Location: Home >> Detail

J Sustain Res. 2026;8(3):e260064. https://doi.org/10.20900/jsr20260064

,

Katri Hurskainen ,

Pekka Tervonen ,

Harri Haapasalo

,

Katri Hurskainen ,

Pekka Tervonen ,

Harri Haapasalo

*

Although hydrogen-based direct reduction is an important pathway for decarbonising primary steelmaking, the deployment of low-emissions hydrogen has progressed more slowly than expected based on policy and industry ambitions. This study examines how the conditions for hydrogen-based steelmaking are forming in the Bothnian Bay, a cross-border industrial corridor between Finland and Sweden with the potential for renewable electricity, established steelmaking capacity, energy-intensive industry and emerging hydrogen initiatives. An exploratory qualitative research design is applied based on five semi-structured expert interviews and a complementary Webropol survey of 26 regional stakeholders. The empirical material is analysed thematically and interpreted through an analytical framework that considers the stages of the hydrogen-based steel value chain and technological, infrastructural, market and institutional conditions. The findings show that the value chain in the Bothnian Bay remains at an early, pre-commercial stage. The region has a strong regional basis, including renewable electricity potential, industrial competence, research expertise and cross-border collaboration; however, major constraints persist, including limited industrial-scale hydrogen production, immature storage and transport options, uncertainty in electricity prices, incomplete market formation, and differences in permitting, policy support and investment sequencing between Finland and Sweden. Despite its strong potential for hydrogen-based steel development, the Bothnian Bay is not yet implementation-ready as an integrated hydrogen-based steel ecosystem. Progress will require coordinated development of electricity supply, hydrogen production, storage and transport options, industrial offtake, market formation, permitting and cross-border governance. Hydrogen implementation gaps appear at the regional cluster level, and there is a need to convert regional strengths into bankable and coordinated implementation pathways.

BF–BOF, blast furnace–basic oxygen furnace; CAPEX, capital expenditure; DRI, direct reduced iron; EAF, electric arc furnace; ETS, emissions trading system; EU, European Union; H2-DRI, hydrogen-based direct reduction; IEA, International Energy Agency; RQ, research question

The iron and steel sector is one of the largest industrial sources of global carbon dioxide (CO2) emissions, as it is responsible for approximately 7% of global CO2 emissions [1]. Most steel is still produced through the blast furnace–basic oxygen furnace (BF–BOF) route, which is highly energy- and carbon-intensive and typically emits around 1.8–2.0 tCO2 per tonne of steel [1–3]. Although the electric arc furnace (EAF) route yields substantially reduced emissions when powered by low-carbon electricity, particularly when using recycled scrap, the availability of this scrap and the quality requirements mean that the primary form of steelmaking will remain necessary to meet global demand [2,4,5]. Consequently, deep decarbonisation of the steel sector requires not only improved recycling, but also alternative primary production routes that reduce emissions from iron ore reduction.

Hydrogen-based direct reduction (H2-DRI) has gained prominence as one of the main pathways for decarbonising primary steelmaking. In H2-DRI, iron ore is reduced using hydrogen rather than carbon-based reductants, and the reduced iron can then be processed in EAFs. When combined with low-carbon hydrogen and electricity, this route can substantially reduce process-related emissions and offers one of the most viable long-term options for near-zero-emissions primary steel production [6–9]. However, while this pathway avoids the main bottlenecks associated with dependence on coal and coke, it shifts the key constraints toward electricity availability, hydrogen supply, ore quality, infrastructure, storage and market formation [10]. Steel decarbonisation is therefore increasingly understood not as a simple substitution of one technology with another, but as a broader industrial transformation involving new process technologies, energy inputs, value chains and investment structures [1,11,12].

Hydrogen is widely regarded as a key enabler of industrial decarbonisation and a renewable-energy-based economy, especially in hard-to-abate sectors where emissions are difficult to eliminate, such as steelmaking [13–15]; however, the benefits to the climate from this approach depend strongly on the production pathway. Green hydrogen, which is produced through water electrolysis using renewable electricity, is generally considered the most sustainable option, but its deployment depends on the simultaneous scaling of low-carbon electricity, electrolysers, storage, transport infrastructure and end-use demand across wider power-to-X and industrial applications [13,16–20]. The EU has set ambitious targets for hydrogen, including a renewable hydrogen electrolyser capacity of 40 GW and, through REPowerEU, a domestic renewable hydrogen production of 10 million tonnes, and renewable hydrogen imports of 10 million tonnes by 2030 [21–24].

Despite these ambitions, however, the deployment of low-emissions hydrogen remains limited. The International Energy Agency (IEA) reports that global demand for hydrogen reached almost 100 Mt in 2024, while low-emissions hydrogen still accounted for less than 1% of total production. According to the IEA, the potential low-emissions hydrogen production that could be achieved by 2030 based on announced projects has declined from 49 to 37 Mtpa because of project delays and cancellations [25]. Odenweller and Ueckerdt (2025) [26] also show that only 7% of the green hydrogen capacity expected for 2023 was realised on schedule, indicating that projects at the concept or feasibility stage should not be treated as reliable evidence of near-term deployment [26]. These findings indicate that hydrogen-based industrial decarbonisation should not be viewed solely as a technological opportunity, but also as an implementation challenge. For hydrogen-based steelmaking, the central question is not only whether H₂-DRI is technically feasible, but whether the required energy, infrastructure, market, governance and investment conditions can be developed quickly enough to support industrial-scale deployment [26,27].

From the perspective of sustainability transitions, this implementation gap can be understood as a socio-technical coordination problem rather than as a delay in technology deployment. Sustainability transitions involve long-term, multidimensional changes in technologies, infrastructures, markets, user practices, business models, regulations and institutions [28]. Existing industrial systems are also shaped by path dependencies and lock-ins, meaning that new low-carbon technologies must be aligned with complementary assets, investment structures and governance arrangements before established production systems can be replaced or reconfigured [28–30]. In the case of hydrogen-based steelmaking, this implies that H2-DRI, renewable electricity, hydrogen production, storage, transport, offtake markets, certification and permitting must be developed in a mutually supportive sequence. The implementation gap therefore reflects not only technical immaturity but also uncertainty over coordination, bankability, infrastructure sequencing and market formation.

Value Chains for Hydrogen-Based Steel and the Formation of Regional EcosystemsHydrogen-based steelmaking requires coordinated development across several interdependent stages of the value chain, such as low-carbon electricity supply, hydrogen production, hydrogen storage and transport, iron ore preparation, direct reduction, electric arc furnace steelmaking, logistics and end-use markets for low-emissions steel. The concept of a value chain is used here in an extended inter-firm and regional context, rather than simply as an internal firm-level tool, to examine how multiple actors contribute to value creation across the areas of production, infrastructure and market formation [31–33]. This perspective is particularly relevant for hydrogen-based steel, since no single actor can independently establish the full chain from renewable electricity and hydrogen production to industrial steelmaking and downstream demand.

In this study, the value chain for hydrogen-based steelmaking is defined as the full set of interdependent activities required to enable this process, from low-carbon electricity supply and hydrogen production to hydrogen storage, transport, direct reduction, electric arc furnace steelmaking, logistics and end-use markets. By contrast, the hydrogen value chain refers more narrowly to hydrogen production, storage, transport and distribution. The term ‘industrial ecosystem’ is used to describe the broader actor and coordination environment surrounding the value chain, including steel producers, energy companies, infrastructure operators, technology suppliers, research organisations, public authorities and potential customers. The concept of a hydrogen valley is treated as a related but more specific reference concept for analysing regional hydrogen integration; it does not imply that the Bothnian Bay already constitutes a complete hydrogen valley. Accordingly, the empirical focus of this study is the emergence of a hydrogen-based steel value chain, while the ecosystem concept is used to analyse the broader actor, governance and coordination environment that may enable or constrain the formation of that value chain.

Hydrogen value chains are characterised by strong interdependencies between production, storage, transport and end use [34,35]. Investment in hydrogen production depends on credible demand from industrial off-takers, while industrial users depend on reliable hydrogen availability, predictable electricity prices, suitable infrastructure and long-term commercial arrangements. This creates coordination problems typical of emerging industrial ecosystems, where complementary investments must be aligned before the full value chain can become operational [29,30]. In hydrogen-based steelmaking, these interdependencies are especially demanding because H2-DRI–EAF production depends simultaneously on low-carbon electricity, hydrogen availability, suitable ore quality, process integration, storage or buffering capacity, and market demand for low-emissions steel [4,7,12,20].

