan O, Hyk V, Vysochan O, Yasinska A. Accounting in the Context of a Circular Economy for Sustainable Development: A Systematic Network Study. J Sustain Res. 2024;6(1):e240005. https://doi.org/10.20900/jsr20240005

Copyright © 2023 Hapres Co., Ltd. Privacy Policy | Terms and Conditions