Location: Home >> Detail

J Sustain Res. 2025;7(4):e250069. https://doi.org/10.20900/jsr20250069

,

Timo Gerres 2 ,

Anna-Joy Kuehlwein 3

,

Timo Gerres 2 ,

Anna-Joy Kuehlwein 3

1 Facultad de Ciencias Económicas y Empresariales, Universidad Pontificia Comillas, Madrid 28015, Spain

2 Instituto de Investigación Tecnológica, Universidad Pontificia Comillas, Madrid 28015, Spain

3 Independent Financial Advisor & ESG Analyst, Stuttgart 70049, Germany

* Correspondence: Elisa Aracil

Truly sustainable firms have the potential to drive transformative change for the planet and society. This article operationalizes the true sustainability concept by offering an evaluative framework for its assessment. Building on signaling theory, our framework assesses true sustainability by integrating environmental performance and targets, providing a holistic perspective. Applying this framework to 12,312 global observations from leading, highly polluting industries in steel, cement, and aluminium, we identify selective environmental achievements and targets centered primarily on greenhouse gas emissions, overlooking broader environmental themes. Moreover, most producers set distant environmental targets (2050 or beyond), lacking interim milestones or alignment with prior environmental achievements, thereby compromising target feasibility and future orientation towards true sustainability. The framework is applicable across sectors, geographical contexts, and time frames, offering value to transition finance providers, socially responsible investors, and managers aiming to foster true sustainability advancements and manage the green transition.

The pursuit of environmental solutions is a paramount corporate priority [1,2], further intensified from 2015 onwards with the adoption of the Paris Agreement and the Sustainable Development Goals [3]. However, the discrepancy between companies’ positive environmental claims and effective environmental deterioration questions the existence of truly sustainable organizations [4,5]. A truly sustainable firm ‘shifts its perspective from seeking to minimize its negative impacts to understanding how it can create a significant positive impact in critical and relevant areas for society and the planet’ [4]. True sustainability thus implies transformational commitment [6–8]. This means that corporate sustainability initiatives that fail to induce fundamental macro-level changes can be understood as weak sustainability as opposed to strong sustainability which drives systemic transformation [9]. Becoming a truly sustainable firm demands a “transformational” approach [8,10], with a clearly defined agenda that sets specific targets and is shared with all stakeholders [6].

Evaluating progress toward true sustainability depends on firms’ reporting capability and achievements [11]. Abundant literature exists on the truthiness of reported information, that is, on firms’ integrity and opportunistic behavior through symbolic disclosure and impression management [12–16]. However, assessing true sustainability progress based on nonfinancial information is complex and remains little researched. True sustainability evaluations are particularly critical to firms lagging in sustainability performance, as their access to funding, especially transition finance, may be jeopardized without clear indicators of future sustainability potential. Transition finance, according to the EU Taxonomy (2020), supports high-emission industries that are on a pathway to significantly reduce their carbon footprint [17]. In response to this challenge, we propose a framework that operationalizes the true sustainability notion by developing a structured evaluation of its two pillars, i.e., firms’ sustainability performance and targets.

Signalling theory [18] provides a suitable lens. Signals arise in situations of asymmetric information where the sender (firm) holds insider information about a relevant condition (true sustainability) which is communicated through a signal (environmental reports). However, identifying true sustainability progress based on these ‘raw’ signals from public disclosure can be challenging. Non-financial information guidelines (i.e., EU Non-Financial Reporting Directive, CSRD—2022/2464/EU) offer significant insights into corporate sustainability action, yet, companies retain considerable discretion on the quality and quantity of information reported. To fully leverage this information, it is essential to establish a framework that benchmarks and evaluates companies’ progress toward true sustainability [19], testing their sustainability performance and targets against peers.

Prior research on sustainability signals has developed scoring methods as external validation [20–24]. However, these methods overlook selective efforts in sustainability performance and targets. This academic vacuum at the corporate level is remarkable, especially compared to the growing literature on SDG prioritization at the country level [25]. Besides, existing literature on environmental targets focuses on regions or products [11,26], but it is still embryonic regarding overall firms’ strategic environmental targets [6]. As a result, three fundamental and unanswered research questions arise about firms’ environmental practices and targets: What are the main dimensions that characterize a truly sustainable firm? How can we assess firms’ progress towards truly sustainable performance and targets? And how does this progress differ across industries and themes?

Our study addresses these questions by proposing an evaluative framework to assess true sustainability performance and targets. Applying this framework to 12,312 observations from 18 global environmental leaders in the emission-intensive basic material sector, we observe weak progress towards true sustainability, with a selective focus on emissions (scope 1, 2, and 3) and limited ambition in environmental target setting.

This study contributes to the nascent body of research on true sustainability [4,5] by developing a framework that characterizes true sustainability dimensions. Our framework operationalizes the true sustainability notion and provides a better understanding of the aspects that allow identifying firms’ efforts toward true sustainability and its assessment. We also contribute to the literature on sustainability and environmental measurement [20,27] with a methodology on current and prospective firms’ environmental initiatives across multiple environmental challenges, such as biodiversity loss or water discharge, which cannot be neglected in the transformation towards true sustainability [28]. By doing so, we unmask existing environmental practices and targets distant from truly responsible environmental efforts, guiding companies towards true sustainability progress. Finally, we extend the signalling theory analyses [18] to signals on future-oriented scenarios, intentionally signalling prospective corporate sustainability behaviors such as environmental targets.

Corporate true sustainability progress is unobservable by outsiders. Because engagement in true sustainability is decisive information to stakeholders, audiences must rely on signals or proxies that communicate firms’ sustainable behavior [29,30] and ‘allow its true nature to be inferred’ [31].

Sustainability or integrated reports act as signals of underlying sustainable efforts. A veracious signal enhances positive stakeholders’ perceptions conducive to developing a ‘green’ reputation and legitimacy [4,32], fostering corporate value [31]. However, not all signals are equally effective in shaping true sustainability perceptions due to stakeholders’ suspiciousness about the conformity between the signal (i.e., sustainability disclosures) and the underlying corporate behavior (i.e., true sustainability) [33]. Stakeholders’ scepticism on signals can arise from fears of symbolic behavior [34] or from the complexity of verifying reported sustainability claims. This study addresses the latter, focusing on how signal distortions can complicate the assessment of firms’ true sustainability efforts.