Infrastructure is an essential aspect of the formation of a value chain. Hydrogen may be produced on site or near industrial users or be transported from external production sites, and each of these configurations imposes different requirements for electricity grids, storage, transport systems, ports and logistics. Hydrogen transport and storage technologies such as pipelines, underground storage, carrier-based solutions, ammonia and metal hydrides are capital-intensive and geographically dependent [20,21,25,35]. Studies of hydrogen corridors in Europe therefore emphasise the need for integrated planning across production sites, storage facilities, ports and inland transport networks, while also showing that no single infrastructure configuration is universally applicable [36,37].

The concept of regional ecosystems helps to capture the challenges related to coordination by directing attention to the roles of actors, interdependencies and value creation beyond individual firms [38]. Hydrogen valleys represent localised hydrogen ecosystems characterised by technological and sectoral integration, multi-actor involvement, completeness of the value chain, and active deployment [39–41]. Recent legal research has shown that hydrogen valleys remain affected by definitional ambiguity and fragmented regulatory treatment, which may create uncertainty in terms of investment, permitting and cross-sectoral coordination [40]. In this article, the logic of the hydrogen valley is not used to imply that the Bothnian Bay already functions as a complete hydrogen valley; instead, it provides a lens for an analysis of how regional actors, industrial demand, energy resources, infrastructure and knowledge capabilities are beginning to form around hydrogen-based steel production. The formation of an ecosystem in this way can support coordination and shared learning, although misaligned incentives, unclear actor roles and fragmented governance may delay the creation of joint value [42].

The Bothnian Bay is a suitable empirical setting for this analysis as it has major steelmaking and metallurgical sites, renewable electricity potential, ports, logistics infrastructure, energy-intensive industry and research expertise across a cross-border industrial corridor. This regional configuration is important because recent studies of steel transitions and European energy systems suggest that renewable-rich regions may gain new industrial advantages as energy-intensive production becomes increasingly shaped by access to low-cost renewable electricity and hydrogen infrastructure [11,43]. The region includes SSAB’s steel plants in Raahe and Luleå, Outokumpu’s stainless steel production complex in Tornio, and a wider range of process industry, mining, forestry and energy infrastructure around Oulu, Raahe, Kemi, Tornio, Luleå and Skellefteå. The Swedish side also hosts major hydrogen-based steel initiatives, including HYBRIT and Stegra, which illustrate how fossil-free electricity, iron ore resources and coordinated industrial strategies can support the early deployment of low-carbon steel production [9,44,45]. Since hydrogen-based steel production is highly electricity-intensive, the regional electricity system is a prerequisite for the formation of a value chain, particularly under conditions of renewable intermittency, seasonal variation and storage needs [46]. At present, the regional value chain remains incomplete, making the Bothnian Bay a useful case for examining how hydrogen-based steel ecosystems emerge before full industrial-scale implementation.

Cross-Border Coordination and System-Level ConditionsCross-border hydrogen-based industrial development is shaped not only by technological and infrastructural readiness, but also by institutional compatibility and coordinated governance. Hydrogen value chains require decisions on electricity supply, hydrogen production, storage, transport, certification, safety regulation, permitting and industrial offtake [21,35,36]. When these decisions are distributed across national borders, coordination becomes more complex, since actors operate under different policy frameworks, permitting procedures, support mechanisms, and logics for infrastructure planning [36,37]. These differences can affect the timing of major investments and increase uncertainty for firms that depend on complementary assets across the value chain.

In the existing ecosystem literature, it is emphasised that emerging industrial systems depend on complementary investments and coordinated sequencing between multiple actors [29,30]. This is especially relevant for hydrogen-based steelmaking, where the roles of steel producers, energy companies, infrastructure operators, technology suppliers, public authorities and research organisations must be aligned before the value chain can function at an industrial scale [29,30,47]. If the development of hydrogen production, electricity supply, storage, transport, permitting and demand formation occurs at different speeds, the result may be fragmentation of the project rather than an integrated regional value chain [34,35,42]. In cross-border regions, this risk is amplified by differences in national policy priorities, administrative procedures and infrastructure investment timelines [36,37].

Studies of hydrogen infrastructure also show that institutional divergence affects not only regulation but also the practical sequencing of production, storage and transport investments. From the modelling of European hydrogen systems, it is clear that future hydrogen development may involve different combinations of domestic production, regional distribution, imports, storage and corridor-based transport, depending on national strategies, constraints on renewable energy, and infrastructure choices [36,37,43]. International comparative research has also highlighted the importance of harmonised certification schemes and mutually recognised sustainability criteria in terms of enabling hydrogen trade and avoiding regulatory fragmentation [48,49]. These issues are significant for cross-border industrial regions because firms require predictable rules before committing to long-term investments in hydrogen production, infrastructure or low-carbon steelmaking.

For this reason, this study analyses the emergence of a value chain for hydrogen-based steelmaking through a framework based on two dimensions. The first dimension involves the stages of the value chain, such as hydrogen production, storage, transport and distribution, and end use in steelmaking. The second dimension consists of the cross-cutting conditions at the system level that shape whether these stages can develop in a coordinated way. Existing studies identify four categories, which represent technological, infrastructural, market and institutional conditions [20,29,30,41]. Technological conditions refer to the maturity and integration of electrolysis, hydrogen-based direct reduction, electric arc furnaces and renewable electricity supply [7,9,16]. Infrastructural conditions include electricity grids, hydrogen production and storage options, transport solutions, ports, logistics and connections to industrial off-takers [20,35,37]. Market conditions are related to cost structures, demand formation, long-term offtake arrangements, investment incentives and competitiveness of low-emissions steel [25,34,50]. Institutional conditions cover permitting, certification, safety regulation, governance arrangements and cross-border coordination mechanisms [36,37,40,48].

This framework is used to address two analytical questions: firstly, the region-specific factors that influence the emergence of a hydrogen-based steel value chain in the Bothnian Bay are examined; secondly, the system-level requirements that must be met in order for the region to progress from early-stage development toward a functioning value chain are identified. The framework therefore connects the empirical regional case to broader debates on hydrogen implementation gaps, the formation of industrial ecosystems, and the cross-border coordination of value chains.

Aims, Contributions and Research QuestionsThe preceding sections show that although hydrogen-based steelmaking is technically promising, its deployment depends on more than simply the maturity of individual technologies. Prior studies have examined steel decarbonisation pathways, hydrogen production, hydrogen infrastructure, hydrogen valleys and industrial ecosystem formation; however, less attention has been paid to the interplay of these elements in a specific cross-border industrial region where steel production, renewable electricity, infrastructure, policy frameworks and actor coordination are developing unevenly. This gap is important because uncertainty over hydrogen implementation is increasingly visible: project announcements, regional potential and policy targets do not automatically translate into operational and bankable value chains, especially when projects remain at the concept or feasibility stage [26,27].

This article addresses this gap by analysing the emergence of a hydrogen-based steel value chain in the Bothnian Bay region, a cross-border industrial corridor between Finland and Sweden. The region is a relevant empirical case because it combines established steelmaking and process industry capabilities with renewable electricity potential, ports, logistics infrastructure, research expertise and ongoing hydrogen-related initiatives. There are also unresolved questions concerning industrial-scale hydrogen production, storage and transport options, market formation, permitting, investment sequencing and cross-border coordination.

The aim of this study is to identify the region-specific factors and system-level requirements that shape the development of a hydrogen-based steel value chain in the Bothnian Bay. The contributions of the article are twofold: firstly, it provides a regionally grounded analysis of the emergence of a value chain for hydrogen-based steelmaking in a cross-border industrial setting; and secondly, it connects the debate over the hydrogen implementation gap with perspectives on industrial ecosystems and value chains by showing how technological, infrastructural, market and institutional conditions must be aligned before regional potential can be translated into industrial-scale deployment.

To guide the analysis, the following research questions are considered:

RQ1:

RQ2:

In this study, a qualitative research design based on semi-structured expert interviews and a complementary stakeholder survey is applied. The empirical material is analysed through the framework described above, in which the stages of the value chain are combined with technological, infrastructural, market and institutional conditions. Through this approach, the study examines the ways in which regional characteristics enable or constrain the formation of a value chain for hydrogen-based steel and the coordinated prerequisites for further scale-up.