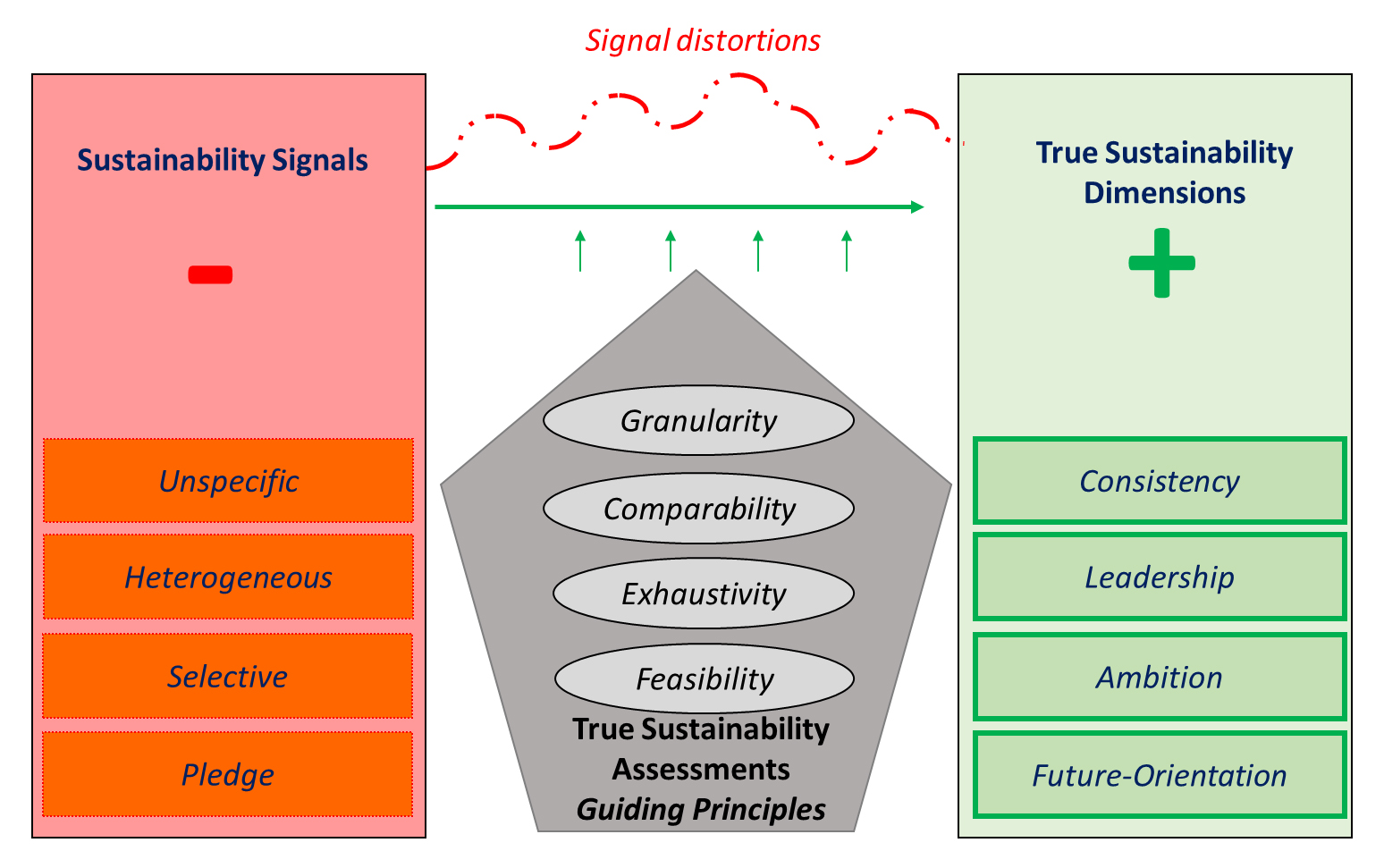

True sustainability has been little researched, nor is there consensus about its definition. Ref. [4] established a typology of business sustainability that culminates in the ‘true sustainability’ business model, understood as a progressive advancement or process rather than a state. Refs. [9,35] further extended this concept. Based on this literature, we argue that true sustainability advancements rely on four core dimensions: consistency, leadership, ambition, and future orientation. In the following sections we examine these dimensions and their underlying guiding principles to provide a comprehensive framework for assessing true sustainability and overcome potential signal distortions.

Consistency and Leadership in True SustainabilityConsistency reflects the specificity in companies’ sustainability disclosure. Unspecific, ambiguous, incomplete, and sometimes opaque non-financial information [12,36,37] obstructs signal observability, thus hampering consistency in true sustainability assessments. Firms apply different levels of data aggregation and units (country, plant, or product), information is provided in absolute or relative terms, and historical trends are not always available [38]. Moreover, since environmental reporting is costly, some firms tend to be more unspecific or vague on issues with perceived lower relevance [39]. These unspecificities distort the signal, compromising the consistency of sustainability information. We introduce granularity as a principle in our framework to capture consistency. Granularity stands for completeness and thoroughness of sustainability disclosures [36,39].

The pervasive heterogeneity across sustainability reports [12] difficults to compare performance across companies, which complicates the assessment of leadership in true sustainability. This challenge, known as signal noise [40,41], arises when reported signals fail to capture key unobservable attributes [34], potentially leading to misjudgments in true sustainability appraisals [42]. Our framework seeks to provide homogeneous assessments that enable comparisons across firms. Since true sustainability operates on a continuum, with varying degrees of progress [4,9], relative improvements become a relevant benchmark [43]. We argue that relative assessments to industry peers are needed to minimize signal noise and effectively evaluate leadership in true sustainability. Accordingly, we incorporate the principle of interfirm comparability into our framework.

Ambition in True SustainabilityBecause sustainable development is a multidimensional and interconnected construct [44], true sustainability requires the ambition to cover a broad spectrum of themes. However, selective or partial disclosure often results in the omission or downplaying of material issues [25]. Companies may be passive regarding challenges where they underperform, focusing on more favorable aspects of their sustainable initiatives [15,25]. Since true sustainability aims for a transformational impact through corporate action, restricting efforts to a narrow set of themes undermines the broader transformation towards true sustainability [45]. For example, emission reductions constitute a prominent environmental goal following the Paris Agreement [46]. Nevertheless, other environmental criteria such as biodiversity, waste management, water use, and recycling, are equally essential for evaluating a firm’s true sustainability performance.

Selective signals may therefore camouflage underlying realities by focusing on a relatively limited number of issues while neglecting others. This ‘signal camouflage’ diverts stakeholder scrutiny away from weak or absent areas, masking weak sustainability efforts. Signal camouflage through selective environmental strategies demands additional analyses to unveil firms’ true nature [29,31]. Therefore, we propose exhaustivity or the pursuit of broad scope in corporate environmental action as an essential guiding principle in our framework.

Future Orientation in True SustainabilityTrue sustainability demands long-term time horizons [4] and a prospective orientation to ensure intergenerational justice [47]. Environmental targets set specific firms’ objectives for performance improvement [6] functioning as aspirational goals and prerequisites to becoming sustainable: ‘without targets, environmental progress is seldom made’ [48]. Therefore, environmental targets are crucial indicators of firms’ sustainability commitment [6].

However, environmental targets often suffer from lack of specificity, heterogeneity, and selectivity, which distort signals and hinder stakeholder assessments of true sustainability. While initiatives such as Science-based targets aim to standardize these efforts, they are not yet fully institutionalized, leaving many targets difficult to compare or verify. Consequently, evaluating environmental targets’ granularity, comparability, and exhaustivity is essential. Moreover, because environmental targets are future-oriented pledges, they carry an ‘intent’ component that can further distort the signal. Although signals typically convey existing, unobservable attributes, intent-based signals [30] may lead to discrepancies between corporate pledges and subsequent actions ex-post [49]. Stakeholders must therefore assess these targets ex-ante, evaluating their coherence with the organizational potential for their achievement within a given timeframe [50]. Past performance can strengthen signals on environmental targets since past signaller characteristics influence current commitments [51,52]. As a result, we introduce environmental targets’ feasibility as a guiding principle in our framework. Feasibility, or the alignment of targets with path development and organizational experience [36], evaluates firms’ potential for accomplishing its targets, acknowledging uncertainties exogenous to the firm, such as technology improvements or resource endowments [53].

To overcome the distortions in sustainability signals, we propose a framework guided by the principles of granularity, comparability, exhaustivity, and target feasibility (Figure 1). In the following sections, we apply the framework to the base material sector.

Figure 1. Signals distortions in true sustainability, guiding principles, and dimensions for a framework to operationalize true sustainability.

Figure 1. Signals distortions in true sustainability, guiding principles, and dimensions for a framework to operationalize true sustainability.

We analyze publicly available sustainability or integrated reports that are externally assured and follow the Global Reporting Initiative (GRI) guidelines, which are the most common for non-financial disclosure [39,54,55]. We select reports for the financial year 2019, avoiding potentially distorting effects of the COVID-19 pandemic and related supply chain disruption. We extract data using content analysis techniques consisting of quantitative and qualitative methods to analyze the documents and categorize the information [56]. As common in content-based disclosure assessments, we assume truthful disclosure [15]. This assumption is supported by external verification and auditing of the reports analyzed, the reputational cost of untruthfulness, and the exposure to third-party ratings. The unit of analysis is “sentence”, either in text or table, expressing quantitative (hard) or qualitative (soft) environmental information. Measurement units include both the number of companies under a particular true sustainability dimension and the number of environmental themes identified in the sample. We chose these measurement units to answer the main research questions.

Among all sustainability indicators in the GRI guidelines, including Environmental, Social, and Governance (ESG), we focus on the environmental ones. While the role of social and governance dimensions in transitioning to true sustainability are significant, stakeholders scrutinize the environmental signals of highly-polluting companies more intensively [14]. According to the GRI 2016 reporting guidelines applied in the 2019 sustainability reports (GSSB, 2016), eight environmental GRI indicators (GRI 301 to 308) cover the following environmental themes: materials (GRI 301), energy (GRI 302), water (GRI 303), biodiversity (GRI 304), emissions (GRI 305), effluents and waste (GRI 306), environmental compliance (GRI 307), and environmental supplier assessment (GRI 308). These are further split into 32 sub-GRI or sub-environmental themes.

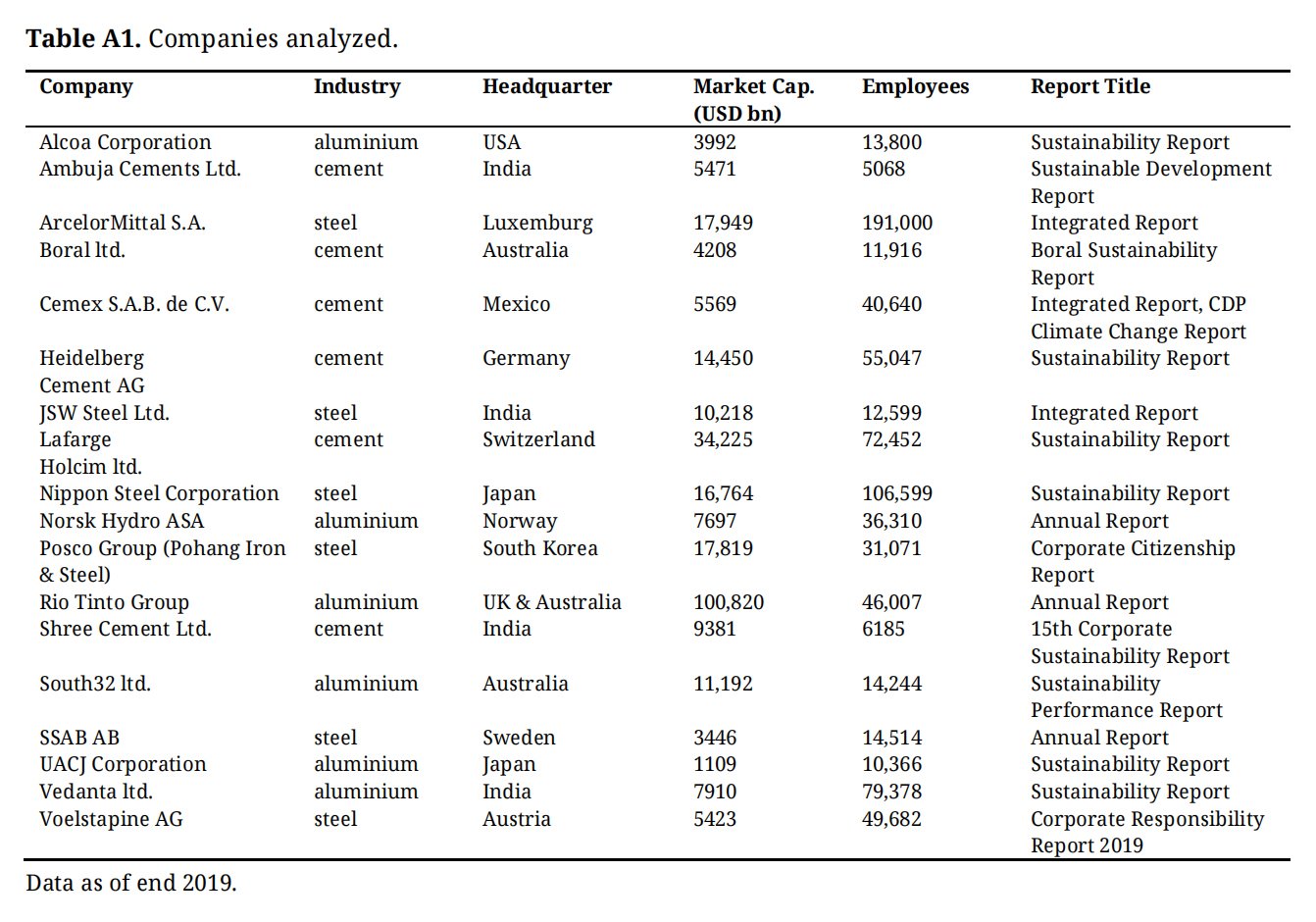

We choose the basic materials sector since it is responsible for 61.7% of all industrial emissions with no large-scale commercial operation using low-emission technologies to date [57]. The sector’s emission-intensive profile makes it less attractive for sustainable investment compared to more easily transitioning industries in the net zero emission race. Transition finance plays a critical role in supporting these sectors by providing capital to invest in cleaner technologies and reduce emissions [58], provided alignment with long-term sustainability. We examine three of the most polluting industries- global steel, cement, and aluminium. Petrochemicals, the third most emission-intensive industry, was excluded due to its heterogeneous production processes and products. To construct the sample, we applied criteria of representativeness and excellence, selecting listed companies that follow GRI guidelines and are classified as best-in-class by the Transition Pathway Initiative (TPI) at the end of 2020 [59]. Appendix A presents the companies analyzed and their main characteristics.

Our 18-company sample is evenly distributed across cement, steel, and aluminium industries and geographically diverse, with one-third (n = 6) headquartered in Europe, 28% in South Asia (India) (n = 5), 16.6% in East Asia (Japan and South Korea) (n = 3), 16.6% in Australia (n = 3), and 5.5% in North America (n = 1). By including only listed companies, the sample lacks representative Chinese companies where non-financial information is often unavailable. Nonetheless, the sample represents global best-in-class basic material companies, ranging from smaller players with 5000–15,000 employees to global conglomerates with more than 100,000 employees (see Appendix A).

This study follows a stepwise approach commonly used in content analysis by developing a scoring system, data compilation and coding, aggregation, and statistical analysis [60].

Scoring MethodThe first step involves developing a scoring system for current and prospective environmental efforts to assess true sustainability progress, guided by the principles of granularity, comparability, exhaustivity, and feasibility. The framework was developed inductively and subsequently refined after the first coding, which raised the need to account for additional entries.

We evaluate two distinct elements: past environmental performance and forward-looking environmental targets. To assess environmental performance, we identify three categories of indicators for each environmental sub-theme (sub-GRI): (i) Baseline indicators, capturing quantitative and qualitative data for the current reporting period; (ii) Trend indicators, with quantitative and qualitative data over three consecutive years; and, (iii) Scope indicators, which provide breakdowns by geographical location, functional activities, and product portfolio items (i.e., source or type, water or waste quality, and destination). Quantitative methods are then used to transform these observations into comparable numerical scores. Following grading schemes from prior studies [20,23], the framework quantifies both qualitative and quantitative data relevant to true sustainability. Past environmental performance is scored across baseline, trend, and scope categories, with a 0–2 scale applied to each, leading to a 0–6 scale per sub-GRI, enhancing both granularity and exhaustivity.