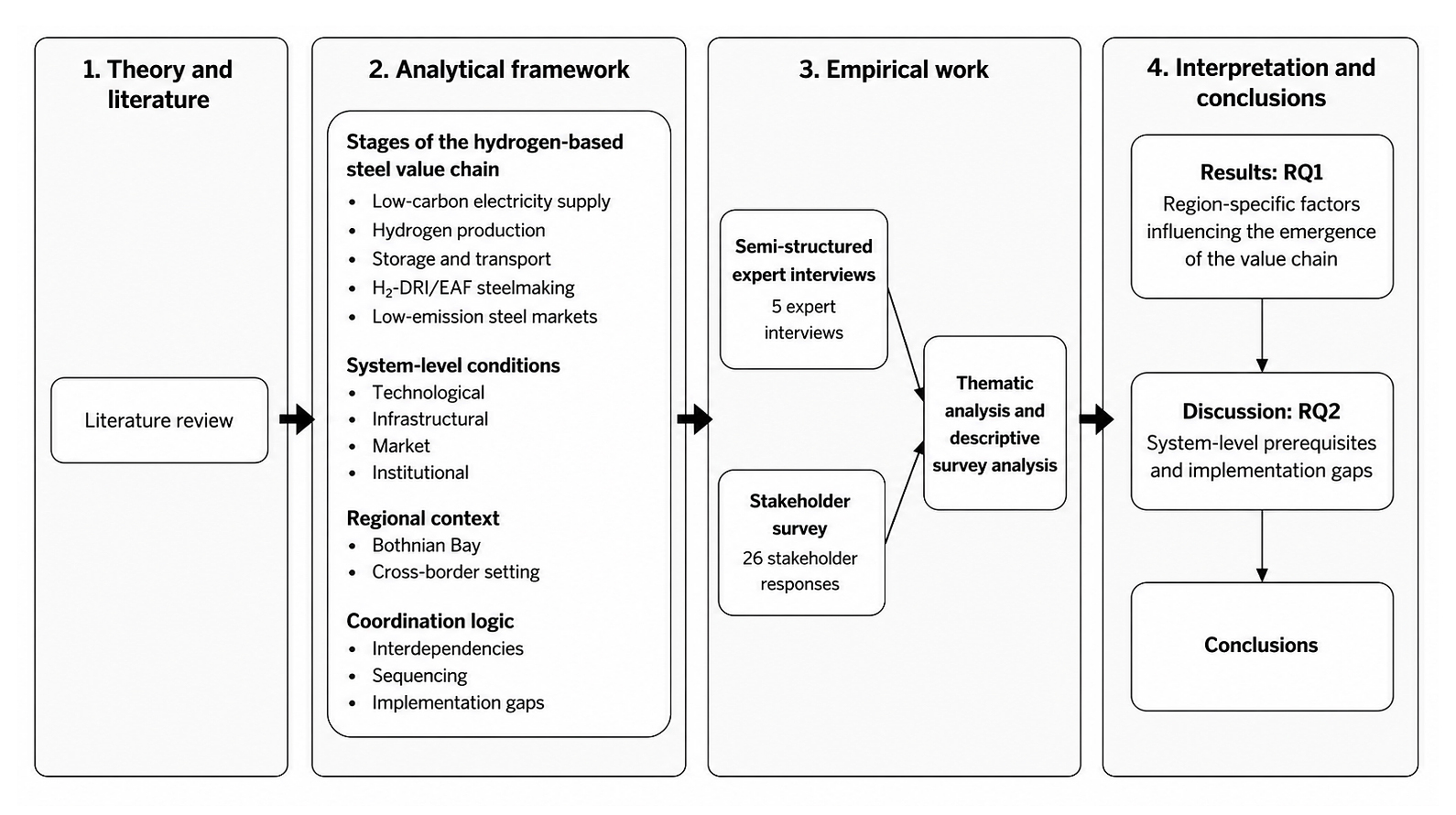

An exploratory qualitative research approach is applied here. This approach is particularly suitable for examining emerging industrial transformations characterised by uncertainty, evolving actor constellations and limited prior empirical evidence [51,52]. The empirical material consists of semi-structured expert interviews and a complementary stakeholder survey conducted using Webropol. Both instruments were organised around the analytical framework developed in the Introduction, covering the stages of the value chain and the necessary technological, infrastructural, market and institutional conditions, regional context and coordination logic. The interviews provided in-depth expert insights, while the survey broadened the empirical base by capturing perceptions from a wider set of regional stakeholders. Figure 1 summarises the research design and analytical framework of the study, and shows how the literature review informed the framework, how the framework guided the empirical work, and how the material was interpreted in relation to RQ1 and RQ2.

Figure 1.

Research design and analytical framework used to examine the emergence of a value chain for hydrogen-based steel in the Bothnian Bay.

Figure 1.

Research design and analytical framework used to examine the emergence of a value chain for hydrogen-based steel in the Bothnian Bay.

The research design was chosen to examine an emerging industrial transition in which the actors’ roles, infrastructure configurations, market conditions and institutional arrangements were still developing. This design was appropriate because the development of hydrogen-based steelmaking in the Bothnian Bay remains at an early stage and the number of actors with direct knowledge of the topic is limited.

In this empirical design, semi-structured expert interviews were combined with a complementary stakeholder survey. The interviews generated an in-depth qualitative understanding of the regional development of the value chain, while the survey broadened the empirical base by capturing perceptions from a wider group of relevant regional actors. The aim of the study was not to ensure statistical representativeness; instead, purposive sampling was used to capture organisational perspectives relevant to the emergence of this value chain.

The empirical design should therefore be understood as exploratory and interpretive rather than representative or predictive. The purpose of the interviews and survey was to identify how informed regional actors perceived the maturity, constraints and coordination needs of the emerging value chain for hydrogen-based steelmaking. The study did not seek to quantify the full techno-economic feasibility of hydrogen-based steelmaking or to provide statistically generalisable evidence about all regional stakeholders; the empirical material was instead used to analyse perceived readiness, bottlenecks and system-level prerequisites in a region where the value chain is still largely at a pre-commercial stage.

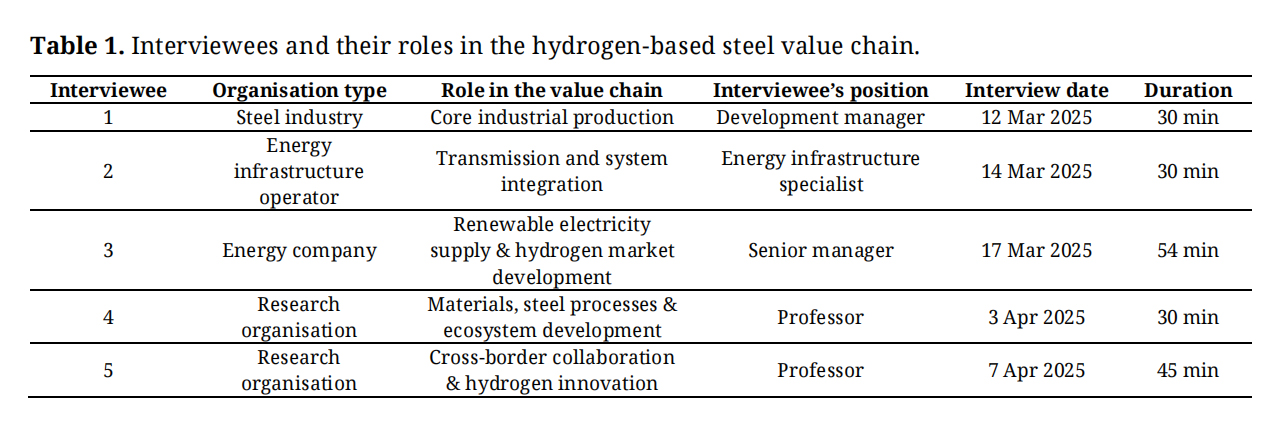

Data Collection Expert InterviewsFive semi-structured interviews were conducted with representatives of key organisations that were involved in or influencing the development of hydrogen-based steel in the Bothnian Bay region. Interviewees were selected using purposive sampling, a method in which participants are chosen based on their expertise, organisational role and relevance to the research topic rather than through random selection [53,54]. The aim was to include perspectives from core industrial production, energy supply and infrastructure, and research-based ecosystem development, rather than to produce a representative sample of all regional actors. These organisations were prioritised because they represent actors with direct experience of steel production, electricity and hydrogen infrastructure, energy market development, relevant materials and cross-border innovation. The interview sample did not cover all of the relevant stakeholder groups; in particular, financial institutions, environmental non-governmental organisations, downstream steel customers and public policymakers were not included as separate interviewee categories. Their absence limited the extent to which the study could assess financing conditions, societal acceptance, downstream demand and policy implementation from the perspectives of these actor groups.

The interviewees and their organisational roles are summarised in Table 1. Each interviewee’s position is reported in anonymised form to indicate a functional perspective while protecting individual and organisational confidentiality. Interviews were carried out in the spring of 2025, lasted 30–55 min, and followed a shared interview guide focusing on the development of the value chain, regional strengths and gaps, cross-border cooperation in the Bothnian Bay, and system-level prerequisites for scaling beyond pilots. All interviews were audio-recorded and transcribed verbatim.

Table 1. Interviewees and their roles in the hydrogen-based steel value chain.

Table 1. Interviewees and their roles in the hydrogen-based steel value chain.