Environmental targets, although not explicitly required by GRI guidelines [61], are evaluated following UN’s recommendations [62]. For each sub-GRI, we score their maturity (medium-term targets until 2030, and/or long-term targets to 2050+), and their nature (quantitative and/or qualitative). Granularity assessments in target setting are crucial for target credibility and consistency. Granularity depicts the levels of depth and precision in the target setting, as determined by their quantitative or qualitative expression and by their medium or long-term horizons. We evaluate each target item strictly binary, with “1” if the corresponding information was disclosed and “0” otherwise. This approach yields a sub-GRI target score on a 0–4 scale. Moreover, targets were evaluated against peers (comparability) and in relation to past environmental performance to assess target feasibility.

Data Compilation and CodingIn the second step, we compiled and analyzed data from the corporate sustainability reports, including supplementary sections, summaries, and appendices. This process was tedious since the reports were complex and lengthy, given that GRI disclosure lacks a standardized structure, with companies reporting in varying sequences, or through case studies or best practices. Occasionally, the GRI and sub-GRI headings were missing or data was reported without specifying the corresponding GRI, further complicating the process of data extraction and coding. Data compilation and categorization were carried out independently by the three researchers. To ensure consistency and reliability, we triangulated by randomly reassigning companies to coders, allowing for cross-validation of the categorizations. The coders attained an agreement in excess of 90%. Any discrepancies in criteria were resolved collaboratively, and coding was updated accordingly. This process yielded 144 observations at the GRI level and 576 at the sub-GRI level. After removing missing data, we compiled 684 observations per company, consisting of 424 environmental performance items and 260 environmental target items. In total, the sample includes 12,312 observations (684 per company × 18 companies). Table 1 presents the descriptive statistics.

Table 1. Descriptive statistics.

Table 1. Descriptive statistics.

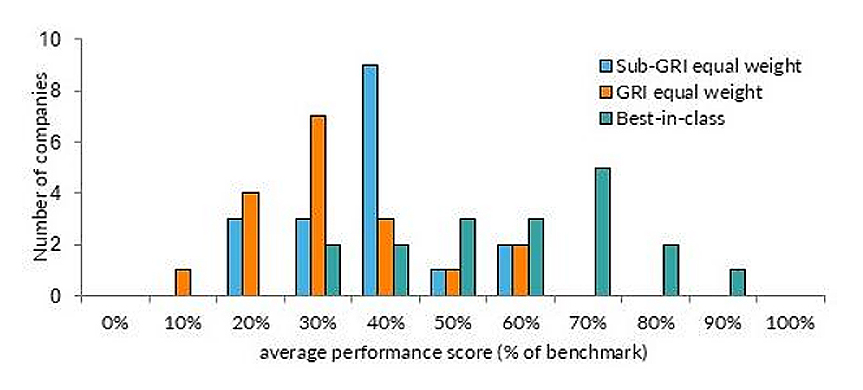

Given the varied number of sub-GRIs within each GRI, ranging from 1 for environmental compliance (307-1) to 7 for emissions (305-1 to 305-7), we conduct a sensitivity analysis on different procedures to aggregate sub-GRI data into a performance score and a target score (Figure 2). Figure 2 visualizes the effects of the alternative aggregation approaches, providing an overview of how different weighting schemes shape the resulting scores. After comparing different weighting schemes, we chose an equal-weight aggregation at the sub-GRI level. This method avoids inflating scores, as seen in the best-in-class approach, which can favor those reporting only a few high performing indicators [29]. Moreover, by equally weighting sub-GRIs instead of GRIs [23], we prevent the overemphasis of GRIs with fewer indicators (e.g., GRI 307) and ensure a balanced representation across all environmental dimensions. This yields a maximum performance score of 192 points (6 points for each of the 32 sub-GRIs) and a maximum target score of 128 points (4 points for each of the 32 sub-GRIs).

Figure 2. Sensitivity analysis for aggregation methods.

Figure 2. Sensitivity analysis for aggregation methods.

The comparability guiding principle of our framework requires relative metrics, since the heterogeneity across companies complicates comparisons of absolute scores [43]. To address this, we build a hypothetical synthetic company that combines the highest observed score for each item across all firms, serving as a true sustainability benchmark. Subsequently, we calculate relative scores to the benchmark for intra- and inter-industry evaluations, allowing us to assess firms’ progress toward true sustainability in a comparative context.

After deriving the final scores (absolute and relative to benchmark), we apply statistical procedures to analyze the data. We conduct univariate analysis and examine bivariate relationships to assess true sustainability dimensions, i.e., consistency, leadership, ambition, and future orientation in environmental performance and targets. Finally, we contrast environmental targets with performance scores, building an evaluative framework that enables true sustainability assessments.

The results analysis of the 18 selected companies is outlined across the four dimensions of true sustainability and its two pillars: performance and targets.