To complement the interviews, a stakeholder survey was conducted using Webropol among organisations active in, or strategically relevant to, hydrogen-related development in the Bothnian Bay. The survey sample was defined using purposive sampling, targeting organisations with direct involvement in or strategic relevance to hydrogen-related activities rather than a general or random population [53,54].

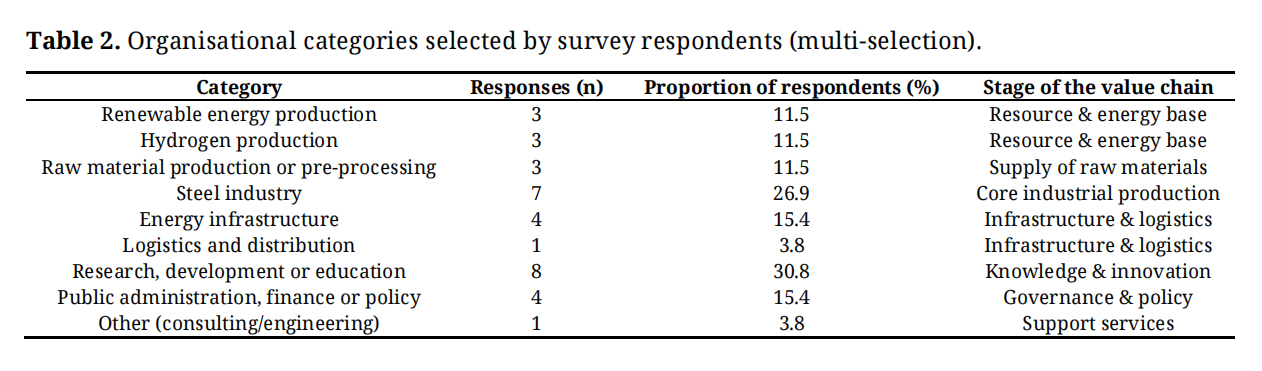

The survey invitation was distributed through targeted regional hydrogen, steel, energy and innovation networks, and 26 valid responses were received from energy companies, municipalities, infrastructure operators, industrial firms, technology providers and research actors. Respondents were distributed between Finland and Sweden, with 16 from Finland (61.5%) and 10 from Sweden (38.5%). Since each respondent could select from multiple organisational categories, the results describe the range of perspectives offered by the actors involved, rather than mutually exclusive respondent groups. The survey was treated as complementary exploratory evidence rather than as a statistically representative dataset. It was used to broaden the empirical base beyond the five interviews and to examine whether wider stakeholder perceptions supported, complemented or diverged from the interview findings. The responses were integrated with the interview material through thematic comparison; the closed survey items are therefore interpreted as descriptive indicators of stakeholder perceptions rather than as independent measures of regional readiness. The distribution of selected organisational categories is shown in Table 2. Since several of the organisational categories could be selected, the percentages do not sum to 100.

The survey mirrored the themes of the interviews and included Likert-scale, multiple-choice and open-ended questions. Respondents evaluated the maturity of the components of the value chain, identified strengths and bottlenecks, reflected on current and desired collaboration patterns, and provided their own views on the expected development of hydrogen-based steel and related business models. The survey questions followed the same thematic structure as the interview guide, covering the maturity of the value chain, regional strengths and bottlenecks, cross-border collaboration, business models, and system-level requirements for the development of hydrogen-based steelmaking.

Table 2. Organisational categories selected by survey respondents (multi-selection).

Table 2. Organisational categories selected by survey respondents (multi-selection).

The empirical material was analysed using thematic analysis, following Braun and Clarke [55]. The analysis was based on both framework-guided and data-driven coding. The interview transcripts and open-ended survey responses were first coded according to the thematic structure derived from the analytical framework, which involved the stages of the value chain and the technological, infrastructural, market and institutional conditions. Additional empirical codes were then added where respondents had raised issues that were not fully captured by the predefined categories. Next, codes were consolidated into broader analytical categories, which formed the basis for the themes reported in the Results section. Finally, the interview and survey materials were compared within each category to identify converging, complementary and diverging perceptions, following principles of good practice in thematic analysis [55].

Closed survey responses were analysed descriptively, using response counts and percentages. No inferential statistical tests were conducted, since the survey was based on purposive sampling and was used to complement the qualitative analysis rather than to produce statistically generalisable results.

Research Ethics and Data HandlingThe study involved expert interviews and a stakeholder survey with professionals in organisational or expert roles. Participation was voluntary, and participants were informed about the purpose of the study and the use of the collected material. Interviewees gave consent to participate and for the interviews to be recorded for transcription and analysis.

To preserve confidentiality, interviewees are described here using anonymised organisational roles rather than personal names or identifiable organisational attributions. Survey responses were analysed in aggregated form, and open-ended responses were used only in ways that avoided identifying individual respondents or organisations. The empirical material was stored and handled by the research team for research purposes.

The study did not involve medical research, vulnerable participants or the collection of sensitive personal data, and the material was anonymised and handled confidentially by the research team. Under the applicable University of Oulu research ethics procedures, formal ethical approval was not required for this type of study.

TrustworthinessThe trustworthiness of the study was assessed using the criteria of credibility, dependability and transferability [56], which are commonly applied in qualitative business research [54].

Credibility was strengthened through the use of a shared thematic framework across interviews and the survey, enabling comparisons between in-depth expert accounts and broader stakeholder perceptions. Dependability was supported through systematic transcription, consistent coding procedures and transparent documentation of the analytical steps. Transferability was limited by the regional and exploratory nature of the study; however, the contextual description of the Bothnian Bay region, the respondent categories and the focus of the value chain allow the reader to assess the relevance of the findings to other industrial regions. Overall, the research design provides a coherent audit trail from framework development to data collection, analysis and interpretation.

The transferability of the findings is strongest for industrial regions that combine energy-intensive industry, renewable electricity potential, hydrogen-related project activity and cross-border or multi-level governance. The findings may be less transferable to regions without an established base for steel or processing industries, without significant potential for renewable electricity, or without similar cross-border institutional dynamics. The results should therefore be interpreted as context-sensitive analytical insights rather than as generalisable conclusions about all regions involved with hydrogen-based steelmaking.

The results are organised into six empirical themes that explain how regional factors shape the emergence of a value chain for hydrogen-based steelmaking in the Bothnian Bay. The themes synthesise the interview and survey findings across the analytical categories introduced in Section Cross-Border Coordination and System-Level Conditions. In this section, RQ1 is addressed by identifying the main strengths, bottlenecks and cross-border dynamics affecting the formation of the value chain, while a system-level interpretation of these findings is presented in the Discussion in relation to RQ2. Section Thematic Findings presents the thematic findings; the empirical factors are synthesised into a results matrix in Section Synthesis of Results; and the main empirical findings are summarised in Section Summary of Empirical Findings.

Thematic Findings Current State of the Value ChainThe empirical material shows that the value chain in the Bothnian Bay is in a transitional, pre-commercial phase, with uneven maturity across its components. Interviewees emphasised that strategic intent is strong and that major industrial actors have committed to long-term decarbonisation, but several critical elements remain only partially developed. Industrial-scale hydrogen production is not yet available at the regional level: Finland has only one operational producer, and Sweden’s capacity outside the HYBRIT ecosystem remains limited. Most planned projects are still in the feasibility or early development stages, creating uncertainty for downstream steelmaking processes.

The survey results support this assessment. Renewable energy production was rated as developing or fully developed by 88.4% of respondents, while hydrogen research was rated as developing or fully developed by 69.2%. By contrast, hydrogen production was rated as not developed or still at an early stage by 84.6% of respondents, fossil-free steelmaking was rated at these levels by 65.4%, and infrastructure and logistics were rated at these levels by 61.5%. Several respondents also commented on the absence of regional hydrogen suppliers, reinforcing the finding from the interviews that the value chain remains incomplete.

Interviewees also stressed that transition timelines were long and asymmetrical across the region. HYBRIT’s next major milestones were expected in 2028 in Luleå, while SSAB Raahe was aiming for hydrogen-based transformation in the 2030s. There is therefore a combination of strong ambition and piloting activity in the region, with limited operational readiness and incomplete integration of the value chain.

Regional Characteristics of the Bothnian BayInterviewees highlighted several regional strengths supporting the development of hydrogen-based steel. Abundant renewable electricity, particularly from onshore and offshore wind, was consistently viewed as the region’s strongest enabler, and survey respondents ranked the availability of renewable energy as the most important regional advantage. The region also benefits from an established heavy industry base involving steelmaking, chemicals, mining, pulp and other energy-intensive industries. Interviewees noted that this expertise, combined with strong research institutions in Oulu, Luleå and elsewhere, creates favourable conditions for transition to a hydrogen-based industrial sector.