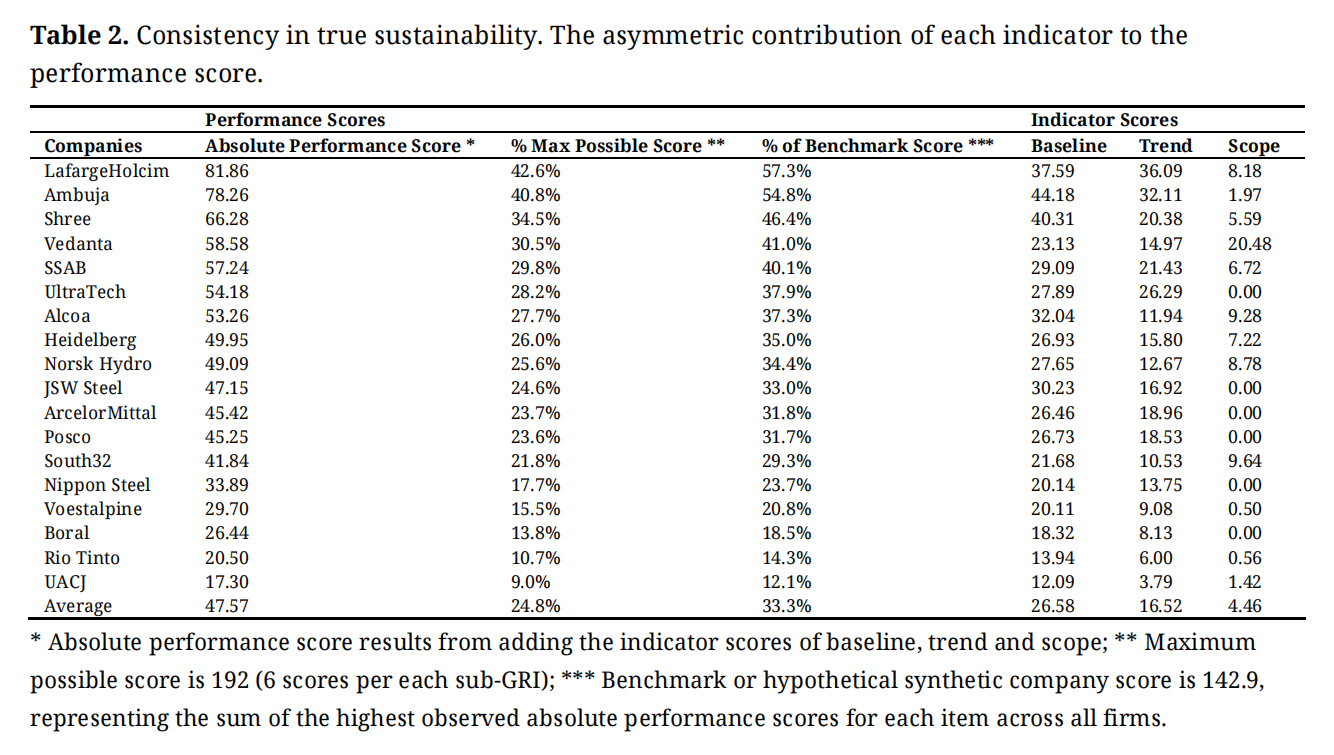

Environmental Performance Scores across True Sustainability Dimensions Consistency in True Sustainability ProgressThe results in Table 2 show the mean performance score across companies, along with the contributions of each indicator category (baseline, trend, and scope) to the performance score. Only 24.8% of the maximum possible score is achieved on average, which denotes a remarkable distance towards fully true sustainability practices. When assessing consistency in true sustainability advancements, we find that companies focus on baseline and trend indicators, contributing, on average, 55.9% and 34.7% respectively to the performance score. However, scope indicators (which demand exhaustive information on products, regions, and impact), are absent in one-third of the sample, contributing by just 9.4% to the performance score. Prior research has shown that corporate environmental data are often heterogeneous and unstructured [12], but we also find that it lacks sufficient detail. This is more significant for environmental themes that rely on internal and external collaboration, for example, supplier assessment, scope 2 and 3 emissions, and resource use by partner organizations. This finding suggests that global value chains must be further integrated through shared reporting practices and information exchange mechanisms to effectively monitor true sustainability advancements.

Table 2. Consistency in true sustainability. The asymmetric contribution of each indicator to the performance score.

Table 2. Consistency in true sustainability. The asymmetric contribution of each indicator to the performance score.

Our hypothetical synthetic company, or benchmark, is constructed by combining the highest observed score for each item across all firms in the sample. This synthetic profile therefore represents the best-achieved performance observed in the dataset—a reference point for both intra- and inter-industry comparisons. The benchmark achieves a total score of 142.9, which corresponds to 74.4% of the maximum possible score. Table 2 illustrates the gap between firm performance scores and the benchmark. Higher performance scores reveal greater leadership in true sustainability. Cement producers LafargeHolcim, Ambuja, and Shree lead the performance ranking (see Table 2). However, when compared to the benchmark, their scores represent only 57.3%, 54.8% and 46.4%, respectively. This indicates that even the best performers remain distant from the true sustainability benchmark case.

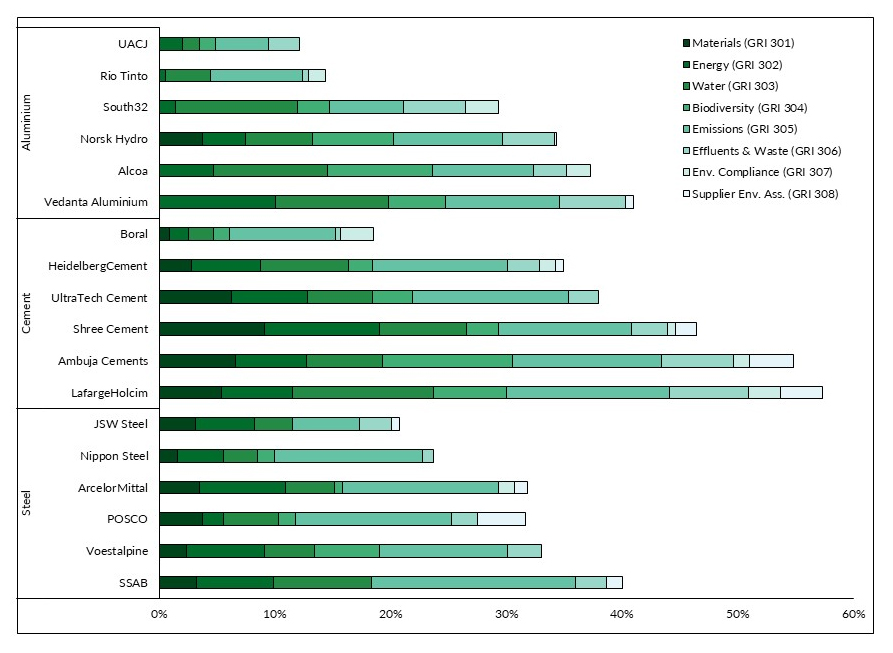

Figure 3 summarizes leadership performance at both company and industry levels across all environmental themes. Cement producers leading the sample, LafargeHolcim, Ambuja, and Shree, present relatively high and balanced scores across all themes, whereas low-scoring companies tend to underperform in categories less directly linked to operational processes, such as biodiversity (GRI 304), effluents & waste (GRI 306), environmental compliance (GRI 307), and supplier environmental assessment (GRI 308).

Figure 3. Leadership in true sustainability across industries, companies, and environmental themes. Performance scores as a % of the benchmark.

Figure 3. Leadership in true sustainability across industries, companies, and environmental themes. Performance scores as a % of the benchmark.

Asymmetries across heavy pollutant industries’ progress towards true sustainability can relate to available technologies such as hydrogen-based steel making, carbon capture for cement plants, green ammonia production, advanced recycling, biobased plastics for petrochemicals, and graphite-free anodes in the aluminium industry [63]. Implementing such technologies on a commercial scale may require an industrial policy focused on creating lead markets, internalizing externalities such as emission costs, supporting technology diffusion, and phasing out emission-intensive production [64]. However, the success of these policies depends on firms’ ability to secure transition funding from investors that value business conduct aligned with true sustainability.

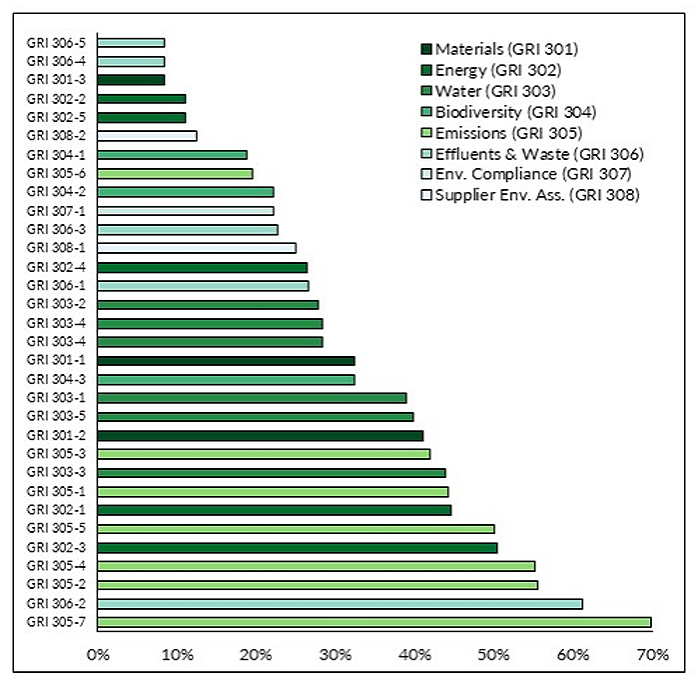

Ambition in True Sustainability ProgressAmbition across a wide range of environmental themes is crucial for true sustainability advancements. However, our findings suggest a selective focus on emission-related themes (Figure 4). Emissions (GRI 305) lead the table, with average sub-GRI performance scores above 50% of the benchmark, while non-emissions related themes represent 27.7% of the benchmark, suggesting a strong ‘emiddion bias’ over other environmental themes.

Figure 4. Ambition towards true sustainability. Average sub-environmental theme performance score (% of the benchmark).

Figure 4. Ambition towards true sustainability. Average sub-environmental theme performance score (% of the benchmark).

We also find evidence of selective behavior within sub-environmental themes. Among Emissions (GRI 305), sub-GRI 305-7, which covers Nitrogen oxides (NOx), Sulphur oxides (SOx), and other significant air emissions, records the highest average score across the sample, (69.8% of the benchmark score). Reporting requirements for sub-GRI 305-7 are more standardized across sectors, using similar table formats for NOx, SOx, and other particle emissions, leading to more comparable and available data. Other Emissions sub-themes score relatively high against the benchmark, namely scope 2 emissions (305-2: 55.6%), carbon intensity (305-4: 55.2%), reduction of greenhouse gas (305-5: 50.0%), and scope 1 emissions (305-1: 44.2%).

Energy (GRI 302) is another highly scored environmental theme, but displays selectivity: While energy intensity (302-3: 50.5%) and energy consumption within the organization (302-1: 44.2%) rank among the highest, energy consumption outside the organization (302-2: 11.1%) and reductions in energy requirements of products and services (302-5: 11.1%) score among the weakest across all environmental themes. A reason for this selectivity may be the complexity involved in monitoring energy consumption outside the organization (302-2) which requires tracking other firms, a more complex task than controlling internal energy consumption (302-1). In turn, reductions in energy requirements of products and services (302-5) demand a more detailed disclosure than general energy intensity indicators (302-1). These findings suggest a tendency to focus primarily on sub-GRI that can be easily measured.

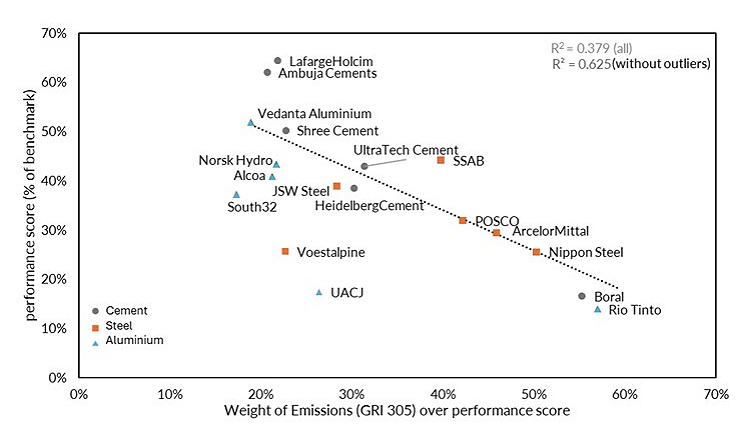

Emissions (GRI 305) represent a much higher proportion of the performance of low-scoring companies, whereas high-scoring firms diversify across multiple environmental indicators, reducing their score reliance on emissions. Figure 5 confirms this pattern, showing an inverse correlation (R2 = 0.379) between the weight of emissions (GRI 305) in total scores and company performance score, indicating that low-scoring companies focus primarily on emissions (GRI 305) at the expense of other environmental themes. The correlation strengthens significantly when considering weak performers UACJ and Voestalpine as outliers (R2 = 0.625).

Figure 5. The weight of emissions (GRI 305) in the performance score. Trendline adjusted by outliers.

Figure 5. The weight of emissions (GRI 305) in the performance score. Trendline adjusted by outliers.

Several factors may explain why firms prioritize certain environmental themes [65]. Materiality plays a role, as it determines which issues firms deem most relevant to stakeholders [66]. Nonetheless, true sustainability requires ambition and a broad scope corporate action beyond materiality. Another reason for selectivity can rely on influencing stakeholder perceptions about firms’ greenness [67]. Companies may prioritize issues that can discursively build a particular image in front of stakeholders [68] and disguise absent efforts using related environmental rhetoric [25]. For example, firms may use metonymy to facilitate stakeholders’ association between limited environmental engagement on a particular theme and broader environmental commitment [69]. A selectivity towards emissions might create an environmental halo effect [67,70] reinforcing the illusion of exhaustive sustainability actions even when initiatives remain narrowly focused.

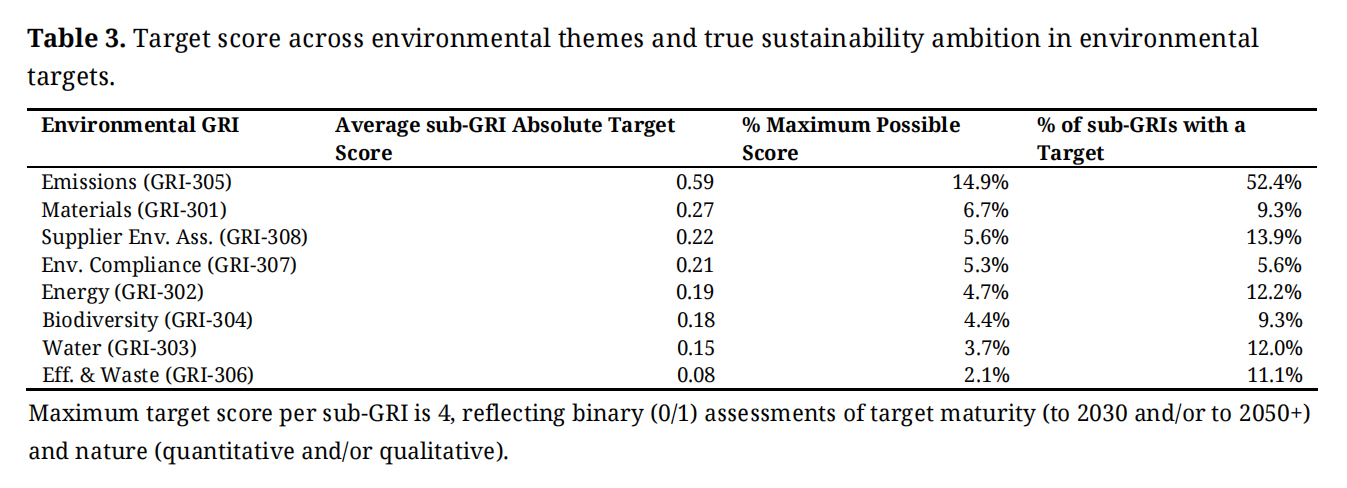

Environmental Target Scores and True Sustainability ProgressEnvironmental targets are evaluated at two analytical levels: the sub-GRI level (maximum score 4, Table 3) and the company level (maximum score 128, aggregating maximum score of 4 across 32 sub-GRIs, Table 4). Overall, environmental target setting is far less frequent than environmental reporting. Table 3 presents target scores and targets ambition across sub-GRI environmental themes, revealing weak target performance. Targets for waste (GRI-306) are particularly marginal, achieving, on average, 2.1% of the maximum possible score. Results improve slightly to 3.7% for water (GRI-303) and 4.4% and 4.7% for biodiversity (GRI-304) and energy (GRI-302), respectively. Targets on emissions (GRI-305) record the highest level of granularity, although still weak, with an average target score of 14.9% of the maximum possible score.

We find evidence of selective behavior and limited ambition in target setting. As shown in Table 3, companies set targets for only 5.6% to 13.9% of the sub-environmental themes, except for emissions (GRI-305), where targets cover 52.4% of its sub-themes (i.e., scope 1, 2, and 3 emissions). This suggests that the average target score is driven by a narrow focus on specific sub-GRIs, rather than a broader, more ambitious approach. The current emphasis on science-based targets [71], which prioritize emission reduction targets, may explain this pattern. However, such selective practice might not be sufficient to approach true sustainability, which demands comprehensive and ambitious targets across all environmental themes. Thus, the high degree of selectivity and lack of ambition towards true sustainability observed in the environmental performance is also present for target setting.