Structural weaknesses were also repeatedly identified. Interviewees and survey respondents pointed to a thin local supply base for essential hydrogen and steelmaking equipment, including electrolysers, compressors, storage systems and specialised metallurgical components. This dependency on international vendors creates long delivery chains and increases investment risk. Respondents also cited high upfront costs, uncertain future electricity prices and the limited size of the region’s local market, which increases the importance of export-oriented value chains.

A further defining feature is the structural asymmetry between Finland and Sweden. Interviewees noted clear differences in industrial policy, public support mechanisms, permitting practices and strategic priorities. Sweden’s longer-established and more centralised support for fossil-free steel through HYBRIT and Stegra contrasts with Finland’s more decentralised, market-driven approach. These differences influence investment timing, the strength of business cases and the predictability of cross-border development.

Technological Development and ResearchTechnological maturity is a decisive factor affecting the region’s transition to hydrogen-based steel. Interviewees agreed that the Bothnian Bay has strong engineering and scientific expertise, but emphasised that further development of several technologies and system configurations will be required before rapid industrial-scale deployment.

Electrolysers were identified as an important technological and cost-related constraint. Interviewees noted that large-scale hydrogen production facilities must be able to operate under conditions shaped by variable renewable electricity, volatile electricity prices and high reliability requirements. Although alkaline and PEM electrolysers are commercially available, respondents raised concerns about cost, availability, long-term performance and operational integration with fluctuating renewable power. Survey respondents also identified electrolyser costs and performance uncertainty as major barriers.

The maturity of hydrogen-based direct reduction (H2-DRI) also remains uneven in this region. Interviewees referenced HYBRIT’s pilot success but highlighted remaining uncertainties concerning cost, performance at scale, ore quality requirements and integration into existing steel plants. On the Finnish side, interviewees noted that SSAB Raahe’s transition will depend heavily on whether local DRI capacity is eventually developed; otherwise, reliance on imported sponge iron from Sweden could limit flexibility and complicate logistics.

Despite these constraints, however, the technological strengths are notable. The region’s universities and research centres are conducting advanced work on electrolysis, hydrogen systems, the effects of fossil-free production routes on steel microstructures and properties, and industrial integration. Interviewees emphasised the long-standing collaboration between academia and industry as a significant accelerant for development, while the survey respondents rated research and education among the most advanced components of the region’s value chain. The main technological finding is therefore not a lack of expertise, but the gap between strong research and pilot activity and the maturity required for scalable industrial implementation.

Cross-Border CollaborationCross-border collaboration between Finland and Sweden is a defining regional characteristic and an important condition for developing a value chain for hydrogen-based steel. Interviewees described strong cooperation between universities, research centres and major industrial actors, citing joint projects, technology pilots and cross-border networks as key strengths. Survey respondents also ranked collaboration as one of the most important long-term enablers, reflecting the interconnected nature of the region’s industrial and energy systems.

However, the empirical material also reveals persistent structural barriers. Interviewees pointed to divergence between regulatory and institutional processes in Finland and Sweden, including differences in permitting processes, environmental assessments, state aid frameworks and grid connection practices. Sweden’s more centralised support for fossil-free steel contrasts with Finland’s more decentralised approach, and these differences may affect both the location and timing of major hydrogen-based steel investments.

Survey respondents evaluated the current level of collaboration less favourably than its desirability. Many warned that without alignment between strategy, regulation and infrastructure planning, there is a risk of duplication of effort in the region or the development of incompatible systems. Interviewees also noted challenges associated with infrastructure interoperability, particularly regarding hydrogen transport options, port logistics, grid development priorities and industrial zoning. The findings therefore indicate that although research and knowledge exchange across the border are strong, deeper coordination is required in terms of permitting, strategic planning and infrastructure design.

Business ModelsThe development of business models emerged as one of the most critical conditions for enabling hydrogen-based steelmaking in the region. Interviewees emphasised that the scale of the investment required demands coordinated, multi-actor approaches, as no single firm can carry the full risk independently.

The need for long-term offtake agreements was highlighted. Interviewees noted that predictable demand and price visibility for fossil-free steel are essential for investment decisions in hydrogen production and infrastructure. The existence of early agreements between steelmakers and automotive companies indicate the emergence of a market, but these remain limited compared with the scale required for full deployment of the value chain. Survey respondents echoed this view by ranking long-term contracts for hydrogen, steel and electricity as key enablers for market formation and financing, since stable demand reduces the risk to upstream actors.

Interviewees also pointed to the need for shared investment models. Co-investment between steel producers, energy companies and technology providers was viewed as especially important in Finland, where uncertainty over local DRI capacity creates ambiguity around the coordination of hydrogen production, sponge iron logistics and steelmaking. Volatile electricity prices were another major concern, as industrial hydrogen production is highly sensitive to variation in input cost. Overall, viable business models depend on risk-sharing arrangements, long-term contracts and aligned incentives across the value chain.

Regulation and PolicyRegulation and policy influence the hydrogen-based steel value chain as both long-term drivers and near-term barriers. Interviewees consistently identified the EU Emissions Trading System (ETS) as an important driver of hydrogen-based steelmaking. As free allowances decline toward 2035–2040, conventional steel production will become increasingly expensive, strengthening the business case for low-carbon production routes.

In addition, regulation creates significant uncertainty. Survey respondents ranked policy uncertainty and slow, complex permitting processes among the most substantial barriers to regional development. Interviewees highlighted that shifting national and EU-level political priorities create mixed signals for industry, complicating long-term planning and investment sequencing.

Cross-border regulatory divergence deepens these challenges. Differences between Finland and Sweden in terms of permitting timelines, environmental assessments, grid connection rules and state aid frameworks create structural friction that slows joint or parallel development. Respondents repeatedly called for harmonised cross-border frameworks, predictable support mechanisms and simplified permitting procedures.

Interviewees also noted the absence of hydrogen-specific regulation regarding safety, transport infrastructure, storage and guarantees of origin. These gaps affect the entire value chain, from renewable expansion and electrolyser deployment to hydrogen storage and steelmaking operations. The findings indicate that regulation and policy are decisive but unstable conditions: long-term climate policy supports this transition, but policy-related unpredictability, slow permitting and insufficient harmonisation continue to impede progress.

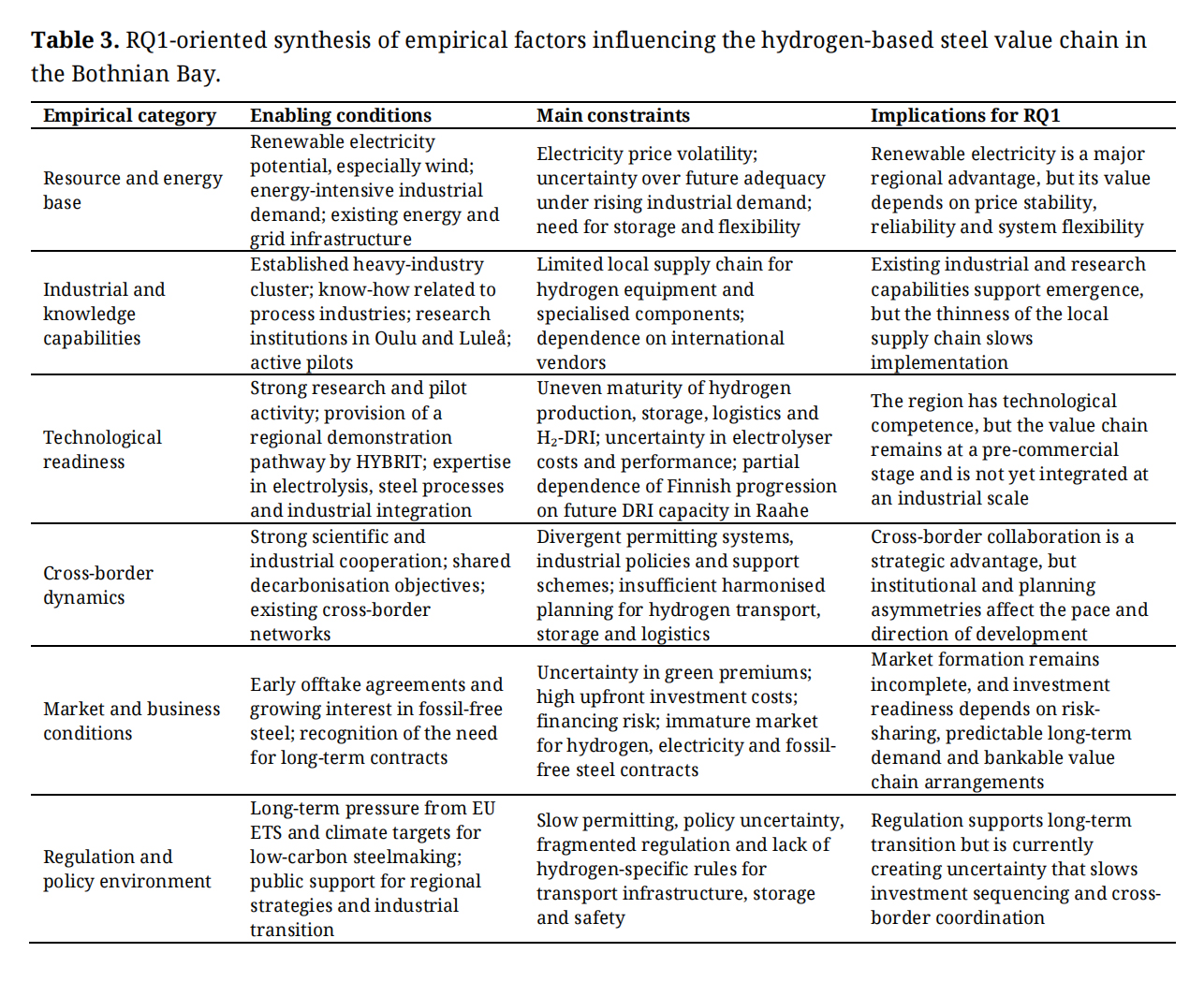

Synthesis of ResultsTaken together, the interview and survey findings show that the emergence of a hydrogen-based steel value chain in the Bothnian Bay is shaped by a combination of enabling regional conditions and unresolved constraints on scaling up. To make these results more accessible, Table 3 synthesises the six thematic findings into a matrix that is oriented towards answering RQ1. Distinctions are made between enabling conditions, constraints and their implications for the emergence of a value chain. However, these categories should be interpreted as analytical distinctions rather than as separate or linear causal factors. In practice, electricity price volatility, hydrogen infrastructure, steelmaking investments, market formation, permitting and cross-border governance are mutually interdependent. For example, infrastructure choices affect investment risk, while offtake uncertainty affects decisions on hydrogen production and cross-border permitting affects the timing of infrastructure deployment.

Table 3. RQ1-oriented synthesis of empirical factors influencing the hydrogen-based steel value chain in the Bothnian Bay.

Table 3. RQ1-oriented synthesis of empirical factors influencing the hydrogen-based steel value chain in the Bothnian Bay.

This synthesis shows that the Bothnian Bay has a strong regional basis for hydrogen-based steel development, particularly in terms of renewable electricity potential, industrial competence and research capacity. However, these advantages are offset by the incomplete development of hydrogen production, infrastructure and markets, as well as regulatory and cross-border coordination constraints. The main empirical finding is therefore not that the region lacks potential, but that the components of the value chain required for industrial-scale deployment are not yet sufficiently aligned. Accordingly, Table 3 should be read as a synthesis of interacting conditions rather than as a ranking or list of independent barriers.

Summary of Empirical FindingsThe results give rise to four main findings in relation to RQ1. Firstly, the Bothnian Bay has a credible regional basis for the development of hydrogen-based steelmaking, especially renewable electricity potential, process industry capabilities and research expertise. Secondly, the value chain remains at a pre-commercial stage, as hydrogen production, storage, transport logistics and hydrogen-based steelmaking capability are not yet integrated at an industrial scale. Thirdly, the regional trajectory is asymmetric: the Swedish side is further advanced through HYBRIT and Stegra, while the Finnish pathway will depend strongly on future decisions concerning SSAB Raahe, local DRI capacity, hydrogen production and infrastructure. Finally, the formation of a value chain depends on parallel progress in energy supply, hydrogen production, infrastructure, markets and regulation.

In this section, the empirical findings will be interpreted based on the analytical framework introduced in Section Cross-Border Coordination and System-Level Conditions, which considers the stages of the value chain and the technological, infrastructural, market and institutional conditions. The central finding is that the Bothnian Bay does not lack potential for the development of hydrogen-based steelmaking, but that its transition is constrained by misalignment between the components of the value chain and the conditions at the system level. The strong renewable electricity potential, established industrial capabilities and research expertise in the region are not yet matched by commercial hydrogen production, infrastructure readiness, market formation, bankable investment arrangements or coordinated governance.

These findings support the theoretical expectation that hydrogen-based steel ecosystems depend on the parallel development of multiple complementary conditions. Technological development alone is insufficient if the development of hydrogen supply methods, storage or transport options, offtake structures and permitting processes remains uncertain. The availability of renewable electricity is a major regional advantage, but this becomes a practical enabler of the value chain only when combined with predictable electricity prices, an adequate grid, suitable hydrogen production configurations and industrial demand. This suggests that renewable-rich regions may gain industrial advantages only when the potential for renewable electricity generation is converted into reliable, affordable and investable energy conditions, a result that is aligned with recent work on the transformation of European energy systems, renewable-rich industrial regions and steel decarbonisation [1,11,12,43].

The Bothnian Bay case also shows that the relevant bottlenecks are interactive rather than isolated. Investment in hydrogen production depends on credible demand from steel producers, while steel producers depend on the reliable availability of hydrogen, predictable electricity prices, suitable material flows, and regulatory clarity. Infrastructure choices also depend on whether hydrogen is produced on site, near industrial users, or transported from external production sites. The primary issue is therefore not whether one specific infrastructure model, such as a pipeline-based system, is required; rather, it is how electricity supply, hydrogen production, storage, transport options and industrial offtake can be sequenced in such a way as to reduce uncertainty and avoid fragmented investment.

This interpretation is consistent with recent studies of the hydrogen implementation gap. The IEA [25] shows that low-emissions hydrogen remains below 1% of global production and that the potential low-emissions hydrogen production expected by 2030 based on announced projects has declined because of delays and cancellations. Odenweller and Ueckerdt (2025) [26] also show that only a small proportion of the anticipated capacity for green hydrogen has been realised on schedule, meaning that project announcements should not be treated as equivalent to deployment. The findings for Bothnian Bay reflect this broader pattern at a regional level: strategic intent, pilot activity and research capacity are strong, but industrial-scale implementation remains constrained by incomplete coordination across the value chain.

The regional implementation gap can therefore be interpreted as a socio-technical transition challenge. The empirical findings show that the main barriers do not arise from a single missing technology or actor group, but from the incomplete alignment of complementary system elements. The potential for renewable electricity does not automatically create a competitive region for hydrogen-based steelmaking unless it is combined with adequate grid capacity, predictable electricity prices, hydrogen production, storage and transport options, industrial offtake and regulatory certainty. Similarly, hydrogen valley and ecosystem initiatives may create shared expectations and coordination arenas, but they may also risk overinvestment, premature infrastructure lock-in or regional dependency if infrastructure and production choices are made before demand, certification, permitting and market conditions are sufficiently clear. The Bothnian Bay case therefore illustrates how regional potential can remain difficult to realise when technological, infrastructural, market and institutional conditions develop at different speeds.

This framework-based interpretation also clarifies the role of cross-border conditions. Finland and Sweden share a regional industrial base and decarbonisation objectives, but the empirical findings show differences in policy support, permitting practices, industrial project maturity and investment sequencing. These differences do not eliminate the region’s potential, but they complicate the coordinated formation of a value chain. The literature on ecosystems emphasises that complementary investments must be aligned for new industrial systems to emerge [29,30]. In the Bothnian Bay, the challenges related to this alignment are intensified by the cross-border setting.

Pace of Implementation and Feasibility of Scaling UpThe findings suggest that the current pace of development in the Bothnian Bay is not yet sufficient for a fully functioning value chain to emerge on the timeline implied by European hydrogen and industrial decarbonisation targets, including the EU’s 2030 renewable hydrogen ambitions [22,23]. The region has a strong basis for development, including renewable electricity potential, steelmaking capability, industrial demand, and research expertise, but these aspects have not yet been translated into an integrated industrial-scale value chain. The empirical material shows that there are differing levels of maturity in terms of hydrogen production, storage, transport options, offtake arrangements, permitting processes and cross-border planning. This creates a gap between regional potential and implementation readiness.

This assessment is consistent with the broader literature on the hydrogen transition showing that low-emissions hydrogen remains marginal in regard to global production and that the announced hydrogen capacity has often lagged behind expectations [25,26]. These studies underline that project announcements should not be treated as equivalent to implementation.

The Bothnian Bay case reflects this broader implementation gap at the regional level. Strategic intent and pilot activity are visible, particularly on the Swedish side through HYBRIT and Stegra, while the Finnish pathway remains contingent on future decisions concerning SSAB Raahe, local DRI capacity, hydrogen production and infrastructure development. This does not mean that Sweden already has a complete value chain for hydrogen-based steelmaking or that Finland lacks potential. Instead, it shows that the regional transition is asymmetric: some components are advancing faster than others, and national policy, permitting and investment conditions differ across the border.