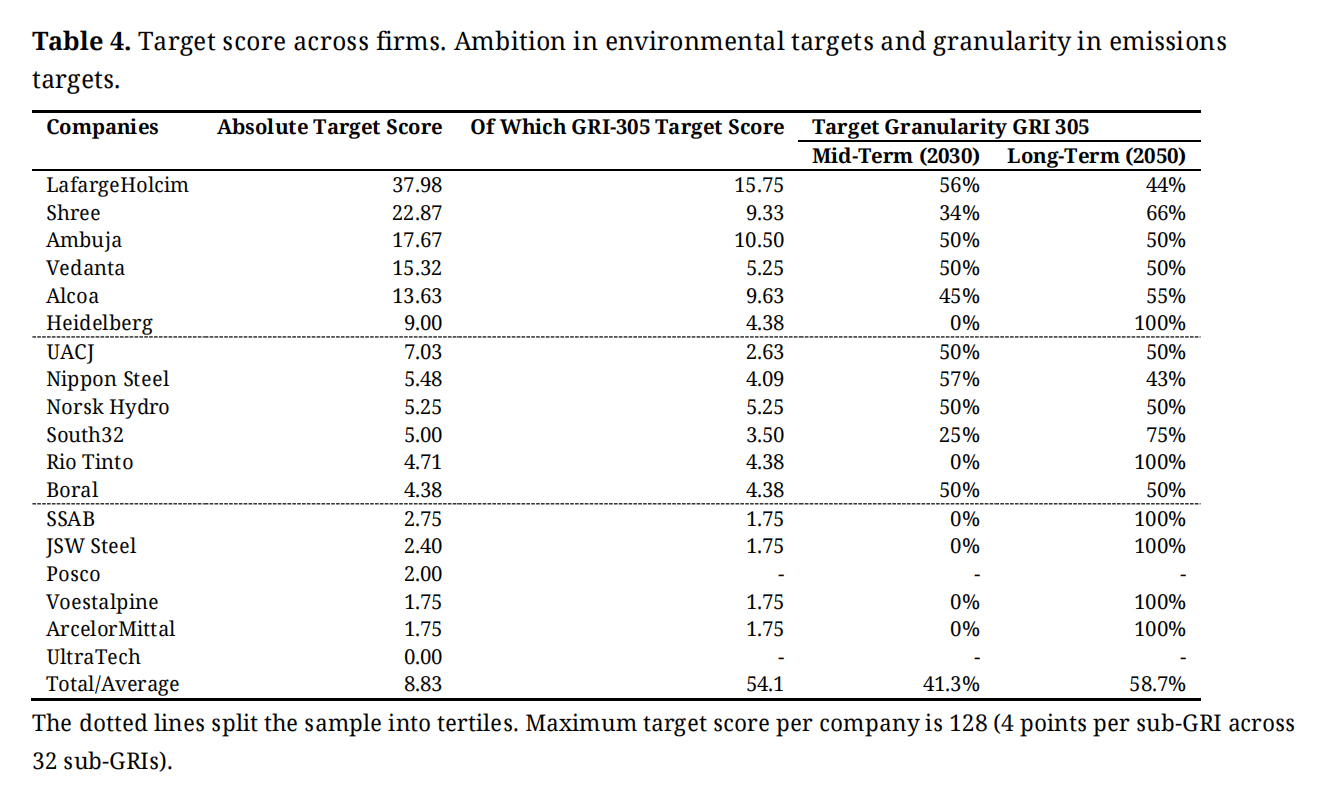

Table 4 presents firms’ environmental target scores, highlighting the observed bias towards emission targets (GRI 305) that account for an average of 54.1% of the total target score. Nonetheless, reliance on emission targets varies by company, with dependence increasing as target scores deteriorate. These findings align with those obtained for performance scores, where leaders demonstrated a broader range of environmental practices across multiple GRIs. The pattern reinforces the finding that broad environmental engagement—rather than a selective focus on emissions—is a distinguishing feature of true sustainability leaders.

Table 3. Target score across environmental themes and true sustainability ambition in environmental targets.

Table 3. Target score across environmental themes and true sustainability ambition in environmental targets.

Table 4. Target score across firms. Ambition in environmental targets and granularity in emissions targets.

Table 4. Target score across firms. Ambition in environmental targets and granularity in emissions targets.

We analyze target granularity by distinguishing between medium-term (2030) and long-term (2050+) targets. Table 4 shows that target-setting leaders tend to define targets for both time horizons, whereas lower-scoring companies focus on long-term targets. Among companies in the 1st and 2nd tertile of environmental target scores, long-term and medium-term targets are relatively balanced. However, among lower-scoring companies in the 3rd tertile, targets are exclusively long-term. Such distant environmental targets might function as a means to postpone challenging short-term decisions [62]. Although regulatory requirements for environmental target setting are evolving, mid-term targets remain rarely institutionalized, especially in non-climate-related areas [6]. For example, the EU Taxonomy (2020) is a step toward harmonized criteria for sustainable investments, but it lacks benchmarks for emission reduction targets in basic material industries [17]. Thus, advancements to assess sustainability achievements would require further development of science-based targets across a broader range of environmental themes, the associated interim plans, and guidance for disclosure [72]. As regulation tightens, our framework can integrate and evaluate progress on environmental target-setting, which are essential for achieving true sustainability.

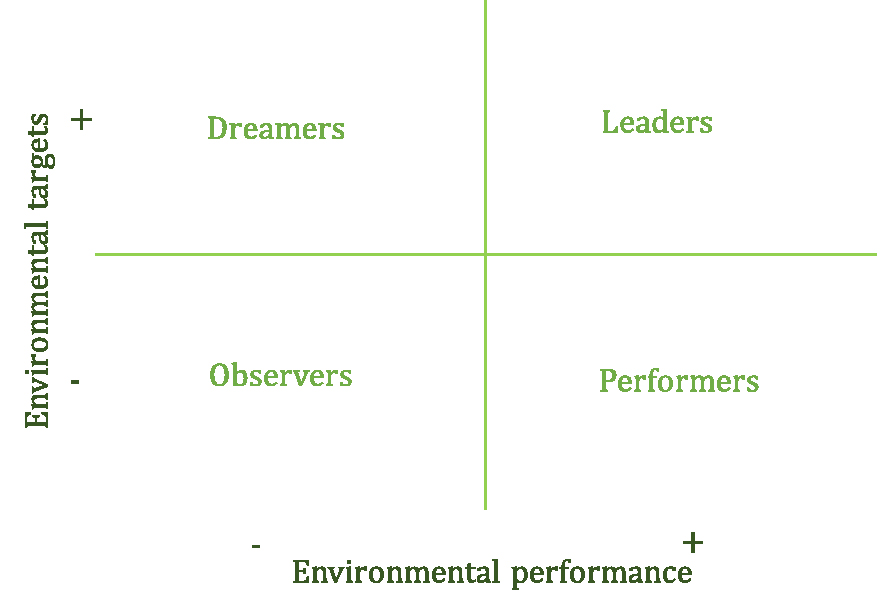

An Evaluative Framework for True SustainabilityWe propose an evaluative framework for true sustainability grounded in empirical evidence from the scoring method, which simultaneously evaluates firms’ environmental performance and environmental target setting. These two pillars represent complementary yet distinct aspects of true sustainability: one captures the effectiveness of past and current environmental actions, while the other reflects the strategic orientation toward future improvement. The intersection of these two variables provides an empirically meaningful basis for classifying companies into four true sustainability profiles (Figure 6). Leaders, Performers, Dreamers, and Observers—each reflecting a different balance between realized environmental outcomes and forward-looking commitments. Leaders demonstrate both high environmental performance and ambitious targets, reflecting robust current practices and a commitment to future improvement. Performers achieve strong environmental outcomes yet lack ambitious targets, indicating steady progress without substantial forward-looking goals. In contrast, Dreamers set high targets but exhibit weak current performance, highlighting a gap between aspiration and action. Lastly, Observers score low in both dimensions, showing minimal engagement with true sustainability practices.