The current track record therefore does not support the conclusion that the region is already on a self-sustaining path toward industrial-scale hydrogen-based steel production. Instead, the findings indicate that scaling up will depend on coordinated acceleration across several interdependent areas. Hydrogen supply must become commercially available at an appropriate scale, but this can be achieved through different configurations, including onsite production, nearby production or transported hydrogen, depending on project-specific economics and infrastructure choices. Similarly, infrastructure development should not be reduced to a single pipeline-based model. The primary requirement is to clarify the relationships between electricity supply, hydrogen production, storage, transport options, port and logistics capacity, and industrial offtake.

This assessment should be interpreted as a perception-based and literature-informed evaluation of regional implementation readiness rather than a quantified techno-economic benchmark. Calculations are not presented here for hydrogen price thresholds, capital expenditure requirements, levelised steel production costs or green premium levels. Nevertheless, the empirical findings indicate why these economic factors are central to scaling up. The cost competitiveness of hydrogen-based steel depends on electricity price exposure, electrolyser utilisation, hydrogen production and storage costs, DRI–EAF investment requirements, infrastructure CAPEX, logistics costs, policy support and the willingness of downstream customers to pay for low-emissions steel. Without long-term offtake agreements, predictable electricity arrangements and risk-sharing mechanisms, regional strengths may remain insufficient to support bankable investment decisions. In future research, the qualitative regional analysis should be complemented with techno-economic modelling and project-level comparisons of alternative hydrogen supply configurations.

This finding has implications for the interpretation of hydrogen targets. The main issue involves not only whether sufficient hydrogen can be produced, but whether it can be deployed in applications where it is strategically necessary. Hydrogen-based steelmaking is a credible use case, since direct electrification cannot replace the chemical reduction function in primary ironmaking. However, the slow deployment of low-emissions hydrogen implies that priority for early use should be given to applications with credible industrial demand [26].

Overall, the Bothnian Bay can be described as a promising region for hydrogen-based steelmaking that is not yet implementation-ready. The term implementation-ready is therefore used in a restricted analytical sense: it refers to whether the main value-chain components and system-level conditions appear sufficiently aligned for coordinated industrial scale-up, not to a quantified assessment of project feasibility, hydrogen costs or infrastructure capacity. The current pace of development is insufficient for a fully integrated value chain to emerge without stronger coordination of investment sequencing, electricity and hydrogen supply, market formation and institutional alignment. This does not undermine the region’s potential, but does clarify the challenge involved in scaling up: the transition will depend less on additional project announcements than on the conversion of regional strengths into bankable projects, long-term offtake structures, predictable infrastructure choices and harmonised governance across Finland and Sweden. This reinforces the need to assess hydrogen initiatives not only based on the reported capacity or strategic ambition, but on their ability to reach investable and operational configurations [26,27].

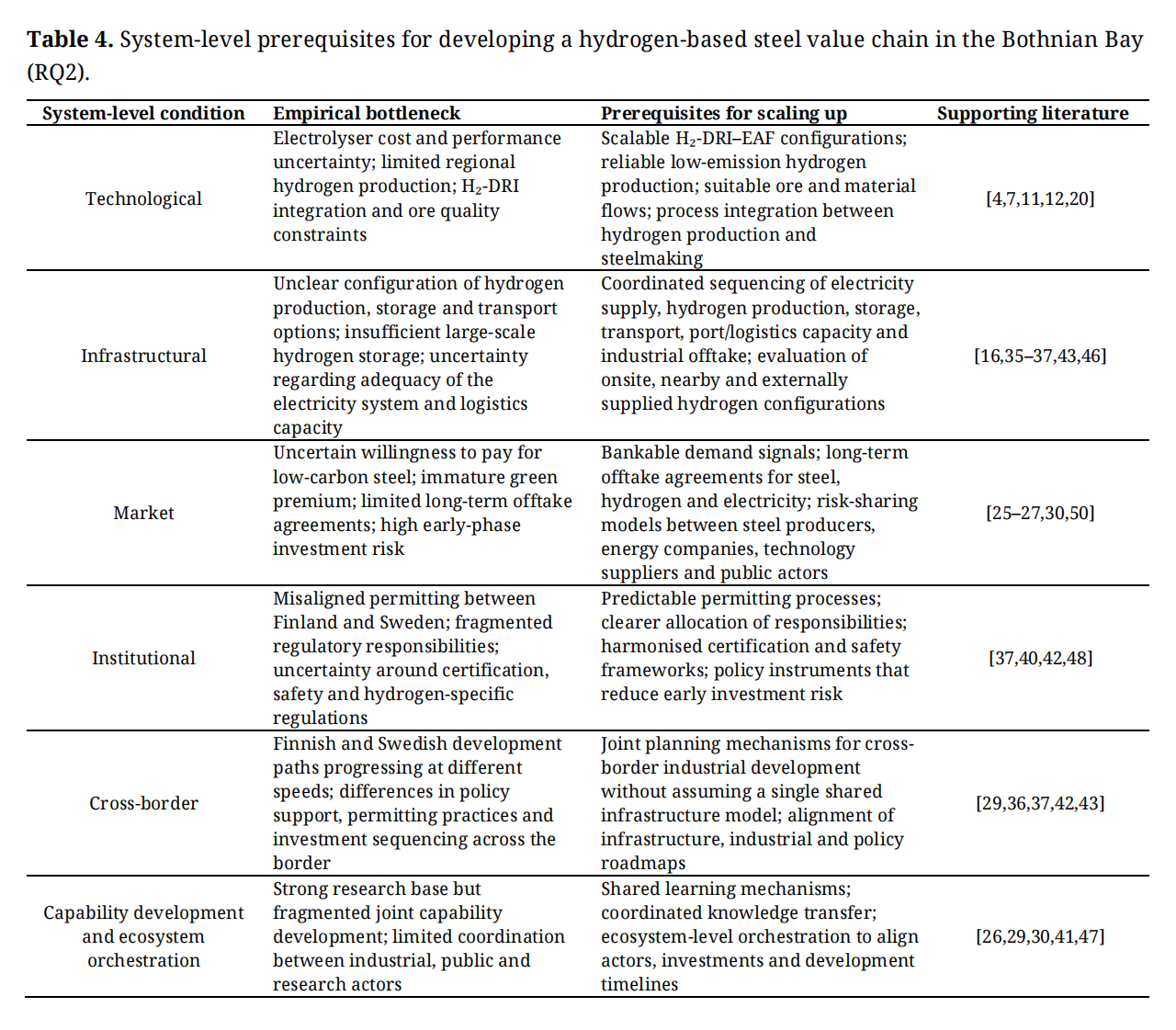

System-Level Prerequisites for Developing a Value Chain (RQ2)The findings indicate that the development of a functioning value chain for hydrogen-based steelmaking in the Bothnian Bay will require coordinated progress across technological, infrastructural, market and institutional conditions. These prerequisites were identified based on the empirical findings from the interviews and survey, and are structured according to the system-level condition domains of the analytical framework presented in Section Cross-Border Coordination and System-Level Conditions. Table 4 summarises the main bottlenecks, the corresponding prerequisites for scaling up, and relevant works in the literature.

Table 4 shows that no single condition is sufficient on its own. The primary issue involves the sequencing and mutual alignment of prerequisites across the value chain. Hydrogen production depends on electricity availability, price stability and technology choices, but investment in hydrogen production also depends on credible industrial demand, infrastructure choices and regulatory predictability. Similarly, hydrogen-based steelmaking depends not only on H2-DRI–EAF technologies, but also on suitable material flows, electricity market exposure, offtake arrangements, investment timing and permitting.

The findings therefore indicate that the immediate challenge does not involve simply building one missing asset, such as a pipeline or a single production facility. This is consistent with recent work on European energy systems showing that although net-zero industrial strategies can reshape cross-border hydrogen infrastructure needs, infrastructure choices depend on assumptions related to regional production, demand and system integration [43]. Clarification is required on how hydrogen for steelmaking will be produced, stored, transported and linked to industrial offtake in a given region. These choices may involve onsite production, nearby production or externally supplied hydrogen, depending on project-specific economics and infrastructure conditions. Overemphasising one pathway too early may create lock-in or misdirect investment.

Table 4.

System-level prerequisites for developing a hydrogen-based steel value chain in the Bothnian Bay (RQ2).

Table 4.

System-level prerequisites for developing a hydrogen-based steel value chain in the Bothnian Bay (RQ2).

Environmental sustainability also needs to be assessed across the full value chain, rather than assumed based on the use of hydrogen alone. The climate and environmental performance of hydrogen-based steelmaking depends on the electricity source used, electrolyser production process, hydrogen storage and transport configuration, steelmaking route, material inputs, and system boundaries used in assessment. Life cycle assessment can support a comparison between alternative hydrogen supply configurations and conventional steelmaking routes by identifying where emissions, resource use or other environmental burdens occur across the value chain [2,8,21]. Critical material requirements are also relevant to scalability, since electrolysers, storage technologies, grid expansion and hydrogen infrastructure may depend on materials whose availability, cost, environmental impacts and supply chain resilience affect long-term deployment. For the Bothnian Bay, this means that future project evaluations should combine regional techno-economic assessments with life cycle and material supply analyses before specific infrastructure pathways are locked in.

Market and institutional prerequisites are equally important. Long-term offtake agreements, risk-sharing arrangements and clearer demand signals are needed to reduce the problem of “who moves first”, while predictable permitting, certification and safety regulations are needed to reduce uncertainty over cross-border investment. The region also requires stronger ecosystem orchestration to align industrial timelines, infrastructure planning and knowledge transfer between Finland and Sweden.

Overall, RQ2 can be answered as follows: a functioning hydrogen-based steel value chain can be developed in the Bothnian Bay only if technological, infrastructural, market and institutional conditions are advanced in parallel. The primary requirement is a coordinated form of implementation between electricity supply, hydrogen production, storage and transport options, industrial offtake, regulatory alignment and cross-border governance.

Theoretical and Practical ImplicationsThe study has two main theoretical implications. Firstly, it shows that the formation of a value chain for hydrogen-based steel cannot be explained by technological readiness alone. The Bothnian Bay case demonstrates that emergence depends on alignment between technological, infrastructural, market and institutional conditions across interdependent stages of the value chain. This finding is consistent with ecosystem and value-chain perspectives that emphasise complementary investments and coordinated sequencing, and it extends these perspectives by applying them to a cross-border industrial region.

Secondly, the study connects debates on the hydrogen implementation gap with the formation of regional value chains. The findings show that the gap between ambition and deployment in this area is not solely related to global or national policies, but also arises at the cluster level when infrastructure choices, offtake structures, electricity system conditions and governance remain misaligned. The findings also caution against treating emerging hydrogen regions as complete hydrogen valleys before completeness of the value chain, established governance arrangements, regulatory clarity and deployment readiness, particularly given the definitional and legal ambiguity surrounding the development of hydrogen valleys [40].

In practice, policy makers and industrial actors should focus less on announcing additional hydrogen projects and more on converting existing regional strengths into bankable implementation pathways. In the Bothnian Bay, a more operational coordination function between Finland and Sweden is required for development in the area of hydrogen-based steel. This does not necessarily imply the need for a new formal authority, but a structured forum should be provided via which steel producers, energy companies, infrastructure operators, ports, public authorities, research organisations and potential customers can align industrial timelines, electricity grid development, hydrogen production, storage and transport options, port and logistics planning, and knowledge transfer. This would support the development of coordination and complementary investment logic at the ecosystem level discussed in the literature [29,30].

More concretely, cross-border coordination should include at least four practical mechanisms. Firstly, Finland and Sweden should develop a shared roadmap for hydrogen-based steel infrastructure that considers onsite, nearby and transported hydrogen configurations rather than assuming a single predefined infrastructure model. This would be consistent with the literature on hydrogen infrastructure and corridor planning in Europe, which emphasises that hydrogen infrastructure choices depend on regional production, demand, storage, and transport assumptions [36,37]. Secondly, procedures for permitting, safety regulation and environmental assessment should be made more predictable through regular cross-border regulatory dialogue, particularly for hydrogen storage, transport, ports and industrial use. Thirdly, certification and guarantees-of-origin practices should be harmonised or made mutually recognisable in order to reduce uncertainty in cross-border hydrogen and low-emission steel markets [40,57]. Finally, public and private actors should develop risk-sharing and co-investment mechanisms, such as joint infrastructure planning, public–private partnerships, contracts for difference, investment guarantees or coordinated offtake arrangements, in order to reduce the problem of “who moves first” between steel producers, energy companies, infrastructure operators and downstream customers. These mechanisms would make the practical implementation pathway more credible than general regional ambition alone.

This study has examined the emergence of a value chain for hydrogen-based steel in the Bothnian Bay region through semi-structured expert interviews and a complementary Webropol survey. A framework was applied based on the stages of the value chain and the technological, infrastructural, market and institutional conditions.

In relation to RQ1, the findings show that the Bothnian Bay has favourable regional conditions for the development of hydrogen-based steelmaking, such as renewable electricity potential, established steelmaking and process industry capabilities, research expertise and existing industrial demand. However, these strengths are counterbalanced by limited capacity for industrial-scale hydrogen production, immature storage and transport options, uncertain electricity and offtake conditions, and differences in policy support, permitting and investment sequencing between Finland and Sweden. The Swedish side appears to be further advanced in terms of the existing deployment of hydrogen-based steel through HYBRIT and Stegra, while the Finnish pathway remains dependent on future decisions concerning SSAB Raahe, local DRI capacity, hydrogen production and infrastructure development.

In relation to RQ2, the study shows that a functioning value chain for hydrogen-based steel can be developed in the Bothnian Bay only if technological, infrastructural, market and institutional conditions advance in parallel. The primary requirement is not a single asset, such as a specific transport infrastructure solution, but a coordinated implementation that includes electricity supply, hydrogen production, storage and transport options, industrial offtake, permitting, certification and cross-border governance. The current pace of development is not yet sufficient for the region to be considered implementation-ready as an integrated ecosystem for hydrogen-based steel.

This study contributes to the literature on hydrogen value chains and industrial ecosystems by showing how implementation gaps arise at the regional cluster level. The findings demonstrate that regional potential is not automatically translated into the formation of a value chain when complementary assets, market signals and institutional arrangements remain misaligned. The findings also caution against treating emerging hydrogen regions as implementation-ready hydrogen valleys before a complete value chain, regulatory clarity and coordinated governance are in place. For policymakers and industrial actors, the main implication is that development in the area of hydrogen-based steel should focus on converting existing regional strengths into bankable, coordinated implementation pathways. In practice, this requires long-term offtake agreements, predictable electricity arrangements, a shared infrastructure roadmap between Finland and Sweden, clearer permitting and safety procedures, mutually recognised certification and guarantees-of-origin practices, and public–private risk sharing mechanisms that support joint investment in hydrogen production, storage, transport, port logistics and low-emission steel markets.

These mechanisms are not proposed as a single governance blueprint. Rather, they indicate the types of coordination functions through which the prerequisites identified in Table 4 could be translated into implementation: reducing uncertainty for investors, improving infrastructure compatibility, and aligning permitting, certification and offtake arrangements across the border.

The study is limited by its exploratory qualitative design and by the early stage of development of hydrogen-based steel in the region. The interview and survey material captures informed stakeholder perceptions, but the value chain itself is still largely at a pre-commercial stage, meaning that future investment decisions, policy changes and technology deployment may alter the regional trajectory. Further research is needed to examine the evolution of concrete hydrogen-based steel projects over time, compare alternative hydrogen supply configurations, and assess the economic and infrastructural feasibility of onsite, nearby and transported hydrogen models in cross-border industrial regions.

The datasets generated and analysed during the current study are not publicly available because they contain interview and survey material from a limited group of regional experts and stakeholders, and public release could compromise participant and organisational confidentiality. Aggregated survey results and anonymised empirical findings are reported in the manuscript. Further information may be available from the corresponding author upon reasonable request, subject to confidentiality and ethical restrictions.

Conceptualization, AL, KH, PT and HH; methodology, AL, KH, PT and HH; investigation, AL; formal analysis, AL, KH; data curation, AL; writing—original draft preparation, AL, KH; writing—review and editing, AL, KH, PT and HH; supervision, PT and HH; project administration, AL All authors have read and agreed to the published version of the manuscript.

The authors declare that they have no conflicts of interest.

The authors received no specific funding for this work.

The authors are grateful to the interviewees and survey respondents for their valuable time and insights, and to colleagues who provided feedback during the research process. The authors also acknowledge the support of the wider research project environment, including project meetings and discussions with academic and regional stakeholders, which helped shape the development of the research topic.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

39.

40.

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

Lammassaari A, Hurskainen K, Tervonen P, Haapasalo H. Emergence of a Hydrogen-Based Steel Ecosystem in the Bothnian Bay: Regional Factors and System-Level Prerequisites. J Sustain Res. 2026;8(3):e260064. https://doi.org/10.20900/jsr20260064.

Copyright © Hapres Co., Ltd. Privacy Policy | Terms and Conditions