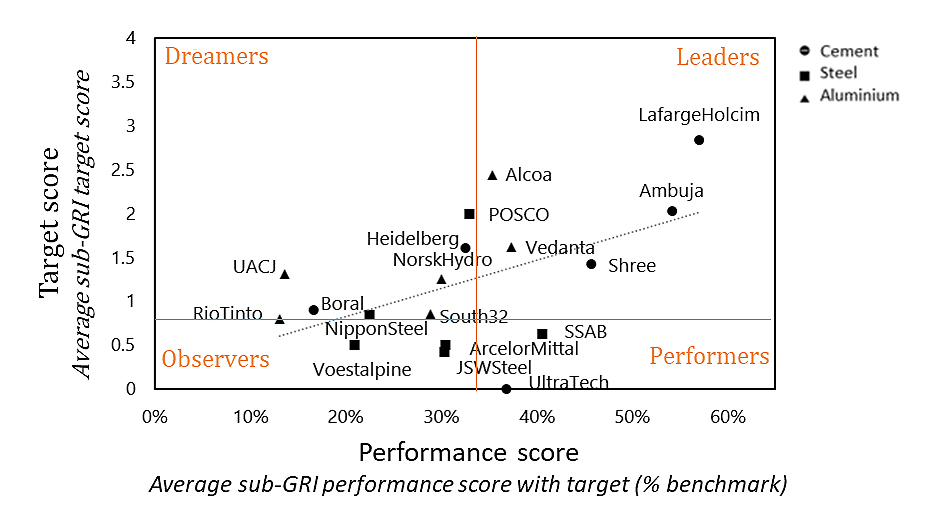

Figure 7 presents the empirical application of the true sustainability framework across the companies and industries analyzed. The results reveal the discrepancy between performance and target scores (R2 = 0.2735), suggesting that environmental targets are not fully supported by prior performance data, and that high environmental performance does not necessarily translate into ambitious target setting except among leaders. The Leaders quadrant is empirically defined by companies such as LafargeHolcim and Ambuja, which pair strong performance with the most ambitious targets. In contrast, SSAB and Ultratech are prominent within the Performers group, exhibiting significant environmental performance but lacking ambitious targets. These discrepancies suggest that better performance scores demonstrating consistency, leadership, and ambition are not always matched by future-oriented target setting, potentially undermining the company’s commitment to true sustainability. We find a significant amounts of companies in the Dreamers cluster (e.g., UACJ, Heidelberg), where ambitious targets contrast with weak past performance, suggesting that target feasibility is compromised by weak prior environmental performance, which may fail to signal true sustainability advancements. Finally, the Observers group, with Voestalpine and Nippon, shows weak performance and minimal target setting, reflecting limited true sustainability engagement.

Figure 6. An evaluative framework to operationalize true sustainability.

Figure 6. An evaluative framework to operationalize true sustainability.

Figure 7. Empirical application of the true sustainability framework across companies and industries. Note: Threshold levels align with average performance scores; R2 = 0.2735.

Figure 7. Empirical application of the true sustainability framework across companies and industries. Note: Threshold levels align with average performance scores; R2 = 0.2735.

This paper presents a framework for assessing true sustainability by analyzing corporate signals—nonfinancial disclosures related to both existing operations (environmental performance) and prospective goals (environmental targets). Our approach follows a scoring system for rating disclosures, which does not assess truthiness in reported information but disclosed claims [23], thus allowing for inter- and intra-industry comparisons and benchmarking. We apply the framework to highly polluting industries that are particularly dependent on transition finance to transform toward greener practices and reach net-zero emissions by 2050 [17].

The results highlight industry leaders, but also reveal a lack of detail in sustainability disclosures across business units or activities. Environmental performance and target setting are often selective, with a strong focus on emissions, neglecting other themes. This bias is particularly pronounced among true sustainability laggards. In particular to environmental targets, there is a disconnect between past performance and target-setting, except for leading companies, raising doubts about their feasibility. Furthermore, we observe a predominance of long-term targets over mid-term ones, often without corresponding transition plans to support and monitor their achievement.

By depicting an evaluative framework on true sustainability progress, this study contributes to the literature in three main ways. First, we extend the stream of research on true sustainability [4,5] by operationalizing the notion through an evaluative framework. In contrast to earlier studies that rely on theoretical underpinnings of true sustainability, our framework advances theory by depicting the key dimensions for true sustainability and subsequently offers a quantitative method to assess true sustainability advancements. This approach enables companies and policymakers to benchmark progress and provides academics with an operational foundation of the true sustainability concept. Second, this study contributes to the growing body of literature on sustainability measurement [20,27], and environmental targets evaluation [71] by integrating prospective targets into the framework. Given that investment decisions particularly in transition finance are future-oriented [58,73], incorporating both current performance and future targets is critical. This inclusion aligns with the needs of investors seeking to fund companies in progress towards true sustainability, thereby bridging sustainable finance and corporate environmental strategies.

Finally, we extend the application of signalling theory in business studies [29,30]. Prior research used signalling theory to differentiate substantive sustainability efforts vis-à-vis opportunistic behavior [74]. However, its application to the emerging phenomenon of true sustainability remains novel. Our framework to evaluate true sustainability progress aims to counteract signal distortions, enhancing true sustainability assessments. Besides, most research in management studies using signal theory has evolved around unobservable and existing latent firms’ traits [30,31], while signals about future intentions remain unexplored. Some studies have addressed signalling intents in entrepreneurship [75,76], referring to unintended signals that indicate possible future action [77]. However, these signals are less costly since they can be easily imitated (i.e., cheap talk) [30]. In contrast, we examine how intentional signals (i.e., environmental target setting) about the future can become valuable indicators of true sustainability, a perspective not previously studied. These signals are paramount for assessing truly sustainable environmental efforts by green investors to anticipate firms’ prospects.

Our framework is generalizable to any industry, although the findings in this study are limited to our sample in the basic materials industry. However, the essential issues highlighted here transcend to other sectors requiring transition finance, such as oil and gas or traditional utilities. While results may vary with a different sample, our focus on best-in-class companies suggests that benchmark improvements are unlikely.

This study has strong implications for organizations and their environmental impact. From a managerial perspective, the framework not only evaluates true sustainability progress but can serve as an internal guide to foster corporate sustainable actions, encourage data collection, strengthen sustainability disclosure comprehensiveness, and enhance performance monitoring. This aligns with research highlighting the role of strategic frameworks in fostering corporate sustainability [78].

Our framework and methodology enhance transparency and investors’ confidence in true sustainability. Investors, particularly asset managers and transition finance providers, can use this framework to obtain a comprehensive and comparable picture of environmental performance and targets based on public information. By reducing information asymmetries between firms and financial market participants, this approach may lower capital constraints, especially for highly polluting firms. In the context of transition finance [79,80], this framework enables investors to identify advancements in true sustainability, ensuring funding for developing low-carbon technologies and phasing out emission-intensive practices.

All data generated from the study are available in the manuscript.

Conceptualization, EA, TG and A-JK; methodology, TG; validation, EA, TG and A-JK; formal analysis, TG; writing—original draft preparation, EA; writing—review and editing, EA, TG, A-JK; visualization, TG. All authors have read and agreed to the published version of the manuscript.

The authors declare no conflicts of interest.

This work has been supported by the Madrid Regional Government (Grant PHS-2024/PH-HUM-294), Spain.

Table A1. Companies analyzed.

Table A1. Companies analyzed.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

59.

60.

61.

62.

63.

64.

65.

66.

67.

68.

69.

70.

71.

72.

73.

74.

75.

76.

77.

78.

79.

80.

Aracil E, Gerres T, Kuehlwein A-J. Can environmental performance and targets signal true sustainability advancements? An evaluation framework with evidence from polluting industries. J Sustain Res. 2025;7(4):e250069. https://doi.org/10.20900/jsr20250069.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions